How Charitable Bunching Works with Donor-Advised Funds

If you donate to charity regularly but take the standard deduction, you could be missing out on tax savings. For 2026, the standard deduction is $32,200 for married couples filing jointly and $16,100 for single filers. Unless your itemized deductions exceed these amounts, your charitable contributions won’t lower your tax bill.

Charitable bunching solves this by letting you combine multiple years of donations into one tax year to surpass the standard deduction. Using a donor-advised fund (DAF) makes this strategy even more effective, allowing you to claim a large deduction upfront while distributing funds to charities over time.

Here’s how it works:

- Make a large, single contribution to a DAF: Fund it with cash or appreciated assets (like stocks) to maximize deductions and avoid capital gains tax.

- Claim the tax deduction in one year: Push your itemized deductions above the standard threshold.

- Distribute grants to charities later: Support your favorite causes consistently, even in years you take the standard deduction.

This strategy is particularly useful in high-income years or when planning for changes in tax laws, such as the new 0.5% AGI floor for charitable deductions starting in 2026.

How Donor-Advised Funds Can Make Giving Easier (and Lowers Your Taxes)

sbb-itb-e723420

Tax Deduction Limits for Charitable Contributions

Before diving into donation strategies like bunching, it’s crucial to understand the IRS rules on how much you can deduct in a single tax year. These limits are tied to your Adjusted Gross Income (AGI) and depend on whether you're donating cash or appreciated assets.

"The amount of charitable cash contributions taxpayers can deduct on Schedule A as an itemized deduction is limited to a percentage (usually 60 percent) of the taxpayer's adjusted gross income (AGI)."

If your deductions exceed these AGI limits, don’t worry - they can be carried forward for up to five years [6]. Let’s break down the specifics for cash donations and appreciated assets.

Cash Donation Deduction Limits

For donations made in cash, you can generally deduct up to 60% of your AGI when contributing to public charities or donor-advised funds [6]. However, if you give to certain private foundations, veterans' organizations, fraternal societies, or cemetery organizations, the limit drops to 30% of your AGI.

Here’s an example: Say your AGI is $100,000 and you donate $10,000. You can deduct $9,500 immediately, while the remaining $500 (0.5% of AGI) is carried forward to future years [7].

"Starting in 2026, single taxpayers can deduct up to $1,000 per year in cash charitable contributions without itemizing. Married individuals filing jointly can deduct $2,000."

To qualify for a deduction in a specific tax year, make sure your donation is processed - whether by check, credit card, or electronic payment - by December 31 [8].

Appreciated Asset Deduction Limits

Donating appreciated assets, such as stocks or real estate held for more than one year, comes with its own set of rules. These contributions are deductible up to 30% of your AGI, based on the asset’s full fair market value, all while avoiding capital gains tax on the appreciation [2]. However, assets held for one year or less are treated as ordinary income property, and the deduction is limited to the lesser of the asset’s cost basis or fair market value [2].

To maximize your deduction when giving appreciated assets, consider increasing your AGI during the donation year. For instance, exercising stock options or doing a Roth conversion can boost your AGI, allowing you to claim a larger deduction under the 30% limit [2].

Cash vs. Appreciated Asset Deduction Limits

Here’s a quick side-by-side comparison to help you decide which type of contribution aligns with your strategy:

| Feature | Cash Contributions | Appreciated Assets (Long-Term) |

|---|---|---|

| AGI Limit | 60% | 30% |

| Tax Benefit | Lowers taxable income | Lowers taxable income and avoids capital gains tax |

| Valuation | Full cash amount | Fair market value |

| Best For | Immediate tax benefits | Preserving wealth and reducing capital gains tax |

If you’re in a high-income year - like after receiving a large bonus or selling a business - donating appreciated securities can provide a dual advantage. Not only does it reduce taxable income, but it also eliminates capital gains tax, making it a smart move for bunching multiple years of donations into one deduction [2].

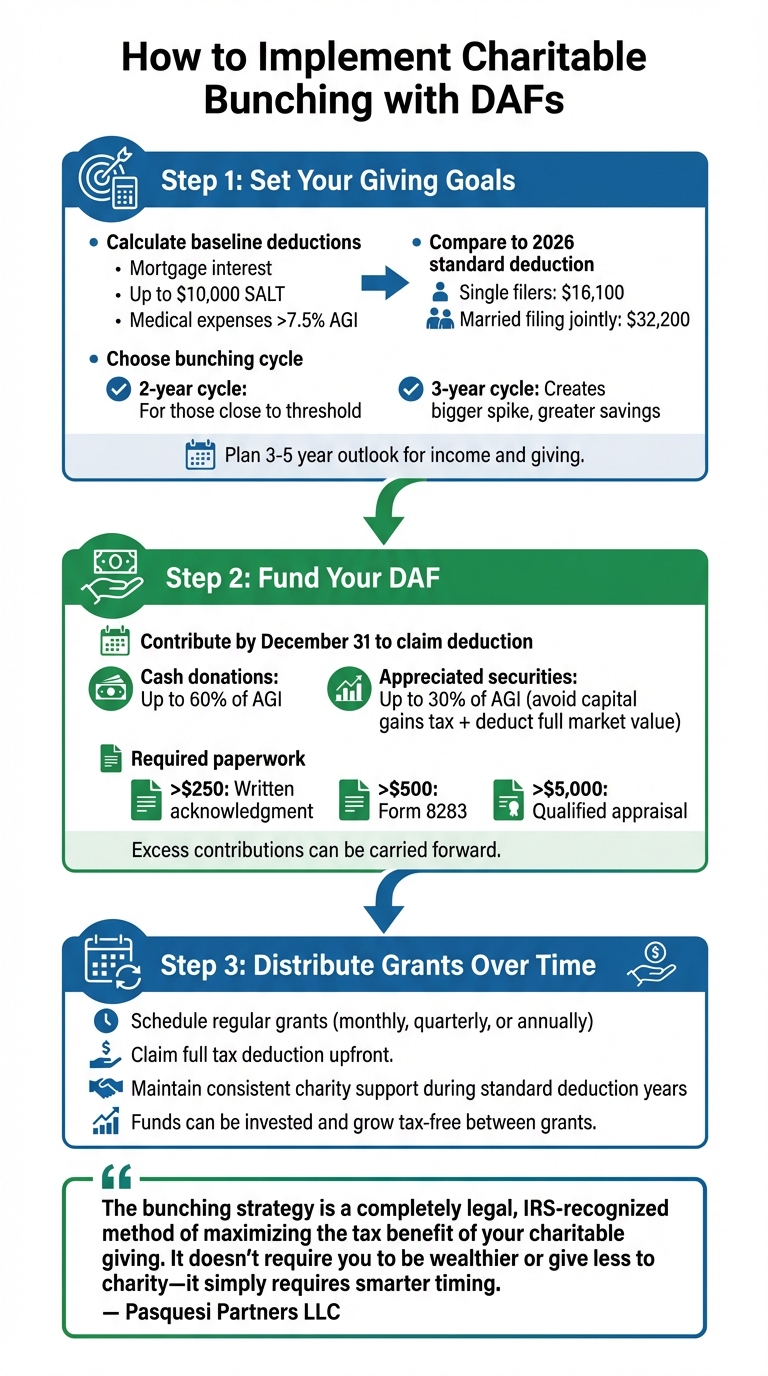

How to Implement Charitable Bunching with DAFs

3-Step Process for Implementing Charitable Bunching with Donor-Advised Funds

You can maximize tax savings with donor-advised funds (DAFs) by following three steps: set your giving goals, fund your DAF, and distribute grants over time.

Step 1: Set Your Giving Goals

Start by calculating your baseline deductions, which include items like mortgage interest, up to $10,000 in state and local taxes, and medical expenses exceeding 7.5% of your adjusted gross income (AGI) [10]. Compare this total to the 2026 standard deduction: $16,100 for single filers or $32,200 for married couples filing jointly [3]. If your non-charitable deductions don’t meet the threshold, figure out how much additional charitable giving is needed to go beyond it.

Next, decide on a bunching cycle. A two-year cycle is often effective if you're close to the standard deduction threshold, while a three-year cycle can create a bigger spike in itemized deductions and may result in greater tax savings [9][10]. When planning, consider a 3-to-5 year outlook for income and charitable commitments. For instance, if you anticipate a $100,000 bonus in September 2025, that could be an ideal year to bunch contributions and reduce the impact of a higher marginal tax rate [9].

"The bunching strategy is a completely legal, IRS-recognized method of maximizing the tax benefit of your charitable giving. It doesn't require you to be wealthier or give less to charity - it simply requires smarter timing."

Once your goals are clear, the next step is funding your DAF to lock in your tax deduction.

Step 2: Fund Your DAF

After identifying your bunching year, make contributions to your DAF by December 31 to claim the deduction. Donating long-term appreciated securities can be particularly advantageous - you avoid capital gains tax and can deduct the full fair market value, up to 30% of your AGI [5][9]. Cash donations, on the other hand, are typically limited to 60% of your AGI [1][9].

Be sure to handle the paperwork properly. For donations over $250, secure written acknowledgment. For non-cash gifts above $500, file Form 8283, and for gifts exceeding $5,000, obtain a qualified appraisal [9]. If your contributions exceed annual limits, you can carry them forward under IRS guidelines [1][9].

With your DAF funded, the next focus is on distributing grants.

Step 3: Distribute Grants Over Time

Once your DAF is set up, you can schedule regular grants - monthly, quarterly, or annually - to provide ongoing support to your chosen charities. This method allows you to claim the full tax deduction upfront while ensuring consistent financial support for charities during the years you take the standard deduction [1][3].

Additionally, funds in your DAF can be invested and grow tax-free between grants, potentially increasing the total amount available for future donations [3].

"Bunching doesn't mean you have to stop supporting your favorite charities annually. You can maintain giving consistency with a donor-advised fund... ensuring you maintain steady support while optimizing your tax benefits."

Charitable Bunching Examples

Here’s a look at how different bunching strategies stack up against annual giving. These examples highlight the potential tax benefits of bunching.

Annual Giving vs. 2-Year Bunching

Meet Alison and James, a married couple who typically itemize $28,000 in deductions each year. This includes $15,000 in charitable donations and $13,000 from other deductions like mortgage interest and state taxes. Without bunching, their total deductions over two years equal $63,700, which matches the standard deduction for that period [1].

Now, let’s say they bunch two years of donations - $30,000 - into a donor-advised fund (DAF) in 2025. This pushes their 2025 itemized deductions to $43,000. In 2026, they take the standard deduction of $32,200. Altogether, this strategy boosts their total deductions to $75,200, giving them an extra $11,500 in deductions [1].

| Strategy | Year 1 Deduction | Year 2 Deduction | Total 2-Year Deduction | Additional Benefit |

|---|---|---|---|---|

| Annual Giving | $31,500 (Standard) | $32,200 (Standard) | $63,700 | $0 |

| 2-Year Bunching | $43,000 (Itemized) | $32,200 (Standard) | $75,200 | $11,500 |

This example shows how a simple two-year bunching plan can increase deductions. But what happens when you take it a step further? Let’s look at a three-year bunching strategy.

3-Year Bunching with Appreciated Assets

Now imagine a married couple who donates $20,000 annually and has $25,000 in other deductions. If they itemize in 2026, their deductions exceed the standard deduction by $12,800, saving $4,480 based on a 35% tax rate [3].

Instead of donating annually, they decide to bunch three years of donations - $60,000 - into one year, using appreciated stock rather than cash. This pushes their itemized deductions to $85,000, which is $52,800 above the standard deduction. Over three years, this strategy could save them $17,167.50 in taxes. On top of that, by donating appreciated stock, they avoid paying capital gains tax, potentially saving another 23.8% on the stock’s gains [3][11].

"One tax-efficient strategy is called bunching, where you group multiple years of deductions into a single year to surpass the standard deduction, which can also be especially beneficial in a high-income year or during pre-retirement."

- Fidelity Charitable [3]

These examples highlight how bunching, especially when paired with tools like donor-advised funds or appreciated assets, can maximize tax benefits while supporting charitable giving.

Track and Optimize Your Giving with Deductible.me

Keeping tabs on your charitable giving can get complicated, especially when trying to maximize tax benefits through strategies like bunching. You need to track how your itemized deductions stack up against the standard threshold and the AGI floor set by recent laws. That’s where Deductible.me comes in - offering tools that make managing your donations easier and more efficient. Here’s how it helps strategic donors stay on top of their giving.

Donation Tracking with Deductible.me

Deductible.me streamlines the process of tracking your charitable contributions over several years. By combining your charitable donations with other deductions - like mortgage interest and the $10,000 SALT cap - it calculates your itemized deductions in real time. This lets you see if a bunching strategy is worth pursuing[3][2]. The platform is particularly helpful when managing contributions to Donor-Advised Funds (DAFs) and making grant recommendations[4][3].

Another key feature is its ability to handle the five-year carryforward rule. If your deductions exceed the annual AGI limits - 60% for cash donations and 30% for appreciated assets - Deductible.me keeps track of the excess for future use[1][2]. For high-income earners in the 37% tax bracket, this is even more critical as the deduction cap drops to 35% in 2026. With this tool, you can ensure you’re making the most of every tax benefit[2].

AI-Powered Item Valuation

When donating non-cash items to your DAF, accurate valuation is essential to meet IRS requirements. Deductible.me’s AI-powered valuation tool simplifies this by analyzing images of your donated items and providing fair market value estimates. This is especially helpful for appreciated assets, which are subject to the 30% AGI deduction limit[1][12].

Advanced Analytics to Guide Your Giving

The platform also features an analytics dashboard that offers a clear picture of your giving patterns over multiple years. You can see how bunching strategies affect both your charitable contributions and tax savings. Set annual giving goals, track your progress, and adjust your approach as your income or AGI changes. These insights not only help you stay compliant but also ensure you’re maximizing the benefits of your giving strategy[1][2].

Conclusion

To wrap up, merging charitable bunching with donor-advised funds offers a powerful way to maximize tax benefits while maintaining steady support for the causes you care about. By grouping several years of donations into one tax year, you can surpass the 2026 standard deduction thresholds - $16,100 for single filers and $32,200 for married couples filing jointly [3]. From there, a donor-advised fund allows you to distribute grants to charities at your own pace.

The benefits grow even more when you donate appreciated securities instead of cash.

"For high-income donors, acting in 2025 before new rules take effect in 2026 could preserve significantly more of their wealth for charitable purposes."

- Joseph Powanda, CFP®, CPWA® [2]

With the 2026 changes introducing a 0.5% AGI floor and a 35% deduction cap for top earners, timing your bunching strategy during high-income years - such as after a business sale or a Roth conversion - can make an even bigger impact [2][9].

Deductible.me simplifies this process by tracking itemized deductions in real time, managing the five-year carryforward rule, and using AI to value non-cash donations. Whether you're bunching $30,000 over two years or donating $150,000 in appreciated stock, this tool ensures you stay compliant while maximizing your tax savings. Together, these strategies create a well-rounded, efficient approach to giving.

FAQs

How do I know if bunching will beat the standard deduction for me?

To figure out if bunching your donations is more advantageous than taking the standard deduction, compare your total itemized deductions (including charitable contributions) to the IRS standard deduction. If your itemized deductions are higher than the standard deduction in a given year, concentrating your donations in that year might result in bigger tax savings.

Should I fund my DAF with cash or appreciated stock?

Donating appreciated stock to a donor-advised fund (DAF) can be a smarter tax move compared to giving cash. Here's why: when you donate stock that's gone up in value, you skip paying capital gains taxes on the appreciation. Plus, you can still claim a charitable deduction based on the stock's fair market value. While cash donations are straightforward, they don't come with these added tax perks. If you own securities that have gained value, gifting them is often the best way to maximize tax savings - especially during high-income years or when the appreciation is substantial.

What happens if my charitable deduction exceeds the AGI limit?

If your charitable deduction surpasses the adjusted gross income (AGI) limit, you don’t lose the excess. Instead, you can carry it forward and deduct it in future tax years. This carryover is valid for up to five years, giving you multiple chances to apply the deduction during that period.