QCD Rules for 2026 Explained

Qualified Charitable Distributions (QCDs) are a tax-efficient way to donate to charity directly from your IRA while reducing your taxable income. In 2026, QCDs are more advantageous due to new tax laws under the One Big Beautiful Bill Act (OBBBA) that limit traditional charitable deductions. Here's what you need to know:

- Eligibility: You must be at least 70½ years old to make a QCD. Eligible accounts include Traditional IRAs, Inherited IRAs, and Rollover IRAs. Employer-sponsored plans like 401(k)s do not qualify unless rolled into an IRA.

- Annual Limit: You can transfer up to $111,000 per person ($222,000 for married couples) directly to a qualified 501(c)(3) organization without triggering taxable income.

- Tax Benefits: QCDs lower your Adjusted Gross Income (AGI), helping you avoid higher tax brackets, reduce Medicare premiums, and decrease the taxable portion of Social Security benefits. They also count toward satisfying your Required Minimum Distribution (RMD) if you're 73 or older.

- Restrictions: QCDs cannot be made to donor-advised funds, private foundations, or supporting organizations. Contributions must be sent directly from your IRA custodian to the charity.

To maximize the benefits, initiate your QCD early in the year, ensure the charity qualifies, and keep proper documentation. Missing deadlines or donating to ineligible organizations can disqualify the tax benefits.

QCDs are a powerful tool for tax planning and charitable giving in 2026. By following these rules, you can save on taxes while supporting causes you care about.

Who Qualifies for QCDs in 2026

Minimum Age Requirement

To be eligible for a Qualified Charitable Distribution (QCD) in 2026, you must be at least 70½ years old on the exact date the funds leave your IRA. Timing is critical - if the distribution occurs even a day before you reach 70½, it will be treated as taxable income.

"A common misunderstanding is that QCDs cannot be made until RMDs begin at age 73. In fact, the eligibility age for QCDs stays 70½." – Elmer Howard, Prosperity Financial Accounting [9]

This is an important distinction. While Required Minimum Distributions (RMDs) now start at age 73 or 75, depending on your birth year, QCDs can still begin earlier, at 70½. For inherited IRAs, the beneficiary's age is what determines eligibility - not the age of the original account holder.

Which Retirement Accounts Qualify

Once you meet the age requirement, the type of IRA account you have determines whether you can make a QCD. Traditional IRAs, Inherited IRAs, and Rollover IRAs are eligible. Roth IRAs also qualify, though they are rarely used for QCDs since distributions from Roth accounts are already tax-free.

SEP IRAs and SIMPLE IRAs can only be used for QCDs if employer contributions for the year have stopped.

Workplace retirement plans like 401(k)s, 403(b)s, and 457(b) plans do not qualify for direct QCDs. If your savings are in one of these accounts, you’ll need to roll the funds into a Traditional IRA first. Once the rollover is complete and you meet the age requirement, you can proceed with QCDs from the new IRA.

sbb-itb-e723420

QCD Limits and Adjustments for 2026

Annual $111,000 QCD Limit

Starting in 2026, individuals can transfer up to $111,000 from their IRA to a charity without triggering taxable income.

"For tax year 2026, the per-taxpayer limit for Qualified Charitable Distributions (QCDs) has been increased for inflation to $111,000, up from $108,000 in 2025." – Lincoln Community Foundation [14]

For married couples filing jointly, the combined limit reaches $222,000, but each spouse must distribute funds from their own IRA to take full advantage of this household limit.

It's important to note that if you go over the $111,000 limit in a single year, the excess will be treated as taxable income. Additionally, you can't carry over any unused amount to offset future Required Minimum Distributions.

There’s also a one-time QCD option for funding split-interest vehicles like Charitable Gift Annuities or Charitable Remainder Trusts. This comes with a separate limit of $55,000 and is available only once in your lifetime [14]. This limit is entirely separate from the annual QCD cap.

Next, let’s look at how inflation adjustments impact these limits.

Inflation Adjustments to QCD Limits

Under the SECURE 2.0 Act, the QCD limit is now indexed for inflation, ensuring it increases incrementally each year. What started as a $100,000 baseline in 2024 has risen steadily, with the 2026 limit set at $111,000, up from $108,000 in 2025 [14].

"Beginning in 2026, the annual limit for Qualified Charitable Distributions is $111,000 per individual, indexed for inflation under the SECURE 2.0 Act." – Bruce Keeler, Professional Advisor [13]

The one-time split-interest election limit also benefits from inflation adjustments, increasing from $54,000 in 2025 to $55,000 in 2026.

| QCD Limit Category | 2025 Limit | 2026 Limit |

|---|---|---|

| Annual Limit (Per Individual) | $108,000 | $111,000 |

| Annual Limit (Married Couple) | $216,000 | $222,000 |

| One-time Split-Interest Election | $54,000 | $55,000 |

When planning your charitable contributions, always check the updated limits for the current tax year. The IRS typically announces these figures each fall for the following year.

Tax Benefits of QCDs in 2026

How QCDs Reduce Your AGI

QCDs (Qualified Charitable Distributions) offer a smart way to lower your taxable income while managing your overall tax strategy. Instead of claiming an itemized deduction, a QCD excludes the donated amount from your Adjusted Gross Income (AGI). This is particularly important under the One Big Beautiful Bill Act (OBBBA), which limits itemized deductions for charitable contributions to amounts exceeding 0.5% of AGI [5]. Since QCDs are excluded from income altogether, they sidestep this limitation entirely.

"A QCD effectively provides a benefit at the full marginal rate... [It] bypasses this haircut, making the first dollar tax-free." – Richard Fox, Founder, Law Offices of Richard L. Fox [12]

This approach is especially advantageous for high-income earners, as it avoids caps that can reduce the value of other tax benefits.

Reducing your AGI through a QCD also has additional perks, like lowering taxes on Social Security benefits and avoiding IRMAA (Income-Related Monthly Adjustment Amount) surcharges. For example, in April 2026, Vanguard analyzed the case of a married couple, Terry and Kelly, both aged 75, with an income of $140,000. By opting for a $50,000 QCD instead of a traditional donation, they reduced their taxable income enough to make their Social Security benefits non-taxable, saving them over $5,400 in taxes [7].

These AGI reductions also align perfectly with the role QCDs play in meeting Required Minimum Distributions (RMDs).

Using QCDs to Satisfy RMDs

QCDs do more than just lower AGI - they also count toward fulfilling your annual RMD requirements. Individuals aged 73 or older must take RMDs, and using a QCD to meet this obligation keeps the distribution from increasing your taxable income [5].

"The amount donated through a QCD is generally excluded from your taxable income. That's different from a normal IRA withdrawal, where you take the distribution, it increases taxable income, and then you may (or may not) receive a charitable deduction." – White Cloud Wealth Management [3]

The IRS uses a "first dollars out" rule, meaning the first distributions you take from your IRA each year are applied to your RMD. To ensure your QCD counts toward your RMD and stays excluded from income, make your QCD before or alongside any other IRA withdrawals [4].

Elliott Davis provided a clear example in January 2026. A retiree in the 37% tax bracket faced a $100,000 RMD. By donating $50,000 through a QCD, the retiree avoided $18,500 in taxes. If they had taken the RMD first and then donated, the savings would have dropped to $16,625 due to the AGI floor and benefit cap - a difference of $1,875 [8]. This highlights how timing and strategy with QCDs can maximize your tax savings.

How to Make a QCD in 2026

Select an IRS-Approved Charity

To qualify as a QCD (Qualified Charitable Distribution), your donation must go to a 501(c)(3) organization approved by the IRS for tax-deductible contributions. These typically include public charities, churches, schools, and hospitals. However, donor-advised funds (DAFs), private foundations, and supporting organizations are excluded under the 2026 rules [2][3].

To ensure the organization is eligible, request its determination letter confirming its 501(c)(3) status. This step is crucial - if the charity doesn’t qualify, the distribution will be treated as taxable income.

"A donor-advised fund is not subject to any minimum required distribution. The money may stay there for years... The point of the charitable IRA rollover [has been] to get the money out into the charitable community." – Richard Fox, Founder, Law Offices of Richard L. Fox [12]

Also, remember the "no benefit" rule: your contribution must not result in receiving goods or services. For instance, if your donation covers the cost of a ticket for a charity event, it won’t count as a QCD [2][6].

Once you’ve confirmed the charity’s eligibility, the next step is to coordinate with your IRA custodian to complete the transfer.

Work with Your IRA Custodian

Reach out to your IRA custodian to set up a direct transfer to the charity. Make sure the check is made payable directly to the charity - not to you. If the check is issued in your name, the IRS will consider it taxable income, and you’ll lose the tax benefit of the QCD [2][3].

"The check must be made payable to the charity. If the check is made payable to you, it's usually not a qualified charitable distribution and you lose the tax benefit!" – White Cloud Wealth Management [3]

Some custodians allow you to write the check yourself, provided the funds are available. Whether the custodian mails the check to the charity or sends it to you for forwarding, the important detail is that the check must be payable to the charity.

Timing is critical: the distribution must leave your IRA by December 31, 2026, to count for that tax year. There’s no grace period extending into January 2027, so be sure to plan ahead to meet the deadline [2][3].

Keep Proper Documentation

After completing the transfer, it’s essential to maintain accurate records to confirm compliance with QCD rules. For donations of $250 or more, obtain a written acknowledgment from the charity explicitly stating that no goods or services were received in exchange for your contribution [6].

Your IRA custodian will report the distribution on Form 1099-R, using the new Code "Y" for QCDs starting with 2025 distributions. On your 2026 tax return, you’ll report the total distribution on Form 1040, Line 4a, and enter "0" with "QCD" noted on Line 4b [9][16].

"Starting with 2025 distributions filed in early 2026, Form 1099-R will include a new Code 'Y' to show that a distribution was designated as a QCD." – Elmer Howard, Prosperity Financial Accounting [9]

Since some custodians may still report QCDs as regular distributions, it’s a good idea to notify your tax preparer about which distributions qualify as QCDs. This ensures proper reporting and helps you take full advantage of the tax benefits [3][15].

QCD Update for 2026 - Advice You Should Know | Ep #81

QCDs vs. Itemized Deductions

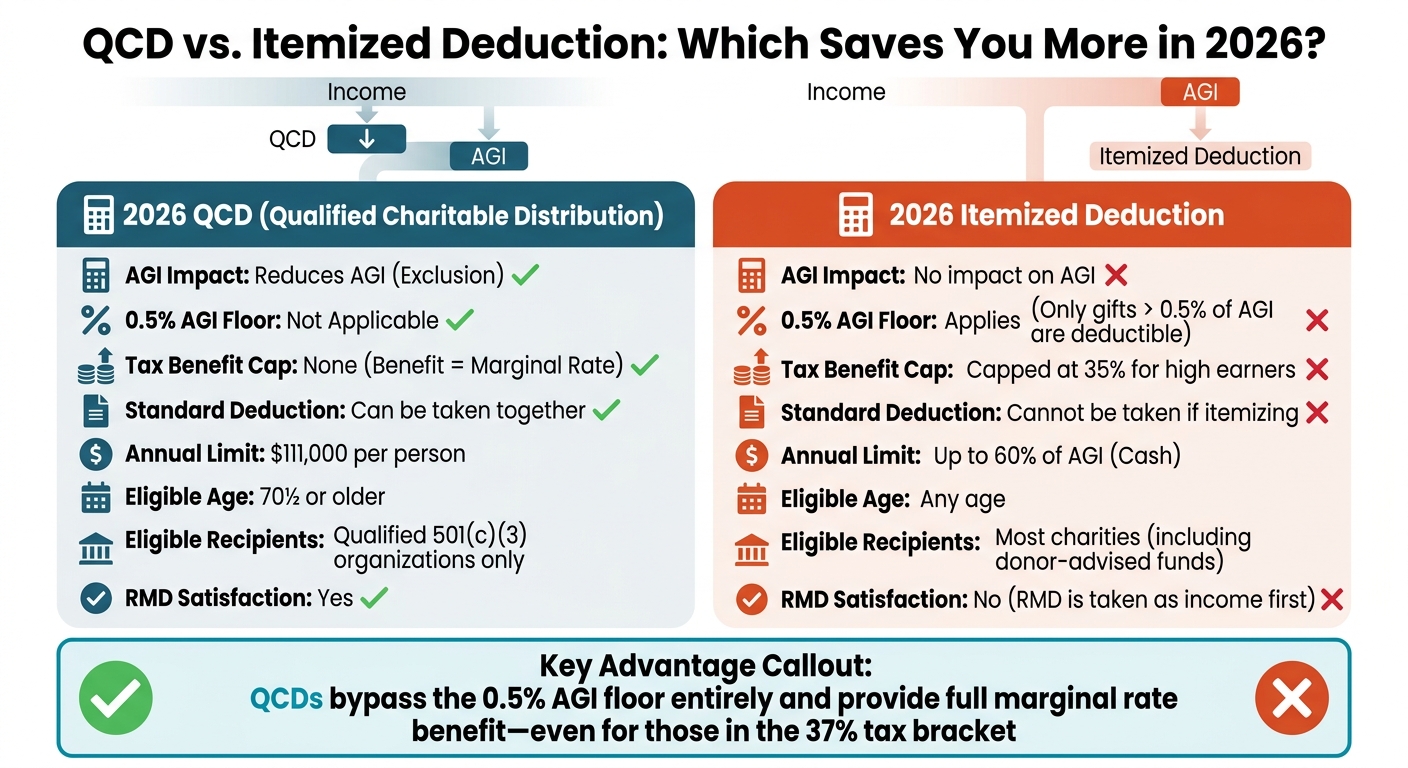

QCD vs Itemized Deduction Tax Benefits Comparison 2026

Side-by-Side Comparison

When planning for 2026 taxes, understanding the differences between Qualified Charitable Distributions (QCDs) and itemized deductions can help you make smarter financial decisions. QCDs reduce your Adjusted Gross Income (AGI) directly, while itemized deductions only lower taxable income after AGI is calculated. This distinction is crucial, especially under the new tax laws, where charitable contributions can only be deducted if they exceed 0.5% of your AGI. QCDs bypass this hurdle by never being included in your income in the first place.

For high-income earners, there’s another catch: itemized charitable deductions are capped at 35%, even if you fall into the 37% tax bracket. QCDs avoid this limit entirely, letting you reap the full benefit based on your marginal tax rate. Plus, with a QCD, you can still claim the full standard deduction - $16,100 for single filers and $32,200 for married couples filing jointly in 2026. In contrast, itemizing requires you to give up the standard deduction.

Here’s a quick comparison to highlight the key differences:

| Feature | 2026 QCD | 2026 Itemized Deduction |

|---|---|---|

| AGI Impact | Reduces AGI (Exclusion) | No impact on AGI |

| 0.5% AGI Floor | Not Applicable | Applies (Only gifts > 0.5% of AGI are deductible) |

| Tax Benefit Cap | None (Benefit = Marginal Rate) | Capped at 35% for high earners |

| Standard Deduction | Can be taken together | Cannot be taken if itemizing |

| Annual Limit | $111,000 per person | Up to 60% of AGI (Cash) |

| Eligible Age | 70½ or older | Any age |

| Eligible Recipients | Qualified 501(c)(3) organizations | Most charities (including donor-advised funds) |

| RMD Satisfaction | Yes | No (RMD is taken as income first) |

"Because itemizers may see a reduction in the tax benefits of donations under the new rules, this change could make the tax savings from a QCD even greater than itemizing charitable donations in some situations." – Hayden Adams, Director of Tax Planning and Wealth Management, Schwab Center for Financial Research

These differences not only affect your tax liability but also simplify the process of preparing your taxes.

Simpler Tax Filing with QCDs

QCDs don’t just save you money - they also make tax filing easier. Unlike itemized deductions, which require you to track receipts, calculate whether your total deductions exceed the standard deduction, and deal with the 0.5% AGI floor, QCDs allow you to simply exclude the amount from your taxable income on Form 1040.

Traditional charitable donations increase your AGI, which can reduce the overall tax benefit because of deduction limits. In contrast, QCDs lower your AGI directly. This reduction can help you avoid income thresholds that trigger Medicare Part B and D premium surcharges or increase the taxation of your Social Security benefits.

For non-itemizers, the 2026 universal deduction for cash contributions is limited to just $1,000 for single filers and $2,000 for married couples filing jointly - far less than the $111,000 annual QCD limit.

"A QCD is an 'exclusion' from income, not an itemized deduction. This means you can still take the standard deduction since QCDs are not subject to itemization." – Kate Schubel, Tax Writer, Kiplinger

If you’re 70½ or older and plan to give to charity, QCDs offer a simpler, more effective way to achieve your goals while maximizing tax savings under the new rules.

Common QCD Mistakes to Avoid

Missing Year-End Deadlines

Don't miss the December 31 deadline - late distributions can become taxable and might impact your Required Minimum Distribution (RMD) calculations or reduce your benefits. Start the process early to account for processing and mailing delays.

Timing is everything. The IRS applies the "first dollars out" rule, meaning the first funds withdrawn from your IRA during the year count toward your RMD. For instance, if you take a regular RMD withdrawal in January and later attempt a Qualified Charitable Distribution (QCD) in November, you can't retroactively apply the QCD to offset the earlier withdrawal.

"If an RMD was already taken earlier in the year, a QCD taken subsequently can't offset the RMD income. The QCD will still be excluded from income, but the RMD already taken will be included in income" – Ed Slott, Founder of Ed Slott and Company [17].

If your IRA offers check-writing privileges, ensure the charity cashes the check before December 31. A check dated in December but cleared in January will count toward the next tax year [10].

Additionally, always confirm the charity's eligibility to preserve the tax benefits of your QCD.

Donating to Ineligible Organizations

Beyond meeting deadlines, it's essential to verify that the organization receiving your QCD is eligible. Only qualified 501(c)(3) organizations can accept QCDs. Donor-advised funds, private foundations, and supporting organizations are excluded.

"Currently, QCDs cannot be made to donor-advised fund sponsors, private foundations and supporting organizations, though these are categorized as charities" – Fidelity Charitable [11].

Use the IRS Tax Exempt Organization Search to confirm eligibility. If an organization isn't listed in Publication 78, it cannot receive QCDs [19].

As highlighted earlier in "Work with Your IRA Custodian", the funds must transfer directly from your IRA custodian to the qualified charity. Receiving any benefit in return for your donation - like event tickets or a dinner - will disqualify the entire distribution from being treated as a QCD [17][18][1].

Conclusion: Making the Most of QCDs in 2026

In 2026, Qualified Charitable Distributions (QCDs) provide a smart way to reduce taxes while meeting your Required Minimum Distribution (RMD) requirements. With new limits on itemized deductions, QCDs stand out as a way to exclude up to $111,000 per person from taxable income.

The beauty of QCDs lies in their straightforward tax advantages. They allow you to fulfill your RMD obligations and lower your Adjusted Gross Income (AGI) in one step - all while supporting a qualified charity. Unlike traditional donations, which require itemizing to claim a deduction, QCDs offer tax benefits even if you use the standard deduction.

To get the most out of QCDs, it’s important to act early and keep accurate records. Start the process at the beginning of the year to ensure the distribution counts toward your RMD before taking any other withdrawals. Direct your IRA custodian to send the funds straight to the charity, and make sure everything is finalized before the December 31 deadline - missed deadlines mean the transfer becomes taxable.

Here’s a quick checklist to help you plan effectively:

QCD Planning Checklist

- Confirm you are at least 70½ years old and that the donation comes from an eligible IRA, such as a Traditional, Rollover, or Inherited IRA.

- Direct your IRA custodian to make the check payable to a qualified 501(c)(3) charity - not to you - and initiate the transfer early to avoid delays.

- Monitor your total QCD amount to ensure it doesn’t exceed the annual limit of $111,000 per person (or $222,000 for married couples with separate IRAs).

- Keep essential documents, including your Form 1099-R and a written acknowledgment from the charity.

- Notify your tax preparer that the distribution was a QCD, as custodians may not always report it correctly until the new "Code Y" becomes standard.

FAQs

Can I do a QCD if I’m not taking RMDs yet?

Yes, you can make a Qualified Charitable Distribution (QCD) even if you’re not yet required to take Required Minimum Distributions (RMDs). The only condition is that you must be at least 70½ years old, as QCDs become an option starting at that age, regardless of whether RMDs apply to you or not.

How do I make sure my QCD counts for this tax year?

To make sure your QCD counts for this tax year, finalize the transfer by December 31. The funds must go directly from your IRA to the charity. You also need to confirm you're at least 70½ years old when the transfer happens. Keep detailed records, and ensure your IRA custodian manages the process accurately. Lastly, stick to the annual limit, which will be up to $111,000 for 2026.

Does a QCD change my Medicare premiums or Social Security taxes?

A Qualified Charitable Distribution (QCD) doesn’t impact your Medicare premiums or Social Security taxes directly. However, it can reduce your taxable income, which might help you avoid higher Medicare Income-Related Monthly Adjustment Amount (IRMAA) surcharges. This makes QCDs an effective way to manage your tax burden while contributing to charitable organizations.