Checklist for Maximizing Charitable Deductions as a Couple

When it comes to charitable giving, couples filing jointly can save thousands on taxes with the right strategies. But new 2026 tax rules - like the $32,200 standard deduction, a 0.5% AGI floor, and a 35% AGI cap for high earners - make it harder to benefit from itemizing. Here's how to navigate these changes:

- Understand AGI Limits: Only donations exceeding 0.5% of AGI are deductible, and high earners face stricter limits.

- Decide on Standard vs. Itemized Deduction: Itemize only if your deductions (e.g., SALT, mortgage interest, charitable donations) exceed $32,200.

- Use Tax-Saving Strategies: Bunch donations, donate appreciated securities, or make Qualified Charitable Distributions (QCDs) if over 70½.

- Document Everything: Keep receipts, acknowledgments, and use tools like Deductible.me to stay IRS-compliant.

- Coordinate Federal and State Taxes: Align strategies to maximize deductions under both systems.

These steps can help you minimize your tax bill while supporting causes you care about.

2026 Charitable Deduction Rules and AGI Limits for Married Couples Filing Jointly

1. Know Your Filing Status and AGI Limits

1.1 File Jointly to Combine AGI

When married couples file jointly, their individual incomes are merged into a single Adjusted Gross Income (AGI). This combined AGI becomes the basis for calculating charitable deductions. Filing jointly simplifies meeting threshold requirements by pooling incomes.

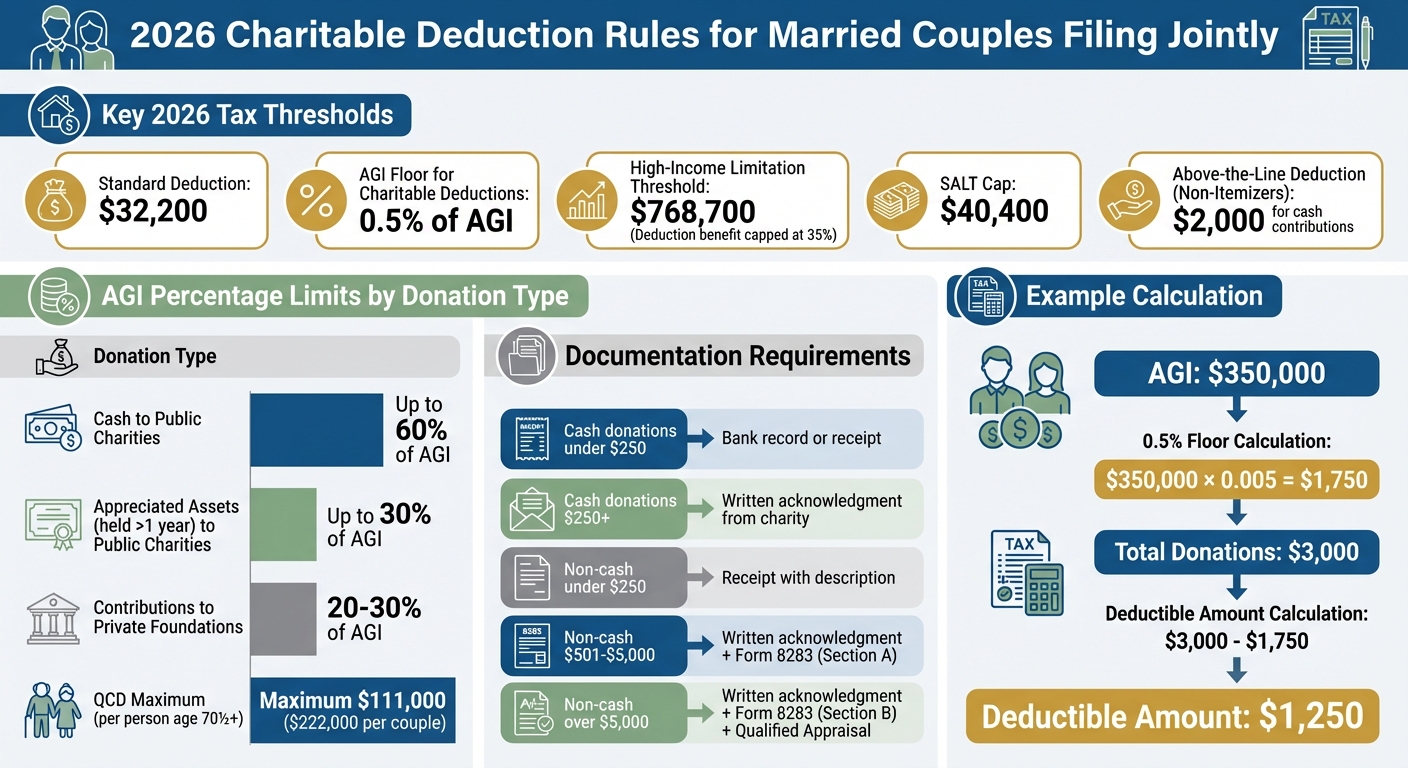

For the 2026 tax year, married couples filing jointly and taking the standard deduction can claim an above-the-line deduction of up to $2,000 for cash contributions to qualified public charities [8]. For those who itemize, the combined AGI determines both donation percentage limits and the 0.5% floor.

1.2 Calculate Percentage AGI Limits for Donations

The IRS restricts deductible amounts based on the type of donation and the recipient organization. For cash contributions to public charities, deductions can go up to 60% of your combined AGI [9]. For example, with an AGI of $200,000, cash deductions could total up to $120,000. However, if you donate appreciated assets held for more than a year, the deductible limit drops to 30% of AGI [2], which in this case would be $60,000. Contributions to private foundations are subject to even tighter limits, usually between 20% and 30% of AGI [9].

1.3 Account for the 0.5% AGI Floor

Starting in 2026, only contributions that exceed 0.5% of your AGI will qualify as deductible [10]. This floor is calculated on the total annual donations rather than individual gifts [11].

"Beginning in 2026, if you itemize deductions on your tax return, you can only deduct charitable contributions that exceed 0.5% of your Adjusted Gross Income (AGI)." - Victor, Accountant, DRS Accounting PC [8]

To figure out the deductible portion of your donations, multiply your combined AGI by 0.005. For instance, tax professionals at Capaldi Reynolds & Pelosi explained that a couple with an AGI of $350,000 and total charitable contributions of $3,000 would have a floor of $1,750 (350,000 × 0.005). This means only $1,250 of their donations could be deducted [7].

High-income earners face an additional restriction. If your taxable income exceeds $768,700 in 2026, the tax benefit of your deductions is limited to 35%, even if you are in the 37% marginal tax bracket [6]. For example, a couple with an AGI of $900,000 and $7,500 in donations would have a 0.5% floor of $4,500, leaving $3,000 as potentially deductible. After applying the high-income limitation, which reduces this amount by $162.16, the final deduction would be $2,837.84 [7].

From here, consider whether itemizing or opting for the standard deduction aligns better with your financial goals.

sbb-itb-e723420

Making donations in 2026: What new tax rules mean for charitable giving now and later

2. Choose Between Itemizing and Standard Deduction

Deciding whether to itemize your deductions or stick with the standard deduction can make a big difference in your tax savings.

2.1 Compare Your Itemized Deductions to the Standard Deduction

The choice between itemizing and taking the standard deduction boils down to a straightforward comparison. For the 2026 tax year, the standard deduction for married couples filing jointly is $32,200[1]. You should only itemize if your total deductible expenses exceed this amount.

To calculate your potential itemized deductions, add up expenses like SALT (state and local taxes), mortgage interest, qualifying medical costs, and charitable donations above the 0.5% AGI floor. Under the One Big Beautiful Bill Act, the SALT cap for 2026 increases to roughly $40,400[1], and mortgage interest remains deductible on loans up to $750,000[14].

Here’s an example: If you pay $20,000 in mortgage interest, reach the SALT cap, and donate $2,000 to charity, your total itemized deductions would be $62,400 - well above the $32,200 standard deduction. However, it’s worth noting that fewer than 10% of taxpayers currently itemize because of the high standard deduction threshold[12].

If your itemized deductions don’t exceed the standard deduction, there are still ways to benefit from tax breaks without itemizing.

2.2 Use the Above-the-Line Deduction for Non-Itemizers

Even if your itemizable expenses fall short of $32,200, you can still take advantage of tax benefits for charitable giving. Couples claiming the standard deduction can deduct up to $2,000 for cash contributions made to qualified public charities[13].

"If you do not itemize and instead claim the standard deduction, you may still deduct up to $1,000 (single) or $2,000 (married filing jointly) for cash contributions to qualified public charities." - John J. Moller, CPA[7]

This deduction applies only to direct cash donations to 501(c)(3) organizations. Contributions to donor-advised funds or private foundations don’t qualify. To ensure your donation is eligible, use the IRS Tax Exempt Organization Search tool, and keep documentation such as bank statements or written acknowledgments from the charity.

3. Plan Your Giving Strategy for Maximum Deductions

Once you've decided on your deduction method, timing your contributions strategically can help you maximize tax benefits. By aligning your donations with IRS rules and thresholds, you can potentially increase your deductions under current tax regulations.

3.1 Use the Bunching Strategy

The bunching strategy involves consolidating donations from multiple years into one tax year to exceed the $32,200 standard deduction threshold. In "off" years, you can then take the standard deduction instead[16][17]. This approach works well under the One Big Beautiful Bill Act, which introduced a 0.5% AGI floor for charitable deductions, as it minimizes the impact of this rule to a single year[4].

"Concentration beats distribution when the standard deduction is high." - FindCPA[4]

Here’s an example: A married couple in 2026 with $10,000 in SALT and $6,000 in mortgage interest bunched three years of $10,000 annual donations into a single year using a Donor-Advised Fund (DAF). This brought their itemized deductions to $46,000, surpassing the standard deduction by $13,800 for that year. In the following years, they used the standard deduction instead[4].

DAFs are particularly useful for this strategy, as they let you take an immediate deduction for the full contribution while spreading out grants to charities over time[16][17]. To make the most of your "giving year", combine bunched donations with other itemized deductions like mortgage interest and SALT[4].

Timing tip: Consider bunching donations during high-income years, such as when you receive a large bonus or complete a Roth conversion. This offsets higher tax brackets and increases efficiency. Additionally, donating appreciated securities instead of cash can help you avoid capital gains tax while deducting the full fair market value (up to 30% of AGI)[4][17].

3.2 Make Qualified Charitable Distributions (QCDs)

If you or your spouse are at least 70½ years old, Qualified Charitable Distributions (QCDs) offer another tax-efficient way to give. QCDs allow you to transfer funds directly from your IRA to a qualified charity, excluding the amount from your Adjusted Gross Income (AGI)[18][19].

"If you are 70-1/2 or older with a traditional IRA, always use QCDs before writing personal checks or itemizing charitable deductions." - FindCPA[4]

For 2026, the maximum QCD limit is $111,000 per person, meaning a married couple could donate up to $222,000 annually if both meet the age requirement[18][21]. Unlike standard deductions, QCDs provide tax benefits even if you take the standard deduction. They also count toward your Required Minimum Distribution (RMD)[18][20].

To qualify, the funds must be transferred directly from your IRA custodian to the charity. If the check is made payable to you first, the distribution will count as taxable income instead of a QCD[18][20]. For example, in 2025, a couple used a $6,000 QCD to reduce their AGI and stay below a state tax threshold, saving $3,897 in taxes. This made their $6,000 donation effectively cost just $2,103[19].

Important note: QCDs cannot be made to Donor-Advised Funds, private foundations, or supporting organizations, and they must be completed by December 31 to count for that tax year[18][20].

3.3 Track and Carry Forward Excess Deductions

If your charitable contributions exceed AGI limits for a single tax year, you can carry the excess forward for up to five years[17][4]. This is especially useful when making large donations or using the bunching strategy.

Carryforwards retain their original "character", meaning contributions of appreciated property subject to the 30% AGI limit will still be bound by that limit in future years[4]. However, under the One Big Beautiful Bill Act, amounts disallowed by the 0.5% AGI floor cannot be carried forward - they are permanently lost[4].

For example, in a 2026 scenario, a donor with a $200,000 AGI donated $80,000 in appreciated stock. Since the limit for long-term capital gain property is 30% of AGI ($60,000), they could only deduct $60,000 that year. The remaining $20,000 was carried forward for the next tax year[4].

To manage carryforwards effectively, keep detailed records of cash and non-cash contributions, as they have different AGI percentage limits - 60% for cash and 30% for non-cash[4]. Also, ensure you have a Contemporaneous Written Acknowledgment (CWA) for any gift of $250 or more, as the IRS requires this documentation to allow carryforwards[17][4].

4. Maintain Proper Documentation for Donations

Once you've planned your giving strategy, proper documentation becomes essential to secure those tax benefits. Keeping accurate records ensures your charitable deductions meet IRS standards. Since documentation requirements differ based on the type and value of your donation, it’s important to understand these rules, especially for married couples aiming to optimize their tax filings.

"In my 15 years advising clients, the most common audit triggers are poorly documented noncash gifts and missing acknowledgments for donations of $250 or more." - Finhelp.io [22]

Here’s what you need to know about documenting cash and non-cash contributions.

4.1 Keep Receipts and Acknowledgments

The IRS sets clear rules about acceptable proof for charitable giving. For cash donations, you’ll need a bank record (like a canceled check, bank statement, or credit card statement) or a written receipt from the organization. If your donation is $250 or more, a "contemporaneous written acknowledgment" from the charity is required [23][25].

When it comes to non-cash donations, the requirements are a bit more detailed. Contributions under $250 require a receipt from the charity that includes a description of the items, along with your own notes on their condition and fair market value [22]. If the total value of your non-cash donations exceeds $500, you’ll need to file IRS Form 8283 (Section A) with your tax return. For donations exceeding $5,000, a qualified appraisal and completion of Section B of Form 8283 are necessary [23][24].

Here’s a quick breakdown of the documentation requirements:

| Type of Donation | Value Threshold | Required Documentation |

|---|---|---|

| Cash | Under $250 | Bank record or receipt |

| Cash | $250 or more | Written acknowledgment from charity |

| Non-Cash | Under $250 | Receipt with description, date, and location |

| Non-Cash | $501 – $5,000 | Written acknowledgment + Form 8283 (Section A) |

| Non-Cash | Over $5,000 | Written acknowledgment + Form 8283 (Section B) + Qualified Appraisal |

You must obtain the written acknowledgment by the time you file your tax return or the return's due date, whichever comes first [25].

"If you file your return without having the [acknowledgment] letter in hand, you cannot go back and get it later to fix a mistake if audited." - SD Mayer [25]

For items like clothing and household goods, the IRS requires them to be in "good used condition or better" [26]. To strengthen your records, photograph the items before donating and maintain a detailed inventory. Be specific in your descriptions - writing "men's cotton dress shirt" instead of just "shirt" will help solidify your documentation [22].

While following IRS guidelines is vital, modern tools can make record-keeping easier and more efficient.

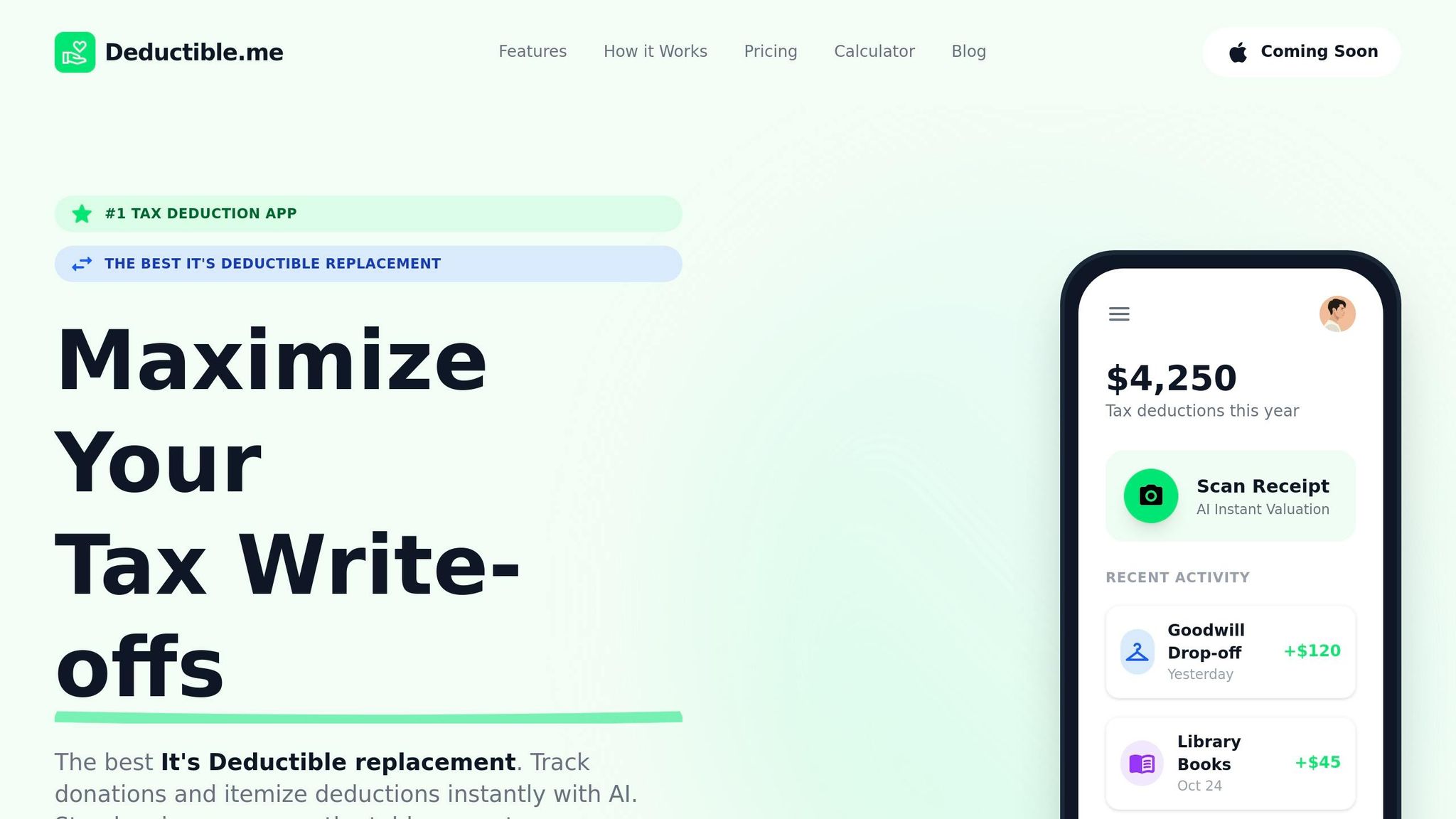

4.2 Use Deductible.me for IRS Compliance

If you’re managing multiple donations, digital tools like Deductible.me can simplify the process. This app uses AI to estimate fair market values for non-cash items based on their condition, saving you the hassle of researching prices manually [3].

With Deductible.me, you can capture photos of your donations as you make them, creating a digital record that’s ready for any audit [3]. The app also allows you to upload and link images of paper acknowledgments or PDF receipts to each donation, creating a secure, centralized repository [3].

When tax season rolls around, the app generates IRS-compliant, itemized reports for your tax preparer. It even prompts you to categorize items as "Excellent", "Good", or "Fair", which is essential for determining their deductible value [3]. For couples filing jointly, both partners can log donations into a single account from different devices, ensuring nothing gets overlooked [3].

"DeductAble ensures every contribution is logged with the right details from the get-go, building a solid foundation for your tax filings and helping you maximize your itemized deductions." - DeductAble.ai [3]

The Premium plan, priced at $2 per month, offers unlimited donation tracking and generates IRS-compliant reports ready for Form 8283. The free tier, on the other hand, allows tracking up to $500 in donation value [3]. By using tools like this, you can ensure every donation is accurately documented and contributes to your overall deductions.

5. Coordinate Federal and State Tax Strategies

Once your records are well-organized and your giving strategy is in place, it's time to align your federal and state tax approaches. While federal rules establish the foundation for charitable deductions, state tax laws can significantly influence the ultimate benefit. Since many states deviate from federal guidelines, understanding these differences is crucial to optimizing your tax outcomes.

5.1 Review State-Specific Charitable Deduction Rules

State policies on charitable deductions vary widely. Some states, like Arizona, Idaho, and Oregon, align closely with federal rules and calculate deductions based on your Adjusted Gross Income (AGI) [28]. However, many others, such as California and New York, impose additional limits or restrictions on deductions.

For instance:

- California limits cash gift deductions to 50% of federal AGI, as opposed to the federal 60% limit [27].

- New York reduces charitable deductions by 25%–50% for couples earning over $1 million and up to 75% for those with AGI exceeding $10 million [27].

- Maine phases out deductions entirely for married couples with AGI between $194,300 and $388,650 [27].

If you receive a state tax credit for a donation, you must reduce your federal deduction by the value of the credit - unless the credit is 15% or less [31].

"When a state gives you a tax credit, the IRS views that credit as a valuable benefit you received... your payment to the charity is not considered a pure gift. It is part gift and part purchase." - TaxShark [31]

Before contributing to state-specific programs like scholarship funds or conservation easements, confirm whether the benefit is a credit or a deduction. If the credit exceeds 15%, expect a reduced federal deduction [31].

Once you've accounted for state-specific rules, adjust your state tax payments to further enhance your overall tax strategy.

5.2 Balance SALT and Charitable Deductions

Combining federal and state strategies can make your giving plan more effective. A key factor in this process is balancing your SALT (State and Local Tax) and charitable deductions to maximize itemized benefits. For 2025, the federal SALT cap is set at $40,000 per tax return [29][30]. This higher cap allows more taxpayers, especially couples, to surpass the $31,500 standard deduction threshold, making charitable contributions even more impactful [30][32].

Timing your state tax payments is essential. For example, paying your Q4 state income tax estimate by December 31 ensures you hit the $40,000 SALT limit. Consider the case of Alex and Jordan, who paid $28,000 in property taxes and $12,000 in state income taxes before December 31, 2025. By doing so, they fully utilized the SALT deduction. If they had delayed the $12,000 payment until January 2026, they would have missed out on that deduction for the 2025 tax year [29].

Business owners have additional options, such as the Pass-Through Entity Tax (PTET), which allows them to pay state income taxes through their business. This approach bypasses the personal SALT cap and reduces AGI, potentially keeping it below the $500,000 threshold where the $40,000 SALT cap starts to phase out [29][31].

"Households near the phase-out thresholds should model adjusted gross income (AGI) carefully to preserve full benefit." - Tax Specialty [30]

Conclusion

Boosting your charitable deductions requires thoughtful planning and meticulous record-keeping. Start by confirming that your chosen charities qualify as 501(c)(3) organizations using the IRS Tax Exempt Organization Search tool [5]. Then, evaluate whether your total itemized deductions surpass the $32,200 standard deduction for married couples in 2026 [4]. Strategies like donation bunching or using donor-advised funds can help maximize your deductions. Keep in mind that only contributions exceeding the 0.5% AGI floor will count as itemized deductions [4].

Accurate documentation is non-negotiable. Missing details, like a donation date or acknowledgment letter, can invalidate your deduction during an audit [3]. Tools like Deductible.me simplify this process by logging donations, generating IRS-compliant reports, and even providing AI-powered valuations for non-cash items such as clothing and household goods. For gifts over $250, the platform ensures you receive the necessary contemporaneous written acknowledgments [3]. These practices are essential for meeting both federal and state requirements.

"Giving to charity should come from the heart, not from trying to game your taxes. But if you're going to give anyway... there's no reason not to structure it in a way that also benefits you financially." - Randy Martin, CPA [5]

State tax rules can complicate things further. For example, if a state tax credit exceeds 15% of your donation, your federal deduction must be reduced accordingly [15]. Additionally, timing your state tax payments to meet the $40,400 SALT cap in 2026 can determine whether itemizing is worthwhile [33]. Balancing federal and state strategies throughout the year is key to maximizing your financial benefits.

FAQs

Will we save more by itemizing or taking the $32,200 standard deduction?

For 2026, the standard deduction for married couples filing jointly is $32,200. If your total itemized deductions - such as charitable contributions - add up to more than this amount, itemizing could save you more on your taxes. Otherwise, sticking with the standard deduction might be the smarter choice. Take the time to review your deductions thoroughly to decide which option works best for your situation.

How does the new 0.5% of AGI floor change what we can deduct for donations?

Starting in 2026, there’s a new rule for charitable contributions: only donations exceeding 0.5% of your adjusted gross income (AGI) will be deductible if you itemize. Contributions below this threshold won’t count toward your deductions anymore. To make the most of this change, you’ll need to keep a close eye on your donations and ensure they go beyond the 0.5% AGI mark before claiming them.

When should we use QCDs, bunching, or appreciated stock to lower our taxes most?

Using Qualified Charitable Distributions (QCDs), grouping donations, or giving appreciated stock are strategies that can lower your tax bill, depending on your financial goals and circumstances.

- Qualified Charitable Distributions (QCDs): Ideal if you're 70½ or older and want to lower taxable income from your IRA.

- Grouping donations: Helps you exceed the standard deduction by combining multiple years of charitable contributions into one.

- Appreciated stock: Donating stocks that have gone up in value lets you avoid capital gains taxes while deducting the full market value of the stock.