IRS Rules for Donations to Educational Institutions

When donating to educational institutions, you can reduce your taxable income by following IRS rules. Here's a quick summary of what you need to know:

- Qualified Donations: Contributions must go to IRS-approved organizations like public schools, colleges, or nonprofit educational institutions. For-profit schools and direct payments (e.g., tuition) are not deductible.

- Documentation: Always keep records. For cash donations over $250, you need a written acknowledgment. Noncash donations over $500 require Form 8283, and those over $5,000 need a professional appraisal.

- Deduction Limits: Cash donations are capped at 60% of your Adjusted Gross Income (AGI). Starting in 2026, itemized deductions will only apply to donations exceeding 0.5% of your AGI.

- Standard Deduction Benefit: From 2026, non-itemizers can deduct up to $1,000 ($2,000 for joint filers) for cash donations to qualified organizations.

- Quid Pro Quo Donations: If you receive goods or services in return, you can only deduct the portion exceeding their fair market value.

Proper records and understanding these rules ensure you maximize your deductions while staying compliant.

Which Educational Organizations Qualify for Tax Deductions?

Public Schools and Nonprofit Educational Institutions

Tax deductions are available for contributions to nonprofit organizations that focus exclusively on educational purposes under Section 501(c)(3) [1]. This includes a wide range of entities like public K–12 schools, state-run universities, colleges, trade schools, educational museums, and nonprofit daycare centers that serve the public and working parents. Other qualifying organizations include planetariums, zoos, and youth groups such as Scouting America and the Girl Scouts of the USA.

Private schools can qualify, but only if they maintain a publicized, nondiscriminatory admissions policy. To confirm an organization's tax-exempt status, check the IRS Tax Exempt Organization Search (TEOS) or review the organization's IRS exemption letter.

Organizations That Don't Qualify

For-profit educational institutions are not eligible for tax-deductible charitable contributions, even if they are accredited or allow students to claim education tax credits like the American Opportunity Tax Credit. Payments such as tuition, enrollment fees, or other charges required for a student’s education are considered personal expenses and cannot be deducted as charitable contributions. Similarly, donations made directly to individual educators or students are not deductible.

Donations to foreign schools are generally not deductible either, except in rare cases covered by specific tax treaties. Even then, these exceptions usually require the donor to have income tied to the country in question.

The next section will outline the documentation needed to claim these deductions.

sbb-itb-e723420

2025 is THE YEAR for charitable deduction tax planning

Required Documentation for Claiming Deductions

IRS Documentation Requirements for Educational Donations by Value

Cash Donations

When making cash donations - whether through cash, check, or electronic payment - it's crucial to keep proper records. Acceptable documentation includes bank records (such as canceled checks, credit card statements, or transfer receipts) or a written confirmation from the organization. This confirmation should clearly state the institution's name, the donation date, and the amount donated [6][7][9].

For contributions exceeding $250, you'll need a contemporaneous written acknowledgment (CWA). This document must confirm whether any goods or services were received in exchange for the donation and estimate their value if applicable. It's important to secure this acknowledgment before filing your tax return. Specifically, you must have it by the earlier of the filing date or the extended filing deadline [1][7][5].

If you're donating through payroll deductions, retain employer documentation (like a pay stub or Form W-2) along with a pledge card or note from the organization that includes its name [1][7].

Now, let’s shift focus to noncash donations, where documentation requirements depend on the donation's value.

Noncash Donations

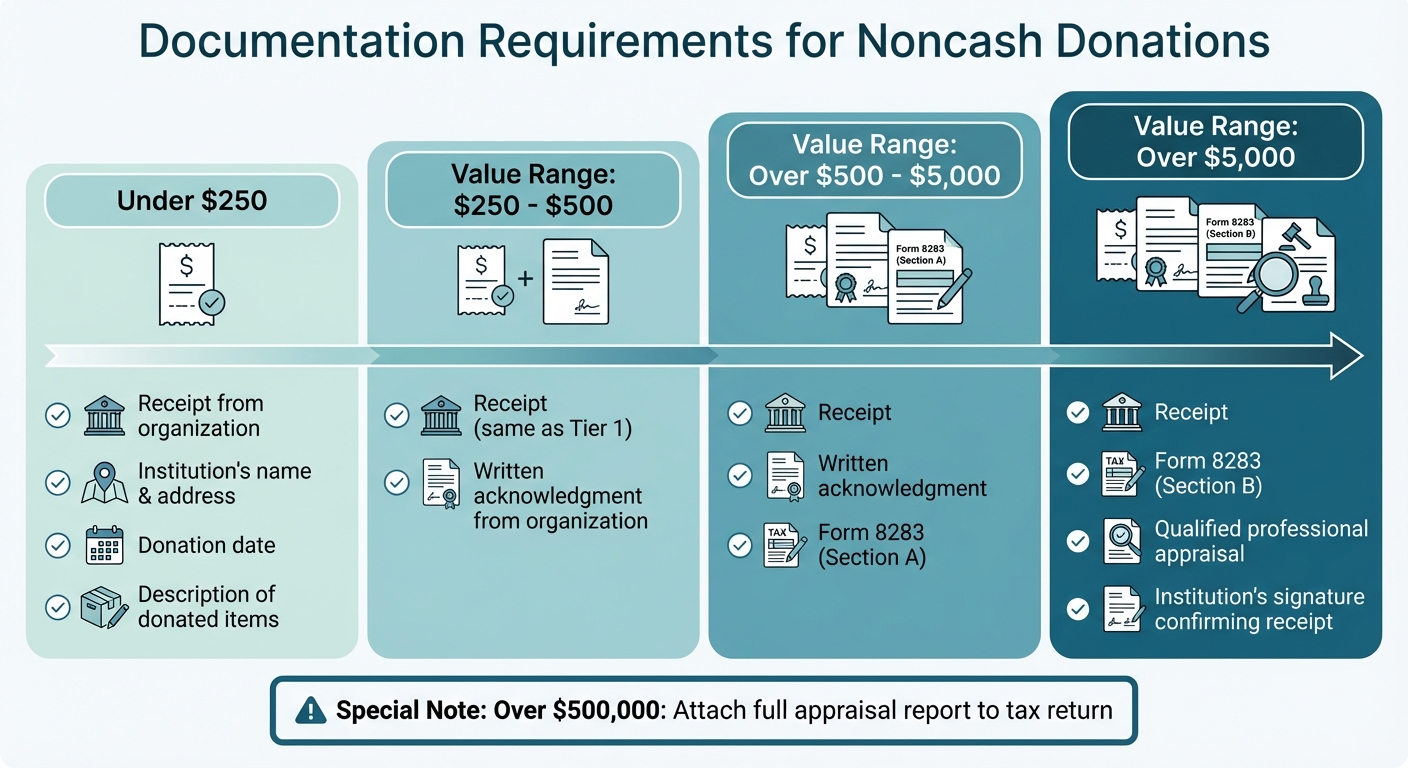

For noncash contributions, the required documentation becomes more detailed as the value of the donation increases:

- Under $250: Obtain a receipt from the organization. It must include the institution's name, address, the donation date, and a detailed description of the donated items [1].

- $250 to $500: In addition to the receipt, secure a contemporaneous written acknowledgment from the organization [1].

- Over $500 to $5,000: Along with the receipt and acknowledgment, you’ll need to file Form 8283, Section A, with your tax return [1][9].

- Over $5,000: This requires a qualified professional appraisal, completion of Form 8283, Section B, and the institution's signature confirming receipt of the donation [1][8].

If you claim a deduction exceeding $500,000, you must also attach the full appraisal report to your tax return.

| Noncash Contribution Value | Required Documentation |

|---|---|

| Under $250 | Receipt with institution's name, date, location, and property description [1] |

| $250 – $500 | Receipt and written acknowledgment from the organization [1] |

| Over $500 – $5,000 | Receipt, written acknowledgment, and Form 8283 (Section A) [1][9] |

| Over $5,000 | Receipt, Form 8283 (Section B), and qualified appraisal [1][8] |

There’s an additional rule to keep in mind: donations of clothing and household items need to be in "good used condition" or better. If an item doesn't meet this standard but you’re claiming a deduction above $500, you’ll still need a qualified appraisal, even if the value is below $5,000.

Lastly, remember that it’s your responsibility to obtain the written acknowledgment. The IRS won't automatically receive this documentation [5].

Deduction Limits and AGI Thresholds

Cash Contribution Limits

If you're donating cash to educational institutions, the IRS sets a limit on how much you can deduct - 60% of your Adjusted Gross Income (AGI). This rule, which became permanent on January 1, 2026, provides donors with clarity for planning their charitable contributions [11]. For instance, if your AGI is $100,000, your annual deduction is capped at $60,000.

What happens if you donate more than the limit? The IRS allows you to carry forward any excess contributions and deduct them over the next five tax years [10][9]. This flexibility ensures you can still benefit from your generosity in future tax filings.

These rules are key to understanding how AGI thresholds influence the total amount you can deduct.

The 2026 AGI Floor for Itemized Deductions

Starting in 2026, a new rule changes how itemized charitable deductions work. You’ll only be able to deduct the portion of your charitable contributions that exceeds 0.5% of your AGI [11]. Essentially, the first 0.5% of your AGI in donations won’t qualify for a deduction.

"This 0.5% threshold functions like a floor. You must clear it before any of your donations count for a tax deduction." - Megan Lencoski, Carnegie Investment Counsel [11]

Here’s an example: If your AGI is $200,000, the first $1,000 (0.5% of $200,000) of your contributions won’t be deductible. Only the amount above that threshold will count toward your itemized deductions [12]. For someone with an AGI of $100,000, the first $500 of donations won’t provide any tax benefit [11].

To work around this, many donors are considering "bunching" contributions - grouping multiple years’ worth of donations into a single tax year. This strategy helps ensure the total exceeds the 0.5% floor, maximizing the deductible amount [11].

There’s also a new benefit for non-itemizers: starting in 2026, taxpayers who take the standard deduction can claim an above-the-line deduction for cash donations made directly to qualified educational institutions. The limit is up to $1,000 for individuals or $2,000 for married couples filing jointly [11][12].

Quid Pro Quo Contributions: How Benefits Reduce Deductions

When it comes to quid pro quo contributions, only the portion of your payment that exceeds the fair market value of the benefit you receive is deductible. For instance, if you spend $65 on a ticket to a school dinner dance and the meal and entertainment are valued at $25, your deductible amount is $40 ($65 - $25) [1].

Small "token" gifts like bookmarks, calendars, or keychains are considered insubstantial and don’t affect the deductible portion [13][14]. Similarly, membership perks valued under $75 - such as free parking or discounted admission - are typically ignored when calculating deductions [13].

However, if your donation earns you a state or local tax credit exceeding 15% of the donation, your federal deduction is reduced accordingly. For example, a $1,000 donation that results in a 70% state tax credit ($700) leaves you with a $300 federal deduction [1]. These rules, combined with requirements for documentation and AGI thresholds, determine the final amount you can deduct.

Common Examples of Quid Pro Quo Contributions

Fundraising events often involve situations where donors receive something in return, which impacts the deductible amount. Here are some typical examples:

- School Fundraising Auctions: If you pay $600 for a week’s beach house rental valued at $600, there’s no deductible contribution because the payment equals the fair market value [1].

- Athletic Event Tickets: Purchasing a $50 basketball game ticket labeled as a $100 contribution results in a $50 deductible amount, as the ticket’s fair market value is $50 [1].

- Professional Services at Fundraisers: A $500 payment for a one-hour tennis lesson with a professional who charges $100 per hour leaves a deductible amount of $400 ($500 - $100) [13].

For contributions over $75, the organization must provide a written disclosure that estimates the fair market value of any benefits received. Failing to provide this disclosure can lead to penalties of up to $5,000 per event [13][14]. Always request this documentation to ensure your deduction is calculated correctly.

A useful tip: If you receive a ticket to a charity event but don’t plan to attend, return it to the organization for resale. This way, you can deduct the full payment amount since you’re not receiving any benefit in return [1].

Noncash Donations: Valuation and Documentation

When donating noncash items to schools, understanding how to properly value and document your contributions is key to maximizing your tax deductions. The IRS requires that these items be valued accurately, following specific rules. Your deduction amount is based on the fair market value (FMV), which the IRS defines as the price a willing buyer and seller would agree upon in an open market [1]. For items like books or equipment, this often means checking what similar used items sell for in the current market.

When Appraisals Are Necessary and How to Value Donations

For noncash donations over $5,000, a qualified appraisal is mandatory. However, neither the donor, the school, nor the seller can serve as the appraiser [8]. High-value art donations may be subject to review by the IRS Art Advisory Panel, a group of 25 art experts. If the art is appraised at $50,000 or more, you can request a "Statement of Value" from the IRS for additional clarity [2][15].

Not all high-value items require appraisals. For example, publicly traded securities are exempt from this requirement, even if their value exceeds $5,000 [8]. However, for donations above $500,000, the IRS requires that the full appraisal report be attached to your tax return [1].

| Deduction Amount | Appraisal Required? | Additional Notes |

|---|---|---|

| Over $5,000 | Yes (Qualified Appraisal) | Both appraiser and school official must sign Form 8283 (Section B) |

| Over $50,000 (Art) | Yes | May be reviewed by the IRS Art Advisory Panel; Statement of Value available |

| Over $500,000 | Yes | Appraisal must be included with the tax return |

| Publicly Traded Securities | No | Appraisal exemption applies regardless of value |

Recordkeeping for Noncash Donations

If your total noncash donations exceed $500 in a year, you’ll need to file Form 8283 [8]. Section A of this form is for items valued between $501 and $5,000, while Section B is for items over $5,000. Section B also requires signatures from both the appraiser and an authorized school official to confirm the donation [8].

To strengthen your records, include details such as the school’s name, the date and location of the donation, and a thorough description of the items given [1]. Taking photos of the donated items - especially for high-value items like equipment, art, or clothing - can help prove their condition and support your FMV claim if the IRS questions your valuation. Additionally, for donations of $250 or more, you must obtain a written acknowledgment from the school. This acknowledgment should describe the donated property and confirm whether you received any goods or services in return [1].

It’s also important to note the "unrelated use" rule. If the school uses your donated items for purposes unrelated to its educational mission, your deduction might be limited to the cost basis rather than the FMV [1]. Furthermore, if the school sells or disposes of donated property valued over $500 within three years, they are required to file Form 8282 and provide you with a copy within 125 days [8].

Next, we’ll look at how tools like Deductible.me can help streamline the donation process.

Managing Donations with Deductible.me

Keeping track of donations, especially to schools and educational institutions, can get overwhelming - think receipts, valuations, and IRS forms piling up. Deductible.me takes the hassle out of the process by automating key tasks while ensuring you stay within IRS guidelines.

AI-Powered Valuation and IRS-Compliant Reports

Figuring out the fair market value (FMV) for donated items like books, computers, or classroom supplies can feel like guesswork. Deductible.me eliminates that uncertainty by using AI to calculate FMV based on current market prices for similar used items. This aligns with the IRS's definition of FMV: what a willing buyer would pay in an open market[16]. Plus, it ensures your donations meet the IRS's "good used condition" standard[4].

The platform also generates the necessary IRS forms when donation thresholds are met. For example, if your repeated donations (like books) approach the $5,000 mark, Deductible.me will alert you that a qualified appraisal is required. It even helps you maintain the contemporaneous written acknowledgments the IRS mandates for certain donations[4]. By tracking forms and thresholds, it keeps everything organized and seamlessly integrates into your annual giving strategy.

Setting and Tracking Annual Giving Goals

Beyond documentation, Deductible.me is your partner in managing IRS donation limits. It helps you set and monitor annual goals, keeping cash donations within the 60% of AGI limit and appreciated assets within the 30% cap[17]. If your contributions exceed AGI limits for the year, the platform tracks carryovers, allowing you to apply the excess to future tax years (up to five years)[1]. It’s a straightforward way to stay on top of your giving while maximizing your tax benefits.

Conclusion

Donating to educational institutions not only strengthens your community but also offers potential tax benefits - provided you follow IRS guidelines. The first step is confirming the organization’s eligibility through the IRS Tax Exempt Organization Search tool. From there, maintaining accurate documentation for each donation is crucial, especially since contributions that come with benefits (quid pro quo donations) reduce the deductible amount by the value of those benefits [1][3].

Staying organized is key. Ensure you have proper records and stay within the AGI limits: 60% for cash donations and 30% for noncash appreciated property. These steps help safeguard your deductions and keep you in compliance with IRS rules [1][18].

To make things easier, Deductible.me streamlines the process. It automates fair market value calculations, generates IRS-compliant reports, tracks donations against AGI limits, and even notifies you when appraisals are required. This tool takes much of the hassle and uncertainty out of charitable giving, so you can focus on making a difference.

FAQs

How do I verify a school is a qualified 501(c)(3)?

To check if a school qualifies as a 501(c)(3) organization, you can use the IRS Tax Exempt Organization Search tool. This tool helps confirm the school's tax-exempt status and whether it can accept tax-deductible donations. For additional information, consult resources like IRS Publication 557, which outlines the requirements and guidelines for tax-exempt organizations.

What qualifies as a “written acknowledgment” from the school?

To claim a deduction for your donation, you’ll need a “written acknowledgment” from the recipient. This document should confirm the donation, describe any property you gave, and specify whether you received any goods or services in return. It also needs to include other necessary details. Make sure you have this acknowledgment in hand before filing your tax return, as it’s required to validate your deduction.

How do I value donated items to avoid an IRS challenge?

To stay on the right side of IRS rules, it's essential to establish the fair market value (FMV) of any items you donate, following their guidelines. For donations worth more than $5,000, you'll need to secure a qualified appraisal and fill out Form 8283, Section B. If the value is $500 or less, you can determine the amount yourself - just be sure to maintain thorough records and take photos of the items. Having proper documentation not only keeps you compliant but also helps minimize the chances of any disputes with the IRS.