What Is Donation Bundling? Tax Benefits Explained

Donation bundling, also known as "charitable bunching", is a tax-saving strategy where you combine multiple years of charitable donations into a single tax year. This approach helps you exceed the IRS standard deduction, allowing you to itemize deductions and reduce your taxable income. Here's how it works:

- Standard Deduction Thresholds (2026): $32,200 for married couples filing jointly, $16,100 for single filers.

- Why It Matters: If your total itemized deductions (including donations, mortgage interest, and state/local taxes) don't exceed the standard deduction, you won't get additional tax savings from charitable contributions.

- How Bundling Helps: By consolidating donations into one year, you can surpass the standard deduction and maximize tax benefits. In off-years, you simply take the standard deduction.

Key Benefits of Donation Bundling:

- Higher Tax Savings: Combining donations helps you qualify for itemized deductions, reducing taxable income.

- Avoid Capital Gains Taxes: Donating appreciated assets like stocks lets you deduct their full market value while avoiding taxes on gains.

- Flexibility Through Donor-Advised Funds (DAFs): Contribute to a DAF for an immediate tax deduction and distribute funds to charities over time.

This strategy is especially effective during high-income years or before retirement. Proper planning and tools like donor-advised funds can simplify the process. Always consult a tax professional to ensure compliance and maximize benefits.

Maximize your Tax Benefits by BUNCHING Charitable Donations!

sbb-itb-e723420

How Donation Bundling Works

Donation bundling is a strategy where you consolidate your charitable contributions into specific years. By focusing your giving during "on" years (when you itemize deductions) and using the standard deduction in "off" years, you can maximize your tax benefits.

Standard Deduction vs. Itemized Deductions

Taxpayers generally have two options: claim the standard deduction - a set amount that reduces taxable income - or itemize deductions by listing eligible expenses like mortgage interest, state and local taxes (SALT), and charitable donations. For 2026, the standard deduction remains at $16,100 for single filers and $32,200 for married couples filing jointly [1].

The catch? Charitable donations only reduce your taxable income if your total itemized deductions exceed the standard deduction. Otherwise, the standard deduction applies, and your charitable gifts don’t offer extra tax savings [3]. Caleb Lund, Director of Charitable Strategies Group at DAFgiving360, explains:

"Those who are charitably inclined and find themselves on the margin between taking the standard deduction or itemizing could maximize their tax benefits by 'bunching' two years of charitable contributions into one year." [2]

Before deciding to bundle, calculate your non-charitable deductions - such as mortgage interest and the SALT cap (set to $40,400 in 2026) - to determine how much charitable giving is needed to surpass the standard deduction threshold. This step ensures your donations are optimized for tax savings.

Timing Your Donations

Once you understand how deductions work, timing becomes key. By combining two or three years of charitable contributions into a single year, you can maximize your tax benefits [3]. For example, if you typically donate $15,000 annually, you could bundle by giving $30,000 in one year and skipping donations the following year.

This approach works especially well during high-income years, such as when you receive a large bonus, sell property, have RSU vesting, or inherit assets. Bundling in these years helps offset higher marginal tax rates. It’s also effective in the years leading up to retirement when your non-charitable itemized deductions are steady and close to the standard deduction threshold. Just ensure your donations are processed by January 1 of the high-giving year [3].

Using a Donor-Advised Fund (DAF) can make bundling even easier. A DAF allows you to secure an immediate tax deduction while giving you the flexibility to distribute funds to charities over time, ensuring consistent support [1].

For a more streamlined approach to managing your charitable contributions, tools like Deductible.me (https://deductible.me) can help track donations and ensure they meet IRS documentation requirements.

Tax Benefits of Donation Bundling

Donation bundling not only simplifies giving but also offers tax advantages that can make charitable contributions more efficient.

Exceeding the Standard Deduction

One major benefit of bundling donations is the ability to surpass the standard deduction, ensuring that every dollar donated reduces taxable income.

Take the example of Jane and Tom, a married couple with a $400,000 annual income. They typically donated $50,000 each year. In 2025, they chose to bundle two years' worth of donations - $100,000 - into a donor-advised fund. This move allowed them to bypass the upcoming 0.5% charitable floor and the 35% deduction cap set to begin in 2026. By bundling, they gained $8,225 more in tax benefits over two years compared to their usual annual giving approach[4].

Avoiding Capital Gains Taxes

Bundling donations using appreciated assets like stocks or real estate offers another significant tax advantage. When you donate long-term appreciated assets, you can deduct the full fair market value while also avoiding capital gains taxes.

For instance, imagine you bought stock for $10,000 that has grown to $50,000. By donating the stock, you eliminate a $40,000 capital gains tax liability and can still claim a $50,000 deduction. This strategy is particularly beneficial for those in higher tax brackets.

Understanding Charitable Deduction Limits

The IRS imposes limits on how much you can deduct based on your Adjusted Gross Income (AGI). Cash contributions are capped at 60% of AGI, while non-cash appreciated assets are limited to 30% of AGI[2][6]. If your bundled donations exceed these limits, you can carry forward the excess deductions for up to five years[2][6].

However, starting in 2026, new rules under the One Big Beautiful Bill Act will make deductions more complex. Contributions will only be deductible if they exceed 0.5% of your AGI[4][5]. Additionally, high-income earners in the 37% tax bracket will face a 35% cap on the tax benefit of itemized charitable deductions[5]. As Fidelity Charitable explains:

"High-income individuals who itemize deductions should carefully consider the timing and amounts of their giving... a bunching strategy or an approach of making larger gifts with less frequency can be more effective under the new rules."[5]

To maximize your deductions under these constraints, consider combining cash donations with appreciated assets. This allows you to fully utilize the 60% AGI limit for cash donations while avoiding capital gains taxes on non-cash contributions. Tools like Deductible.me (https://deductible.me) can help you track donations and ensure compliance with IRS documentation requirements - especially useful for managing complex bundling strategies across multiple years.

Next, we’ll explore actionable steps to implement these bundling strategies effectively.

How to Implement Donation Bundling

If you’re ready to put donation bundling into action, here’s a step-by-step guide to get you started.

Step 1: Calculate Your Annual Charitable Giving

Begin by adding up your non-charitable itemized deductions, such as mortgage interest and state and local taxes (SALT). Compare this total to the 2026 standard deduction - $16,100 for single filers and $32,200 for married couples filing jointly [2][1].

Next, perform a Gap Analysis to figure out how much more in charitable donations you’d need to surpass the standard deduction. For instance, if a married couple's non-charitable deductions total $25,000, they’d need at least $7,200 in additional donations to exceed the $32,200 threshold. Bundling donations for multiple years - say $60,000 over three years - can lead to significant tax savings [1].

It’s also smart to plan ahead. Look at your income over the next three to five years to pinpoint high-income years - like those with big bonuses, asset sales, or Roth conversions - when a larger deduction would be most beneficial. Keep in mind that cash donations are deductible up to 60% of your adjusted gross income (AGI), while appreciated non-cash assets held for more than a year are typically capped at 30% [2][7].

Step 2: Use a Donor-Advised Fund (DAF)

A Donor-Advised Fund (DAF) is an excellent tool for donation bundling. When you contribute to a DAF, you claim the full tax deduction in the year of the contribution, even though you can distribute the funds to charities over time. Financial Planner Joseph Powanda describes it well:

"Think of a DAF as your personal charitable brokerage account. You make a tax-deductible contribution to the fund today, but you can recommend grants to your favorite charities over many years." [8]

DAFs also allow your contributions to grow tax-free, increasing the potential for future giving. They’re particularly useful for donating complex assets like business interests, real estate, or cryptocurrency. These assets can be liquidated within the DAF without triggering capital gains taxes. If you’re planning to donate appreciated securities or other assets, start the transfer process at least 2–4 weeks before December 31 to ensure it’s completed by year-end [9][3].

Step 3: Bundle Donations in High-Giving Years

Timing is everything with donation bundling. Focus on years when your income is higher - such as when you receive bonuses, RSU vestings, or proceeds from asset sales - to maximize tax benefits [3].

For example, a couple with $28,000 in annual deductions and $15,000 in yearly donations could bundle two years’ worth of donations ($30,000) into one year. This would significantly increase their total deductions, leading to greater tax savings [2].

When bundling, prioritize donating appreciated assets, like stocks or ETFs held for over a year. By donating these directly to a DAF, you can avoid capital gains taxes and deduct the full fair market value of the assets [8][9]. If your bundled donations exceed AGI limits, the excess deduction can be carried forward for up to five additional tax years [2][7].

Step 4: Track and Document Your Donations

Proper documentation is critical. For any single cash or property donation of $250 or more, the IRS requires a contemporaneous written acknowledgment from the charity. Without this, your deduction could be denied [7]. For noncash contributions over $500, you’ll need to file IRS Form 8283. If the donation exceeds $5,000, a qualified appraisal is usually required - though publicly traded securities are an exception [7].

When donating appreciated securities, keep broker-to-charity transfer confirmations as proof. Additionally, verify the charity’s tax-exempt status using the IRS Tax Exempt Organization Search tool [7].

To streamline this process, tools like Deductible.me can help. They offer AI-powered valuation, IRS-compliant reporting (including Form 8283 preparation), and efficient tracking of documentation. This makes managing complex bundling strategies across multiple years much easier.

Donation Bundling Examples

Donation Bundling vs Annual Giving: Tax Savings Comparison

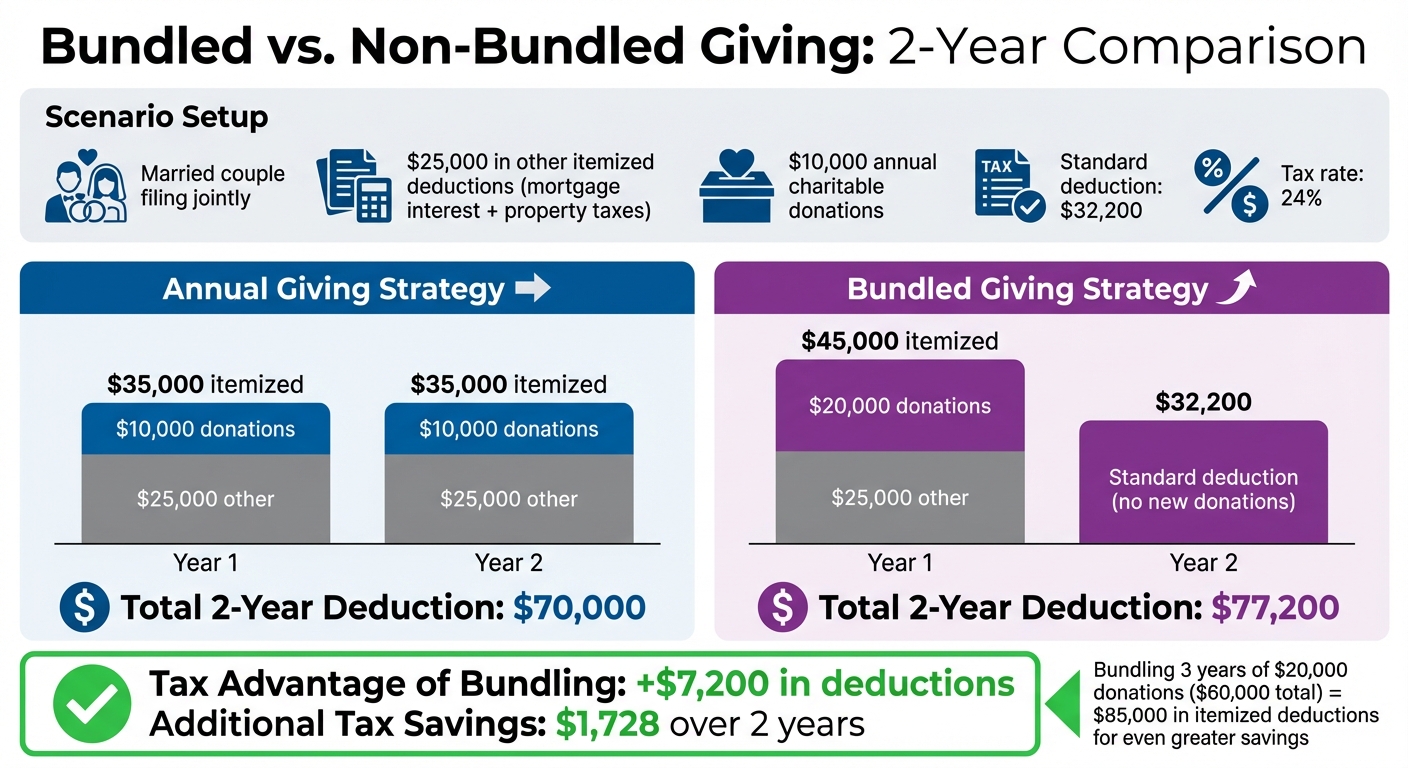

Bundled vs. Non-Bundled Giving Comparison

Let’s look at an example of how bundling donations can make a difference. Imagine a married couple with $25,000 in other itemized deductions (like mortgage interest and property taxes) who typically donate $10,000 to charity each year. The standard deduction for married couples filing jointly is $32,200.

If they stick to annual giving, they would itemize $35,000 each year ($10,000 in charitable donations plus $25,000 in other deductions), totaling $70,000 over two years.

Now, if they bundle their donations, they could combine two years’ worth of giving - $20,000 - into Year 1. That year, their itemized deductions would rise to $45,000 ($20,000 in charitable donations plus $25,000 in other deductions). In Year 2, they wouldn’t make any new charitable contributions and would instead take the $32,200 standard deduction. Over the two years, their deductions would total $77,200 - $7,200 more than the non-bundled approach.

At a 24% tax rate, this extra $7,200 in deductions translates to about $1,728 in tax savings over two years. The benefits can grow even further with a longer bundling period. For instance, if the same couple donates $20,000 annually and bundles three years of donations (totaling $60,000) into one year, they could see $85,000 in itemized deductions - leading to even greater savings [1].

| Giving Strategy (2-Year Period) | Year 1 Deduction | Year 2 Deduction | Total 2-Year Deduction |

|---|---|---|---|

| Annual Giving ($10k/year + $25k other) | $35,000 (Itemized) | $35,000 (Itemized) | $70,000 |

| Bundled Giving ($20k donation + $25k other) | $45,000 (Itemized) | $32,200 (Standard) | $77,200 |

| Tax Advantage of Bundling | +$7,200 |

Next, let’s explore how bundling works when donating appreciated assets.

Donating Appreciated Assets

Bundling isn’t just for cash donations - it also works for non-cash gifts like appreciated assets, which can unlock even more tax savings.

Here’s how it works: Imagine you bought stock for $10,000, and it’s now worth $30,000. Donating the stock directly to a charity or donor-advised fund allows you to deduct the full $30,000 while avoiding capital gains tax [10][11].

This approach offers a double benefit. For example, if you plan to bundle three years of donations totaling $60,000, donating appreciated stock held for more than one year lets you claim the full deduction (up to 30% of your AGI) [2][6]. This strategy has been especially effective for high earners in states like California, where bundling appreciated asset donations has resulted in additional tax savings ranging from $7,000 to $35,000 [3].

Conclusion

Donation bundling is a smart way to make the most of your charitable contributions while optimizing your tax savings.

By consolidating several years of donations, you can exceed the standard deduction threshold and itemize your deductions for greater tax relief. During non-bundled years, you can still benefit from the standard deduction. This approach not only boosts your tax benefits but also amplifies your charitable contributions.

Timing is everything when it comes to bundling. A Donor-Advised Fund allows you to claim a tax deduction upfront while distributing funds to charities over time, ensuring consistent support for the causes you care about. Bundling during high-income years can help offset higher tax rates, and donating appreciated assets adds another layer of tax efficiency by avoiding capital gains taxes while deducting the full market value of the asset.

Staying compliant with IRS rules is crucial, and tools like Deductible.me can streamline the process. With features like AI-powered valuation, IRS-compliant reporting, and tracking for annual giving goals, these tools make it easier to implement your bundling strategy effectively.

Whether you're bundling $20,000 or $60,000, the potential tax savings can be substantial. Work with a tax professional to tailor a bundling plan that aligns with your financial goals. With the right strategy, you can maximize your savings while maintaining meaningful charitable giving.

FAQs

Is donation bundling worth it for me?

If you donate $5,000 or more annually, donation bundling could be a smart move to explore. This approach allows you to surpass the standard deduction threshold, unlocking greater tax savings. By bundling your contributions, you might reduce your taxable income by thousands, making it an appealing option for individuals or families looking to get the most out of their charitable giving.

How many years of donations should I bundle?

To get the most out of your tax benefits, try bundling your charitable donations from 2 or 3 years into a single year. This strategy can help you surpass the standard deduction threshold, making your contributions more tax-effective. By planning your giving this way, you can align your generosity with smarter tax savings.

Can I bundle donations without skipping support for my charities?

When it comes to supporting your favorite charities, you don't have to sacrifice the impact of your donations to maximize tax benefits. By bundling several years' worth of contributions into a single year, you can potentially qualify for larger tax deductions. This approach ensures that your chosen organizations still receive the same total support over time, while you take advantage of optimized tax savings. It's a win-win strategy for both you and the causes you care about.