Ultimate Guide to Balancing Cash and Non-Cash Donations

Want to maximize your tax benefits while giving back? Balancing cash and non-cash donations is the key. Cash donations are straightforward and deductible up to 60% of your Adjusted Gross Income (AGI). Non-cash donations, like appreciated stocks or real estate, offer unique tax advantages, including avoiding capital gains taxes and deducting the full fair market value, though they’re capped at 30% of AGI.

Key Takeaways:

- Cash Donations: Deductible up to 60% of AGI for public charities; 30% for private foundations.

- Non-Cash Donations: Deductible up to 30% of AGI for public charities; 20% for private foundations.

- 2026 Rule Changes: Deductions for high earners capped at 35%, with itemized deductions requiring contributions to exceed 0.5% of AGI.

- Documentation: Accurate records are crucial - receipts, written acknowledgments, and IRS forms (e.g., Form 8283 for non-cash donations over $500).

Pro Tip: Combine cash and non-cash donations strategically to stay within AGI limits and carry forward excess deductions for up to five years. Use tools like Deductible.me to simplify tracking and compliance.

Ready to optimize your giving? Let’s dive into the details.

Year End Charitable Donation Tax Strategies #charitable #donation #taxstrategy

sbb-itb-e723420

IRS Tax Deduction Limits for Cash and Non-Cash Donations

IRS Tax Deduction Limits for Cash vs Non-Cash Charitable Donations

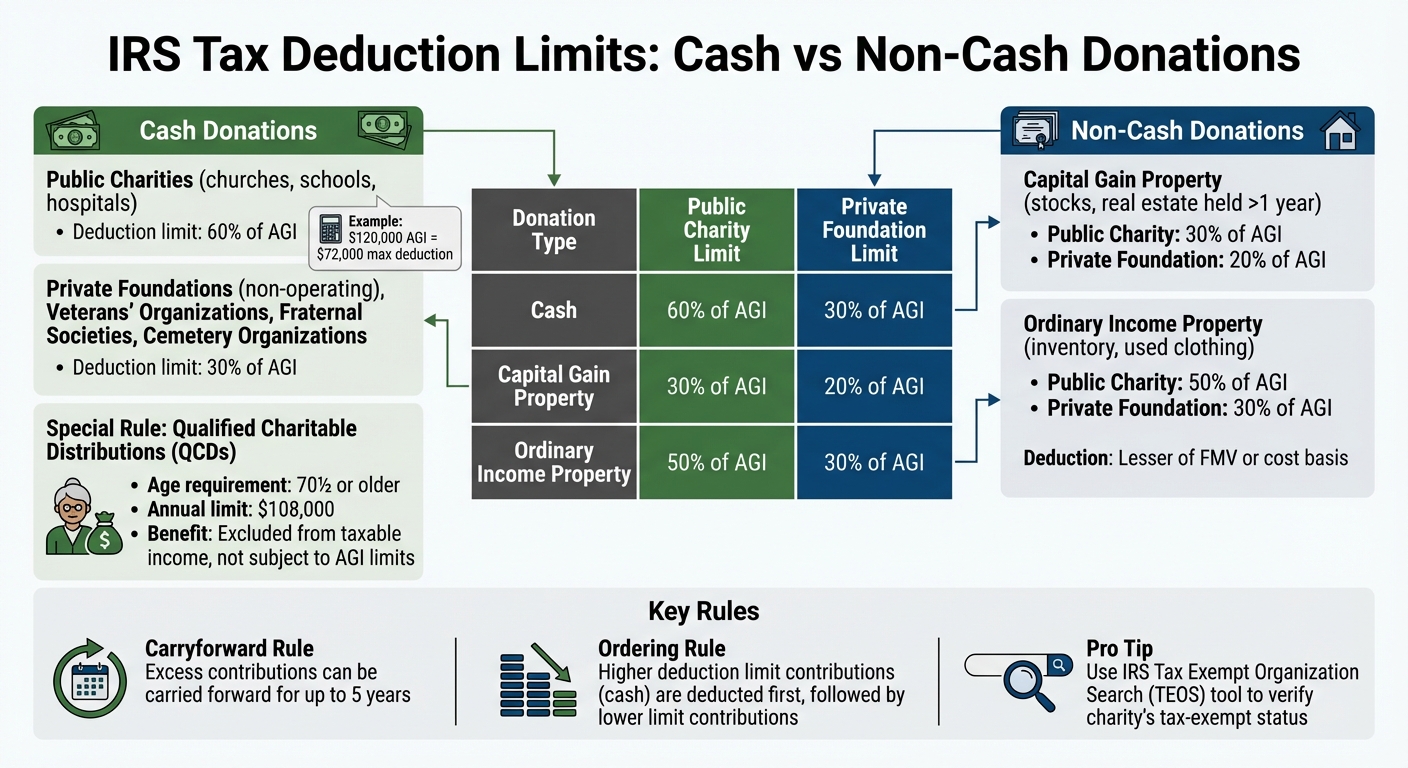

Knowing the IRS's rules for Adjusted Gross Income (AGI) limits is key to planning your charitable donations effectively. These limits vary based on the donation type and the organization receiving it. They dictate the maximum amount you can deduct in a single year, with any extra deductions carried over for up to five years [5].

Cash Donation Limits

For cash donations to public charities - like churches, schools, and hospitals - you can generally deduct up to 60% of your AGI [5]. For instance, if your AGI is $120,000, you can claim up to $72,000 in cash contributions in that tax year.

However, donations to private non-operating foundations, veterans' organizations, fraternal societies, and cemetery organizations are capped at 30% of AGI [4]. To take advantage of these deductions, you’ll need to itemize your deductions if they exceed the standard deduction for your filing status.

If you’re 70½ or older, there’s another option: Qualified Charitable Distributions (QCDs). You can transfer up to $108,000 annually directly from your IRA to a public charity. These distributions are excluded from taxable income and aren’t subject to AGI limits [5].

Next, let’s look at how non-cash donations are treated differently.

Non-Cash Donation Limits

Non-cash donations come with their own set of rules. If you donate capital gain property - like stocks or real estate held for over a year - to a public charity, the deduction is capped at 30% of your AGI [6]. For the same type of donation to a private non-operating foundation, the limit drops to 20% of AGI [6].

For ordinary income property, such as inventory or used clothing, the limits are 50% of AGI for public charities and 30% for private foundations. In these cases, the deduction is typically the lesser of the fair market value or your cost basis [6].

| Donation Type | Public Charity Limit | Private Foundation Limit |

|---|---|---|

| Cash | 60% of AGI | 30% of AGI |

| Capital Gain Property | 30% of AGI | 20% of AGI |

| Ordinary Income Property | 50% of AGI | 30% of AGI |

To ensure your donation qualifies, use the IRS Tax Exempt Organization Search (TEOS) tool to verify the recipient's tax-exempt status [4].

Now, let’s explore how combining donation types can maximize your tax benefits.

How to Combine Cash and Non-Cash Contributions

You can combine cash and non-cash donations in the same year, but the IRS applies ordering rules [6]. Typically, contributions with higher deduction limits - like cash donations - are deducted first, followed by those with lower limits.

For example, mixing cash donations with appreciated assets allows you to maximize deductions, provided each stays within its respective limit.

If your total contributions exceed the AGI limit for the year, the IRS lets you carry forward the excess for up to five years [4]. Keeping track of these carryovers ensures you don’t miss out on deductions in future years. Many tax preparation software tools can help by automatically calculating AGI limits and tracking carryovers.

For property that has lost value, consider selling it first. That way, you can claim both a capital loss and a charitable deduction [6].

Tax Benefits of Non-Cash Donations

Non-cash donations come with some unique tax perks that cash contributions don’t offer. Two major advantages include avoiding capital gains tax and deducting the full fair market value (FMV) of the donated asset.

Avoiding Capital Gains Tax

When you donate appreciated property directly to a qualified charity, you sidestep the capital gains tax on the asset’s growth. This can be a game-changer, especially for those in higher capital gains tax brackets.

"If a taxpayer donates appreciated property directly to a qualified charity, he/she will not be taxed on the appreciation in value. And the even better news…neither will the charity!"

- Mike Batts, CPA, Batts Morrison Wales & Lee

Since public charities are tax-exempt, they can sell the donated asset without paying federal income tax on the gain. This means the charity gets the full value of the asset to support its mission. For instance, say you bought stock for $10,000, and it’s now worth $50,000. By donating the stock directly, you avoid paying taxes on the $40,000 gain and still claim a $50,000 deduction.

However, this benefit only applies if you’ve held the asset for more than a year. If you’ve owned it for a year or less, the IRS considers it ordinary income property, so your deduction is limited to what you originally paid for it (your cost basis) instead of its current market value.

Fair Market Value Deductions

Fair market value (FMV) plays a key role in determining how much you can deduct for non-cash donations. FMV reflects the price an asset would sell for on the open market when both buyer and seller are knowledgeable and willing to act [7].

"FMV is the price that property would sell for on the open market. It is the price that would be agreed on between a willing buyer and a willing seller, with neither being required to act, and both having reasonable knowledge of the relevant facts."

For publicly traded stocks, FMV is calculated by averaging the highest and lowest selling prices on the day of the donation. For other assets, like real estate or artwork, determining FMV might involve comparing recent sales, estimating replacement costs, or even hiring a professional appraiser. Keep in mind, if you’re donating tangible personal property (like art or jewelry), you can only deduct the full FMV if the charity uses the item for its mission. Otherwise, your deduction is capped at your cost basis.

These rules highlight why non-cash donations often make sense when dealing with appreciated assets.

When Non-Cash Donations Make More Sense

Non-cash donations shine when you’re holding highly appreciated, low-cost-basis assets. It’s worth reviewing your portfolio for positions with large unrealized gains.

One strategy is to donate low-basis shares and then use cash to repurchase the same stock. This resets your cost basis to the current market price, allowing you to claim a charitable deduction now while minimizing future tax exposure. Plus, donating directly helps you offload concentrated or risky positions in your portfolio without triggering a taxable event from selling the asset.

| Feature | Gifting Cash (After Selling Stock) | Gifting Appreciated Stock Directly |

|---|---|---|

| Capital Gains Tax | Donor pays up to 23.8% on the gain | $0 (Tax avoided) |

| Deduction Amount | Cash amount after taxes | Full fair market value |

| Impact to Charity | Reduced by the tax paid on the gain | 100% of the asset's value |

| Portfolio Impact | Depletes liquid cash reserves | Eliminates concentrated or risky positions |

Looking ahead, starting in 2026, deductions for appreciated property will generally be capped at 30% of your Adjusted Gross Income (AGI) for public charities, compared to 60% for cash donations. Even with this limitation, the tax savings from avoiding capital gains often outweigh the lower AGI limit, especially for assets with significant appreciation. By understanding these rules, you can better balance cash and non-cash donations to maximize your tax benefits.

Documentation and IRS Compliance Requirements

Keeping accurate records is essential when balancing cash and non-cash donations to preserve their tax benefits. Proper documentation not only simplifies tax filing but also helps avoid IRS audits.

Cash Donation Documentation

The IRS considers cash donations to include payments made by cash, check, credit card, electronic fund transfers, online services, or payroll deductions [8]. Here's what you need to know:

- For donations under $250: Provide a bank record (like a canceled check, bank statement, or credit card statement) or a receipt from the charity. The receipt should include the charity’s name, the date, and the donation amount. For payroll deductions, you’ll need a pay stub, Form W-2, or a document from your employer showing the withheld amount, along with a pledge card or similar documentation from the charity [8].

- For donations of $250 or more: A bank record alone isn’t sufficient. You must obtain a contemporaneous written acknowledgment from the charity. This document should include the charity's name, the donation amount, and a statement indicating whether you received any goods or services in return. If you did, the charity must provide a good-faith estimate of their value [8].

"The law requires a 'contemporaneous written acknowledgment.' This doesn't mean you need the letter the same day you donated, but you do need it by the earlier of: 1. The date you actually file your tax return, or 2. The due date of your return (including extensions)." - SD Mayer [10]

Additionally, if you donate over $75 and receive something in return (e.g., a benefit dinner or merchandise), the charity must disclose the value of what you received [8].

Non-Cash Donation Documentation

Recording non-cash donations requires more thorough documentation. For all non-cash contributions, obtain a receipt from the charity that includes their name, the date, location, and a detailed description of the donated items [12]. Avoid vague descriptions like "a bag of clothes" - be specific, such as "men’s navy blue wool coat" or "four ceramic dinner plates" [12].

| Donation Value | Required Documentation | IRS Forms Needed |

|---|---|---|

| Under $250 | Receipt with charity name, date, and item description | None |

| $250 – $500 | Contemporaneous Written Acknowledgment (CWA) | None |

| $501 – $5,000 | CWA plus records of how/when property was acquired | Form 8283, Section A |

| Over $5,000 | CWA plus qualified appraisal | Form 8283, Section B |

| Over $500,000 | CWA plus qualified appraisal (must attach to return) | Form 8283, Section B |

If your total non-cash donations exceed $500 in a year, you’ll need to file IRS Form 8283, Section A [11]. For items or groups of similar items valued over $5,000, a qualified appraisal is required, and Form 8283, Section B, must be completed. The appraisal must be conducted no more than 60 days before the donation and no later than your tax return deadline [13]. Publicly traded securities are an exception and don’t require an appraisal [11].

"A qualified appraisal isn't just a quick estimate from a friend. It's a formal, detailed report prepared by a professional who meets specific IRS credentials." - DeductAble [3]

For vehicles valued over $500, the charity must provide Form 1098-C within 30 days of the donation or sale [13]. Additionally, clothing and household items must be in "good used condition or better" to qualify for deductions [9].

Avoiding Common Documentation Mistakes

To stay compliant, avoid these common pitfalls:

- Over-reliance on bank records: For donations of $250 or more, bank records alone aren’t sufficient; you need a written acknowledgment from the charity [9].

- Incorrect valuation of used items: Don’t use the original purchase price - determine the fair market value at the time of donation [12].

- Ignoring quid pro quo rules: Always subtract the value of goods or services received in return for your donation, such as event tickets or merchandise [8].

- Timing errors: Documentation obtained after filing your tax return invalidates the deduction [3].

Taking dated photos of donated items and keeping a detailed inventory can help defend against audits [12]. Before donating, confirm the charity’s 501(c)(3) status using the IRS Tax Exempt Organization Search tool [9]. Finally, retain all donation records for at least three years, though seven years is recommended for high-value or complex contributions [12].

With these records in place, you’ll be better prepared to manage your donations effectively.

Tools for Tracking and Managing Donations

Once you're up to speed on IRS compliance, the next step is making sure your donations are managed effectively to maximize tax benefits. Keeping track of both cash and non-cash donations throughout the year requires solid organization from the very first contribution. Many donors now rely on specialized third-party platforms that simplify valuation, maintain detailed records, and create IRS-compliant reports. These tools become especially handy once you’re familiar with the IRS's documentation requirements.

Using Deductible.me for Donation Management

Deductible.me (https://deductible.me) takes the hassle out of donation tracking with its AI-powered valuation and compliance features. Its photo-scanning technology can instantly identify donated items - whether it's a men’s navy wool coat or a set of four ceramic dinner plates - and assign fair market values based on thrift store pricing. This eliminates guesswork and helps you avoid common documentation mistakes.

The platform consolidates all donation types into a single dashboard. It tracks cash contributions, household goods, volunteer mileage (calculated at 14 cents per mile), stocks, and even vehicles [14]. Automated alerts notify you when your non-cash donations approach the $500 Form 8283 threshold or when a single item exceeds $5,000, ensuring you stay ahead of IRS documentation requirements.

When it’s time to file taxes, Deductible.me generates IRS-compliant reports that can be exported as PDFs or CSV files, making it easy to complete Schedule A. The platform offers two plans: a Free plan, which covers up to $500 in donation value - great for occasional donors - and a Premium plan at $2/month, which includes unlimited tracking, analytics for comparing annual giving trends, and tools to manage charitable contribution carryovers across multiple tax years.

Setting and Tracking Annual Giving Goals

Good record-keeping is just the beginning. Setting annual giving goals can help you make the most of your donation strategy. For example, the upcoming 2026 tax rules will only allow itemized charitable deductions for contributions exceeding 0.5% of your Adjusted Gross Income (AGI) [2]. By setting a yearly target, you can track your progress toward this threshold using a tool with a real-time dashboard.

Many donors are turning to a "bunching" strategy, where they combine several years of charitable giving into one tax year to surpass the AGI floor and maximize deductions [2]. Deductible.me makes this easier by letting you review past contributions and plan larger donations strategically. The platform also supports the new non-itemizer deduction: starting in 2026, even if you take the standard deduction, you can still claim up to $1,000 (for single filers) or $2,000 (for married couples filing jointly) for cash-only donations. Keeping separate records ensures you don’t miss out on this above-the-line deduction.

"Missing contemporaneous documentation is the most common reason charitable deductions get disallowed." - Charity Record [14]

Conclusion

Balancing cash and non-cash donations takes careful planning to align your financial goals with your charitable intentions. Cash donations are straightforward and provide an immediate impact, while non-cash assets, like appreciated stocks, offer added benefits. These include a deduction based on the full fair market value and the elimination of capital gains tax [1][16]. It’s also important to remember the adjusted gross income (AGI) limits, as excess contributions can be carried forward for up to five years [1][16].

Looking ahead, tax changes in 2026 will introduce a 0.5% AGI floor, meaning itemized deductions will only apply if your contributions exceed 0.5% of your AGI [16][17]. This makes strategies like bunching donations - combining multiple years of giving into one tax year - more important than ever. Even if you take the standard deduction, you can still claim up to $1,000 for single filers or $2,000 for joint filers in cash-only donations under the new above-the-line deduction [15][16].

Proper documentation is key to ensuring compliance and maximizing your tax benefits. Keep detailed records, including receipts and IRS forms, to safeguard your deductions in case of an audit [1][15]. Tools like Deductible.me can simplify this process by automating valuations, tracking IRS thresholds, and generating tax-ready reports for just $2/month with the Premium plan.

As John Rampton, CEO of Due, wisely notes:

"The tax benefit is the icing - not the actual cake. In the end, the real reward comes from supporting causes that matter to you in a smarter, more strategic manner" [17].

FAQs

How do I decide the best mix of cash vs. appreciated assets to donate?

Choosing between donating cash or appreciated assets comes down to tax advantages, the type of assets you have, and your overall goals. For instance, giving appreciated assets like stocks or real estate can help you sidestep capital gains taxes while potentially allowing you to claim a deduction based on the asset's fair market value. On the other hand, cash donations are straightforward, offer flexibility, and can create an immediate impact. To make the most of your contributions, consider consulting a tax advisor who can help craft a strategy that aligns with your financial and philanthropic goals.

What should I donate or sell first if an investment has lost value?

If an investment has decreased in value, you might want to think about selling it or donating it to claim the loss. If you choose to donate, you could qualify for a tax deduction based on the asset's fair market value (FMV) at the time of the donation. Keep in mind, the FMV may be less than what you originally paid for the investment, as specified by IRS rules.

When do I need Form 8283 or a qualified appraisal for non-cash gifts?

If you donate non-cash items worth more than $5,000, you'll need to complete Form 8283 and obtain a qualified appraisal to back up your deduction. This applies not only to individual items but also to groups of similar items. Additionally, if the total value of your non-cash donations exceeds $500 and any single item or group of similar items is valued over $5,000, these requirements are mandatory for proper documentation.