How State Tax Laws Impact Charitable Deductions

State tax laws can significantly influence your charitable deductions, often in ways that go unnoticed. While federal rules set a baseline, state-specific regulations - like deduction caps, AGI thresholds, and tax credits - can either enhance or limit your savings. Here’s a quick breakdown of what you need to know:

- Federal vs. State Rules: Federal deductions reduce taxable income, but states may offer tax credits (directly lowering your tax bill) or impose stricter limits on deductions.

- State-Specific Examples:

- California reduces itemized deductions by 6% of AGI above $252,000.

- Colorado caps deductions at $1,000 for single filers with AGI over $300,000.

- Minnesota provides a deduction for non-itemizers exceeding $500 in donations.

- 2026 Federal Changes: A new 0.5% AGI floor means only donations above this threshold are deductible. Non-itemizers gain a $1,000 deduction ($2,000 for joint filers).

- Strategies to Maximize Deductions: Consider bunching donations, using donor-advised funds, or leveraging state-specific tax credits.

Managing these rules can be complex, but tools like Deductible.me simplify tracking, compliance, and optimization. The right strategies can help you navigate both federal and state tax systems while maximizing your charitable impact.

Common Problems with State Tax Laws and Deductions

Different State Approaches to Federal Tax Rules

States handle charitable deductions in various ways, creating a patchwork of rules that can be confusing for taxpayers. Some states, like Arizona and Oregon, align closely with federal tax laws, making the process relatively simple. On the other hand, states such as California and New York operate with their own tax systems and distinct deduction rules[8].

The complexity grows when considering how states treat tax benefits. While some states offer tax credits (which directly reduce your tax bill), others provide tax deductions (which lower your taxable income). If you receive a state tax credit, the IRS considers it a "return benefit" under Treasury Regulation § 1.170A-1(h). This means your federal charitable deduction must be reduced by the amount of the state credit[1][3].

Adjusted Gross Income (AGI) limits also vary. Federally, cash gifts up to 60% of your AGI are allowed, but California caps them at 50%[2][5]. Some states, like Alabama, Arkansas, Hawaii, Kentucky, and Minnesota, base these limits on state AGI rather than federal AGI[2]. These differences highlight how state-specific rules can complicate tax planning.

AGI Thresholds and Deduction Limits

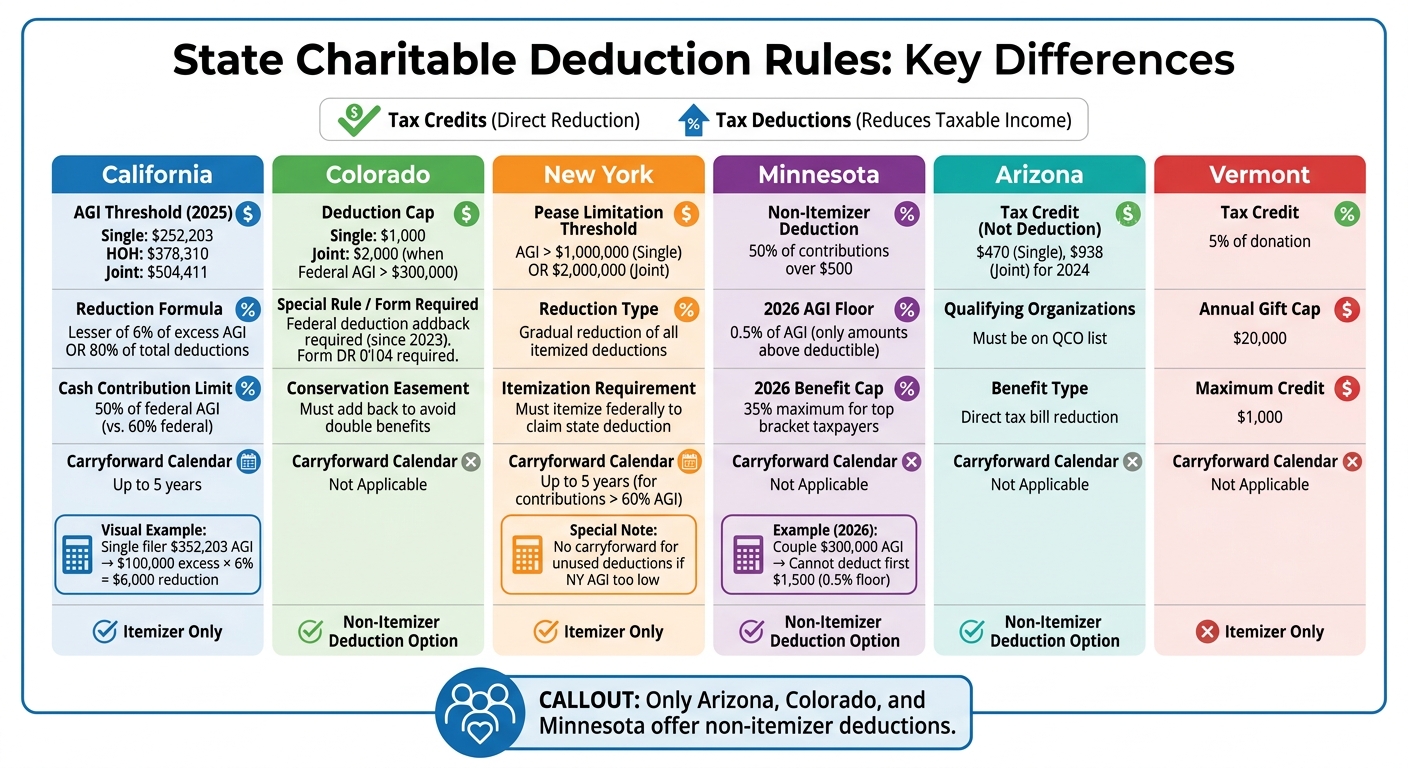

State-specific AGI thresholds add another layer of complexity for taxpayers trying to maximize their deductions. Many states reduce itemized deductions once your income exceeds a certain level. For instance, California reduces itemized deductions by 6% of federal AGI over approximately $252,000 for single filers (or about $504,411 for joint filers), capping deductions at 80%. New York uses a tiered system, reducing deductions by 25% to 75% based on income levels[2][7].

Some states impose strict caps on deductions, regardless of donation size. Colorado limits itemized deductions to $1,000 for single filers and $2,000 for joint filers once federal AGI surpasses $300,000[2][7]. Maine caps deductions at $37,100 and phases them out entirely at higher income levels[7]. Vermont, instead of deductions, offers a 5% tax credit with a $20,000 annual gift cap, resulting in a maximum credit of $1,000[2][7].

Unlike federal rules, some states don't allow unused deductions to carry over to future years. For example, a 2024 New York Advisory Opinion confirmed that if your New York AGI is too low to use your full charitable deduction in the year you make the gift, the excess cannot be carried forward - even if it was fully deductible federally[6]. This could mean losing potential state-level tax benefits for large donations made in high-income years.

No Uniform Rules Across States

The lack of consistent rules across states makes tax planning even more difficult. State standard deductions vary widely, from $2,425 in Illinois to $8,000 in New York[8]. Depending on your situation, you might find it beneficial to itemize on your state return while taking the standard deduction federally - or vice versa.

Additionally, not all federally recognized charities qualify for state-level benefits. States like Arizona and Virginia maintain their own lists of approved organizations. For example, Arizona has its Qualifying Charitable Organizations (QCOs), with a maximum credit of $470 for single filers and $938 for joint filers in 2024[1]. Georgia's Qualified Education Expense Tax Credit, meanwhile, has a statewide annual cap of $120 million[1].

Only a few states - Arizona, Colorado, and Minnesota - offer a non-itemizer deduction, allowing taxpayers who take the standard deduction to still claim charitable contributions[9]. Minnesota was the first to introduce this type of law, aiming to encourage charitable giving among all taxpayers, including those who don't itemize[5]. This patchwork of rules requires donors to keep separate records for state-specific deductions and federal-only deductions, adding another layer of complexity[8].

sbb-itb-e723420

Federal Tax Changes and State Conformity in 2026

Federal Tax Changes in 2026

Starting January 1, 2026, the One Big Beautiful Bill Act (OBBBA) introduces new rules for charitable deductions. One major change is the addition of a 0.5% AGI floor for itemizers. This means only charitable contributions exceeding 0.5% of your adjusted gross income (AGI) will be deductible. For example, a couple with an AGI of $300,000 could deduct only donations above $1,500[10].

High-income earners in the top federal tax bracket face another limitation: their charitable deduction benefits are capped at 35%[10]. This adds a 2% cost to charitable giving for the wealthiest donors. For instance, a $10,000 donation that previously saved $3,700 in taxes will now save around $3,500. This cap increases the marginal cost of giving for those in the highest tax brackets.

For non-itemizers, there's some good news. They can now claim an above-the-line deduction for cash donations to qualified charities - up to $1,000 for single filers and $2,000 for joint filers. This change benefits the roughly 90% of taxpayers who don’t itemize[11]. Additionally, the SALT deduction cap has been raised to $40,400, with a phase-out for households earning over $505,000[10].

These federal adjustments create a new landscape for charitable deductions, with state responses playing a crucial role in shaping the overall impact.

How States Are Responding to Federal Changes

States are reacting differently to the federal updates, which could significantly affect how much donors benefit from their charitable contributions. Some states automatically align with federal tax laws, while others - like California and New York - have independent charitable deduction rules[12]. This means thresholds and limits may vary based on where you live. For example, while the federal law implements a 0.5% AGI floor, some states might not adopt this rule or could create their own variations.

High-income earners in states with independent tax systems should consult tax professionals to fully understand how these changes might influence their state tax returns. Another notable shift is the expected rise in the number of itemizers, projected to grow from 10% to 14% in 2026. This could lead to unique scenarios where taxpayers itemize on their federal return but take the standard deduction on their state return - or vice versa[10].

Federal vs. State Rules Comparison

The table below breaks down key differences between the new federal rules and how states typically handle these issues:

| Feature | Federal Rules | State Approach |

|---|---|---|

| Non-Itemizer Deduction | Up to $1,000 for single filers and $2,000 for joint filers[11] | Varies by state |

| Itemized Deduction Floor | 0.5% of AGI[10] | Varies by state |

| High-Income Deduction Cap | Capped at 35% for high earners[10] | Varies by state |

| AGI Limit for Cash Gifts | Deductible up to 60% of AGI[10] | Often aligns with federal rules but may differ |

| SALT Deduction Cap | Increased to $40,400 with phase-out for AGIs above $505,000[10] | Impacts vary by state |

This comparison shows that while federal tax changes set a broad framework, state-specific variations add complexity. Donors will need to pay close attention to both sets of rules to navigate these changes effectively and maximize their deductions.

Making donations in 2026: What new tax rules mean for charitable giving now and later

State-Specific Limits on Charitable Deductions

State-by-State Charitable Deduction Rules and Limits Comparison 2025-2026

California: AGI-Based Reduction on Itemized Deductions

California has a unique Limitation on Itemized Deductions (LID) that kicks in once your federal Adjusted Gross Income (AGI) surpasses specific thresholds. For the 2025 tax year (returns filed in 2026), these thresholds are set at $252,203 for single filers, $378,310 for heads of household, and $504,411 for married couples filing jointly[13]. If your income exceeds these limits, California reduces your total itemized deductions by the lesser of 6% of the excess AGI or 80% of total deductions[13].

Here’s an example: a single filer with a federal AGI of $352,203 exceeds the threshold by $100,000. Applying the 6% rule, their deductions would be reduced by $6,000. If they initially claimed $30,000 in deductions, they would only be allowed $24,000 after the reduction. The 80% rule ensures that at least 20% of deductions remain intact, no matter how high the income.

California also has stricter rules for cash contributions. While federal law allows deductions for cash contributions up to 60% of AGI, California caps this at 50% of federal AGI[13][14]. Contributions exceeding this limit can be carried forward for up to five years.

Colorado: Itemized Deduction Caps and Non-Itemizer Rules

Colorado starts with your federal AGI but requires you to add back any federal deductions that exceed the state’s limits[15]. From the 2023 tax year onward, this "Standard or Itemized Federal Deduction Addback" applies to all taxpayers, whether they itemize or take the standard deduction[15]. The addback essentially caps the benefit of deductions at the state level.

If you claim a federal deduction for gross conservation easements, Colorado requires you to add it back to avoid receiving double benefits[15]. Taxpayers use Colorado Form DR 0104 to calculate these adjustments and determine the allowable state deduction[15]. These rules highlight the need for careful tax planning to maximize the benefits of your charitable contributions.

New York and Minnesota: Tiered and Phased Reductions

New York and Minnesota take a more nuanced approach, using tiered and phased reduction systems.

New York applies the Pease Limitation, which gradually reduces itemized deductions for high earners. If your AGI exceeds $1,000,000 as a single filer or $2,000,000 as a married couple filing jointly, your deductions will start shrinking. Additionally, to claim charitable deductions in New York, you must itemize on your federal return, as the state doesn’t allow deductions for those using the standard deduction[16]. Contributions exceeding 60% of AGI can be carried forward for up to five years[16].

Minnesota offers a different setup. Non-itemizers can deduct 50% of charitable contributions that go beyond $500[17]. Starting in 2026, Minnesota will introduce a 0.5% AGI floor for itemizers, meaning only contributions above this threshold will qualify as deductible. For example, a couple with an AGI of $300,000 would not be able to deduct the first $1,500 of their donations[17]. Additionally, taxpayers in the top federal tax bracket (37%) will see their deduction benefits capped at 35% beginning in 2026[17].

| State | Rule Type | Threshold/Limit | Impact on Donors |

|---|---|---|---|

| New York | Pease Limitation | AGI > $1M (Single) / $2M (Joint) | Gradual reduction of all itemized deductions |

| Minnesota | Non-Itemizer Deduction | 50% of gifts over $500 | Provides a deduction for those using the federal standard deduction |

| Minnesota | 2026 AGI Floor | 0.5% of AGI | Only contributions above this floor are deductible |

| Minnesota | 2026 Benefit Cap | 35% Cap | Limits tax savings for taxpayers in the highest brackets |

How to Maximize State Charitable Deductions

Making the most of state-specific charitable deductions requires thoughtful planning to navigate limits and maximize tax savings.

Bunching Donations to Exceed Thresholds and Caps

One effective approach is bunching, where you combine multiple years of donations into a single tax year. This method helps push your itemized deductions above the standard deduction threshold, allowing you to claim a tax benefit in the year you bunch while taking the standard deduction in other years[18][19].

For the 2025 tax year, the standard deduction is $15,750 for single filers and $31,500 for married couples filing jointly[18]. Here's an example: A couple who typically donates $6,000 annually decides to combine two years of donations into a single $12,000 contribution. This move increases their deductions by $8,100, saving $11,800 in taxes across their 35% federal and 9.3% California tax brackets[19].

Another tool for bunching is Donor-Advised Funds (DAFs). These funds let you contribute a large sum during a high-income year to secure an immediate deduction, while distributing the money to charities over time[18][19]. This strategy is particularly helpful in overcoming the 0.5% AGI floor set to take effect in 2026[18]. High-income earners in California using bundling strategies can see tax savings ranging from $7,000 to $35,000[19].

If itemizing isn't an option for you, there are still ways to benefit from charitable giving.

Using Non-Itemizer Deduction Options

For those who take the standard deduction, some state programs still offer tax advantages. Starting in 2026, the OBBBA introduces an above-the-line deduction of $1,000 for single filers and $2,000 for married couples filing jointly[18].

Many states also offer tax credits that directly reduce your tax bill, even if you don't itemize[1]. For example:

- Arizona provides credits for donations to Qualifying Charitable Organizations (QCOs), allowing up to $470 for individuals and $938 for joint filers (2024 tax year).

- Virginia's Neighborhood Assistance Program (NAP) offers a 65% tax credit for donations to nonprofits that support low-income communities, with a minimum contribution of $500[1].

Unlike deductions, which lower taxable income, credits directly reduce your final tax bill. If a state tax credit is 15% or less of your donation amount, the IRS lets you retain the full federal charitable deduction without any reduction[3]. Always confirm that your chosen charity is on your state's approved list.

To simplify managing these options, there are tools designed to handle the complexity.

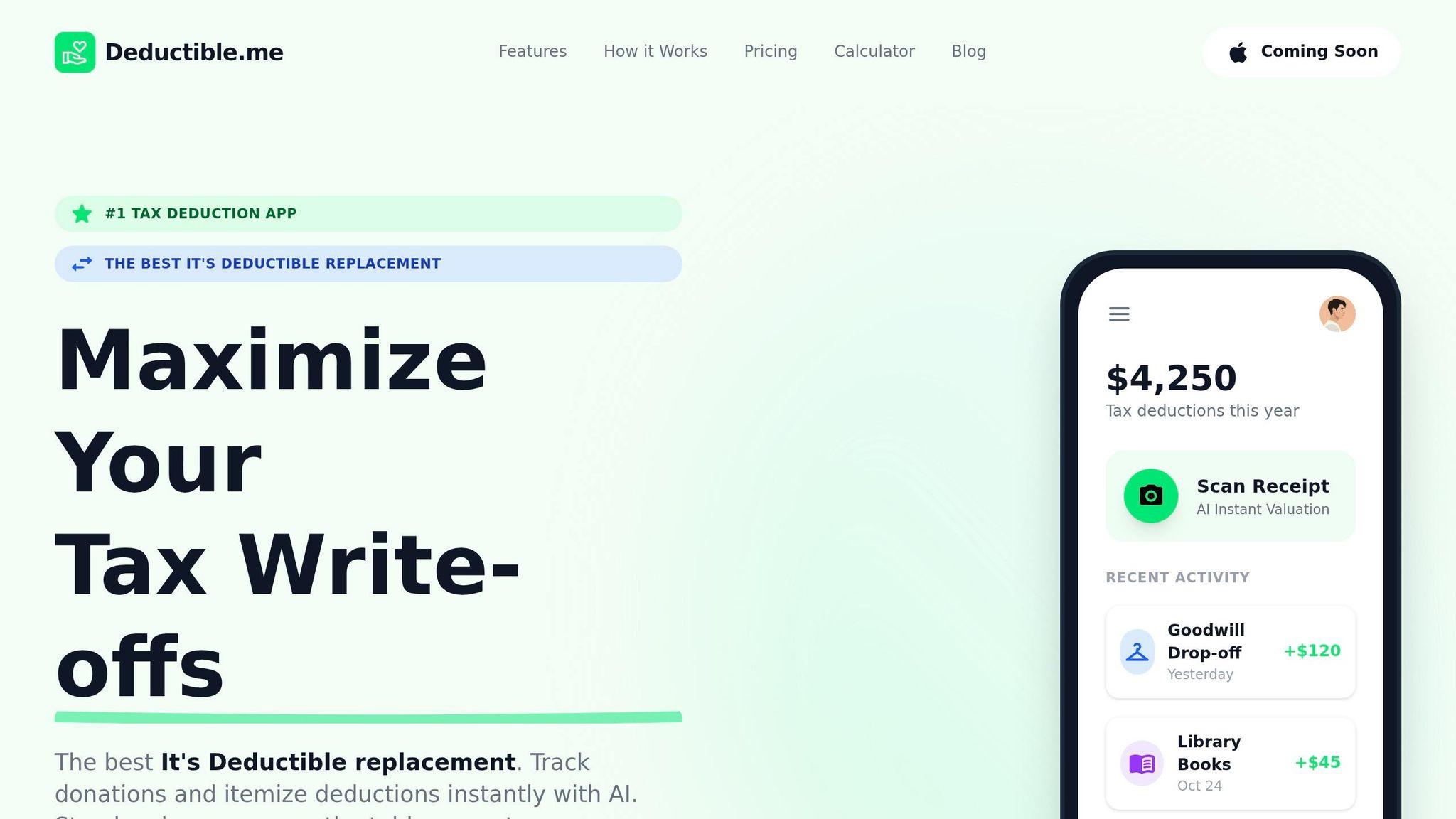

Using Deductible.me for Compliance and Optimization

Keeping up with varying state rules, federal limits, and required documentation can be a challenge. Deductible.me offers tools to make managing your deductions easier.

The app uses AI to value donated items - whether household goods, stocks, or real estate - and generates IRS-compliant reports. It also helps with tracking goals, modeling bunching strategies, and managing receipts. For non-cash contributions over $500, you'll need Form 8283, and for property valued above $5,000, a qualified appraisal is required[18]. Deductible.me ensures you're prepared with all the necessary documentation.

The platform also monitors your annual giving targets and calculates your "deduction gap" - the difference between your non-charitable itemized deductions and the standard deduction - so you know exactly how much to donate to maximize your tax benefit. For 2026, the app even accounts for the 0.5% AGI floor and alerts you when your contributions surpass this limit[20].

With advanced analytics, the app provides real-time insights into your donation patterns, helping you identify the best years for bunching and uncover state-specific opportunities. For serious donors, the Premium plan ($2/month) includes unlimited tracking, advanced receipt management, and priority support - essential for navigating complex tax rules.

Tools for Managing State Tax Rules

Navigating state-specific tax deduction rules can be tricky, but modern tools like Deductible.me are here to help. These tools make it easier to track donations, stay compliant, and find ways to maximize your tax savings across various states.

Deductible.me: Simplify and Optimize Your Charitable Contributions

Deductible.me is built to handle the complexities of both federal and state tax regulations. Using AI-driven valuation, the app evaluates donated items - like clothing, furniture, stocks, and even real estate - and generates IRS-compliant reports. These reports take into account federal requirements while also addressing state-specific rules.

Take California, for instance. Here, itemized deductions decrease by 6% once you cross certain AGI thresholds. Or consider Colorado, where deductions are capped at $1,000 for single filers with an AGI over $300,000. Deductible.me calculates the exact portion of your donations that qualify under these state-specific rules[2]. Even future tax changes, like the 0.5% AGI floor introduced by the One Big Beautiful Bill Act (OBBBA) for 2026, are factored into the app’s calculations. This helps you decide whether itemizing your deductions makes sense for both federal and state returns.

The app also simplifies compliance by managing forms like Form 8283 and appraisal requirements. This is especially helpful in states like Minnesota, where non-itemizers can use Schedule M1C to deduct 50% of charitable contributions exceeding $500[17].

But Deductible.me doesn’t stop at compliance. Its advanced features allow you to refine your overall giving strategy.

Advanced Analytics for Smarter Giving

For just $2 a month, the Premium plan unlocks analytics that give you real-time insights into your donation habits. You can simulate different scenarios, such as donation bunching, and compare how these strategies impact your taxes year over year. This is particularly useful if your income varies, as it helps you time larger contributions for maximum tax benefit.

One standout feature is the "deduction gap" calculation. This shows the difference between your non-charitable itemized deductions and the standard deduction, helping you decide whether itemizing is worth it. For 2026, the app even includes the new above-the-line deduction - $1,000 for singles and $2,000 for joint filers - so you can determine the best approach for minimizing your tax liability[17].

Easy Receipt Management and Documentation

Keeping thorough records is essential for staying compliant and ensuring you get the most out of your deductions. Deductible.me makes this simple by allowing you to log donations instantly. Just snap a photo of your receipt or upload a PDF, and the app creates a permanent digital record.

For non-cash donations, the app goes a step further. It lets you upload photos of the items and note their condition - like "Excellent", "Good", or "Fair" - which is key for defending their fair market value if audited[21][22]. The app even uses a built-in valuation database to suggest fair market values based on current thrift-store resale prices, taking the guesswork out of the process. If you make a single donation of $250 or more, the app reminds you to request the required acknowledgment from the charity before filing your taxes[21].

With unlimited donation tracking and receipt storage included in the Premium plan, Deductible.me keeps all your records organized and ready for tax season. Plus, it ensures compliance with both federal and state rules, giving you peace of mind.

Conclusion

Key Points for Donors

State tax laws differ significantly, with various rules on deductions and credits that donors need to understand. For example, California, Colorado, and New York impose specific limits on deductions, each using unique thresholds and reduction formulas[2].

On the federal side, changes are on the horizon. Starting in 2026, the One Big Beautiful Bill Act will introduce a 0.5% AGI floor for itemizers, meaning only contributions exceeding this amount will be deductible. Additionally, the maximum tax benefit will be capped at 35%[2][5]. For non-itemizers, a new above-the-line deduction will allow $1,000 for singles and $2,000 for joint filers[5].

Strategic planning is key to navigating these changes. Seniors aged 70½ or older can benefit from Qualified Charitable Distributions, which permit transfers of up to $100,000 directly from an IRA to a charity without increasing taxable income[4][5].

These state and federal variations underscore the importance of having tools and strategies in place to simplify the process.

Start Maximizing Your Deductions Today

Understanding state tax rules and federal changes can feel overwhelming, but managing them doesn’t have to be. Deductible.me makes the process easier by tracking your donations, calculating state-specific deduction limits, and ensuring you meet IRS requirements. Its AI-powered valuation tool eliminates uncertainty around non-cash donations, while advanced analytics help you explore strategies like donation bunching.

For just $2/month, Deductible.me's Premium plan offers unlimited donation tracking, detailed analytics, and tools to set and monitor annual giving goals. Whether you’re navigating California’s AGI-based reduction rules or Colorado’s deduction caps, Deductible.me organizes your records and helps you make the most of your tax savings. Turn charitable giving into a smarter part of your financial plan with Deductible.me.

FAQs

Will my state tax credit reduce my federal charitable deduction?

If the state tax credit you receive exceeds 15% of your charitable contribution, IRS rules require you to adjust your federal deduction. Specifically, you'll need to reduce your federal deduction by the amount of the credit. This adjustment ensures your deductions align with federal guidelines for charitable contributions.

Can I itemize on my state return but not on my federal return (or vice versa)?

Yes, you can. State and federal deductions often have different rules for eligibility and amounts because each state establishes its own guidelines independently from federal law. This means it's possible to qualify for itemizing deductions on one return but not on the other.

How should I plan donations for the 2026 0.5% AGI floor?

To get the most out of deductions under the 2026 law, make sure your donations exceed 0.5% of your Adjusted Gross Income (AGI), as only the portion above this limit will qualify as deductible. If you’re taking the standard deduction, you might still benefit from a non-itemizer deduction of $1,000 for single filers or $2,000 for joint filers. It’s a good idea to review your yearly giving plan to stay within the rules and make the most of these benefits.