5 Tax Benefits of Donor-Advised Funds

[intro]

Donor-Advised Funds (DAFs) are a simple way to give to charity while enjoying tax advantages. Here's why they're worth considering in 2026:

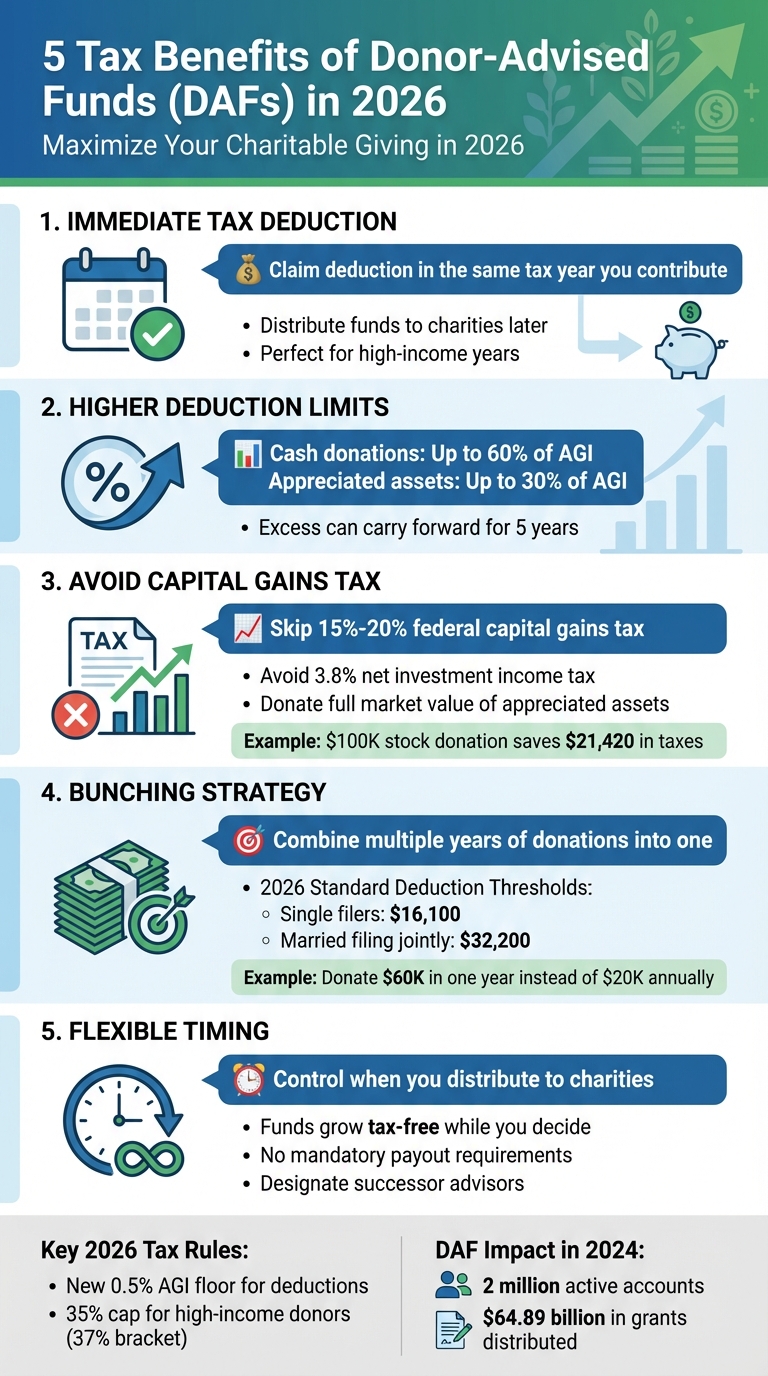

- Immediate Tax Deduction: Get a deduction in the same year you contribute, even if you distribute funds later.

- Higher Deduction Limits: Deduct up to 60% of your Adjusted Gross Income (AGI) for cash donations and 30% for appreciated assets.

- Avoid Capital Gains Tax: Donate appreciated assets directly to skip capital gains taxes and maximize your impact.

- Bunching Strategy: Combine multiple years of donations into one to exceed the standard deduction threshold.

- Flexible Timing: Decide when and how much to grant to charities while funds grow tax-free.

With the new 2026 tax rules, including a 0.5% AGI floor for deductions, DAFs offer a practical way to optimize your giving and tax savings.

5 Tax Benefits of Donor-Advised Funds in 2026

Donor Advised Funds Explained: Maximize Tax Deductions on Charitable Giving

sbb-itb-e723420

1. Get an Immediate Tax Deduction

One standout benefit of donor-advised funds (DAFs) is the ability to claim an immediate tax deduction when you make a contribution. Once you transfer your donation to a DAF, it becomes an irrevocable gift to a 501(c)(3) public charity. This means you can deduct the donation in the same tax year, regardless of when the funds are ultimately distributed to your chosen charities.

This flexibility is especially useful during high-income years - like after selling a business, receiving a significant bonus, or experiencing an exceptionally profitable year. You get the tax benefits right away, while your funds can grow tax-free until you're ready to support the causes you care about, whether that's months or even years later.

"The primary function of a DAF is to separate the timing of your tax deduction from the eventual distribution of funds." - AccountingInsights Team [5]

Here’s how deductions work:

- For cash contributions, you can deduct 100% of the amount transferred.

- For long-term appreciated assets, you can deduct their full fair market value.

To claim these deductions, itemize them on Schedule A of your tax return. For contributions of $250 or more, ensure you have a written acknowledgment from the DAF sponsor. Non-cash assets over $500 require IRS Form 8283, and for non-publicly traded assets valued above $5,000, a qualified appraisal is necessary.

Need help managing your deductions? Check out Deductible.me to simplify tracking and organizing your charitable contributions.

Up next: Discover how DAFs let you deduct up to 50% of your adjusted gross income.

2. Deduct Up to 60% of Your Adjusted Gross Income

Donor-advised funds offer a great way to reduce your tax burden with generous deduction limits. Thanks to the One Big Beautiful Bill Act, which takes effect in 2026, you can deduct cash contributions to a donor-advised fund up to 60% of your adjusted gross income (AGI). This makes it an appealing option for those looking to maximize their tax savings [4][9].

For donations involving appreciated assets - like stocks, real estate, or cryptocurrency that you’ve held long-term - the deduction limit is 30% of your AGI [7]. A real-world scenario helps illustrate how this works.

National Philanthropic Trust shared an example in January 2026: A donor contributed $100,000 in long-term appreciated stock with a $10,000 cost basis. By donating the stock directly, the individual avoided $21,420 in capital gains taxes. This meant the entire $100,000 could go toward charitable causes, compared to just $78,580 if the donor had sold the stock and donated the after-tax proceeds [1].

If your contributions exceed these limits, don’t worry - you can carry forward the excess for up to five years. However, keep in mind the new 0.5% AGI floor. For instance, if your AGI is $1 million, an initial contribution of $5,000 won’t provide any tax benefit [7][8][9].

To make the most of these deductions, consider using tools like Deductible.me. This app simplifies charitable giving and helps you optimize your tax benefits.

3. Avoid Capital Gains Tax on Appreciated Assets

Donating appreciated assets directly to a donor-advised fund (DAF) can help you sidestep capital gains taxes while securing an immediate tax deduction based on the asset's full market value.

When you sell appreciated assets, you're typically hit with a federal capital gains tax of 15%-20%, plus a 3.8% net investment income tax[1]. However, by donating the asset directly to a DAF, which is classified as a 501(c)(3) public charity, the fund can sell the asset without paying any capital gains tax. This means the entire value of the asset goes toward supporting charitable causes.

"If a donor were to liquidate their assets and later donate the proceeds to their DAF, the amount would be reduced by capital gains tax, leaving less money available for philanthropy." – National Philanthropic Trust[1]

Timing matters here. To maximize the benefit, you must have held the asset for more than one year. Assets held for a year or less only qualify for a deduction based on their original cost basis[1]. When donated directly, the amount available for charitable purposes can increase by more than 20% compared to selling the asset and donating the after-tax proceeds[1].

A key tip: never sell the asset before donating it, as this triggers capital gains taxes. If you're considering donating real estate, start the process 3–6 months ahead to meet due diligence requirements and ensure the property is debt-free[6].

4. Bunch Multiple Years of Donations Into One Tax Year

Bunching donations is a strategy where you combine several years' worth of charitable contributions into a single tax year to exceed the standard deduction threshold. For 2026, that threshold is set at $16,100 for single filers and $32,200 for married couples filing jointly[11]. If your annual charitable contributions, along with other deductions like mortgage interest and state and local taxes, don't surpass these amounts, you might miss out on potential tax savings. This approach can help you unlock immediate tax benefits.

Here’s how it works: Instead of donating $20,000 annually, you could contribute $60,000 in one year to a donor-advised fund (DAF). This allows you to claim a large itemized deduction in that year, and then take the standard deduction in subsequent years while continuing to recommend grants from your DAF to your chosen charities. By combining this large contribution with other deductions - such as mortgage interest - your itemized deductions can far exceed the standard threshold, resulting in significant tax savings over multiple years.

"Bunching donations can push your itemized deductions above the standard deduction threshold in one year, allowing you to claim a tax benefit that you might otherwise miss if your donations were spread out over multiple years." – Jewish Community Foundation, Inc.[10]

This strategy becomes even more effective under the One Big Beautiful Bill Act, which allows deductions only for contributions exceeding a 0.5% AGI floor, with a 35% cap for those in the 37% bracket[23,27]. These limits highlight the importance of bunching donations for better tax planning. To make the most of this approach, consider pairing your large DAF contribution with other deductible expenses in the same year. Additionally, transferring appreciated securities at least two weeks before December 31 ensures timely processing and maximizes your deduction benefits[12].

A donor-advised fund not only helps you secure a larger tax deduction in a single year but also ensures steady financial support for your favorite nonprofits over time[26,28]. Tools like Deductible.me can help you track and plan your charitable contributions, making it easier to implement this strategy and optimize your tax savings effectively.

5. Control When You Give to Charities

Donor-Advised Funds (DAFs) give you the freedom to separate the timing of your tax deduction from when you actually distribute funds to charities. When you contribute to a DAF, you secure an immediate tax deduction for that year, even if you decide later which organizations will receive the grants. This approach allows you to fine-tune your giving strategy over time.

"By controlling the timing of the DAF contribution, donors can manage the timing their own tax deductions while planning for future grantmaking to qualified charities." – National Philanthropic Trust [1]

This flexibility can be especially useful in years when your income is higher than usual - like after selling a business, receiving an inheritance, or enjoying strong investment gains. By making a large DAF contribution during such years, you can offset your taxable income while spreading out your charitable giving over time, based on your changing priorities. Unlike direct donations, which require you to allocate funds by the end of the year, a DAF allows you to "pre-fund" multiple years of giving with one transaction.

Another advantage is that assets in a DAF grow tax-free, potentially increasing the total amount available for grants without adding to your tax burden. Since DAFs don’t have mandatory payout requirements, you can support charities on your own terms - whether through smaller recurring grants or larger, strategic distributions.

DAFs also simplify the administrative side of charitable giving. The sponsoring organization handles tasks like verifying that recipient charities meet IRS qualifications as 501(c)(3) organizations. Plus, you get one consolidated tax receipt for your contribution, no matter how many charities ultimately benefit. You can even designate successor advisors to continue your philanthropic efforts, ensuring your giving aligns with your long-term goals.

How to Optimize Your DAF Strategy in 2026

To make the most of your Donor-Advised Fund (DAF) strategy in 2026, it's essential to adapt to the updated tax rules and take advantage of key opportunities.

Starting in 2026, a new 0.5% Adjusted Gross Income (AGI) floor will apply to charitable contributions [8].

"Any amount disallowed by the 0.5% floor is permanently lost. This rule creates a 'use it or lose it' scenario where the initial dollars of generosity are effectively taxed." – Arun KP, Tax Professional, Ourtaxpartner.com [8]

High-income donors will also face a 35% cap on tax benefits for charitable giving, which, when combined with the AGI floor, could reduce tax savings by 7%–10% compared to 2025. For instance, a $100,000 donation that generated $37,000 in tax savings in 2025 might only save about $33,250 in 2026 [14].

Here are some strategies to navigate these changes:

- Super-bunch donations: Consolidate several years' worth of contributions into a single year. This helps you surpass the 0.5% AGI floor and exceed the standard deduction thresholds, which are $16,100 for single filers and $32,200 for married couples filing jointly in 2026 [15]. This method aligns well with the benefits of a DAF, ensuring a more impactful deduction in one year.

- Donate appreciated securities: Contributing securities held for more than a year allows you to avoid capital gains taxes while deducting the full market value of the assets (up to 30% of your AGI).

- Qualified Charitable Distributions (QCDs): If you're 70½ or older, QCDs from an IRA remain a smart option. They bypass the AGI floor and the benefit cap, and the QCD limit will rise to $115,000 in 2026 [13].

- Keep documentation in order: For contributions over $250, secure a written acknowledgment. For noncash donations over $500, complete IRS Form 8283, and for assets valued over $5,000, obtain a qualified appraisal [15].

To simplify compliance and tracking, platforms like Deductible.me can assist with AI-driven item valuation, IRS-compliant reporting, and automated donation tracking. These tools help ensure your paperwork is in order while keeping your strategy on track.

Conclusion

Donor-advised funds (DAFs) offer a blend of immediate tax savings, capital gains tax avoidance, and flexible timelines, making them a smart option for charitable giving in 2026. With deduction limits reaching up to 60% of your adjusted gross income (AGI) for cash donations and 30% for appreciated assets, DAFs provide substantial tax advantages[3].

The bunching strategy is particularly useful under the updated 2026 tax laws. By grouping several years of donations into a single contribution, you can surpass the $16,100 standard deduction and meet the 0.5% AGI floor for charitable contributions[2][17]. This approach simplifies year-end planning while ensuring consistent support for the causes you care about.

DAFs also go beyond immediate benefits. The tax-free growth of funds allows for greater future charitable contributions, and the option to name successor advisors ensures your philanthropic vision can continue through generations[16].

With nearly 2 million active DAF accounts and $64.89 billion in grants distributed during fiscal year 2024, these funds have become a trusted choice for American donors[18][1]. Whether you're managing a financial windfall, planning for retirement giving, or instilling a spirit of giving in your family, a donor-advised fund offers the flexibility and tax efficiency to help you achieve your charitable goals for years to come.

For more tips and tools to optimize your deductions and simplify your giving, visit Deductible.me (https://deductible.me).

FAQs

How does the 0.5% AGI floor change my DAF deduction in 2026?

Starting in 2026, changes to the donor-advised fund (DAF) deduction rules will introduce a 0.5% adjusted gross income (AGI) floor. Essentially, only contributions that exceed 0.5% of your AGI will qualify for a deduction. This marks a shift from 2025, when every dollar donated was deductible from the start.

Which assets are best to donate to a DAF to avoid capital gains tax?

The most effective assets to contribute to a donor-advised fund (DAF) are appreciated assets that you've held for more than a year. These can include stocks, mutual funds, ETFs, or even real estate. Donating these types of assets allows you to avoid paying capital gains taxes, all while making a meaningful impact on the charitable organizations you support.

What paperwork do I need to claim a DAF deduction on my return?

When claiming a deduction for a donor-advised fund (DAF), you'll need to attach IRS Form 8283 to your tax return if your non-cash contributions exceed $500. This form asks for specific details, including:

- A description of the donated asset

- The dates you acquired and donated the asset

- The asset's fair market value

If you're donating appreciated securities or assets worth more than $500, Form 8283 is essential to validate your deduction.