Checklist for Donation Bunching Success

Donation bunching is a tax strategy that helps you maximize savings on charitable contributions by grouping multiple years of donations into one tax year. This method is especially useful if your regular annual donations don’t exceed the standard deduction threshold. Here’s the key takeaway:

- How It Works: Combine 2–3 years of donations into one year to surpass the standard deduction threshold. In off years, take the standard deduction.

- Why It Matters: For 2026, the standard deduction is $16,100 (single) or $32,200 (married filing jointly). If your itemized deductions don’t exceed these amounts, bunching can make itemizing worthwhile.

- Who Benefits: Consistent donors, especially those with annual donations between $5,000–$15,000, high-income earners, or individuals nearing retirement.

- Best Tools: Donor-Advised Funds (DAFs) allow you to claim an immediate tax deduction while distributing funds to charities over time.

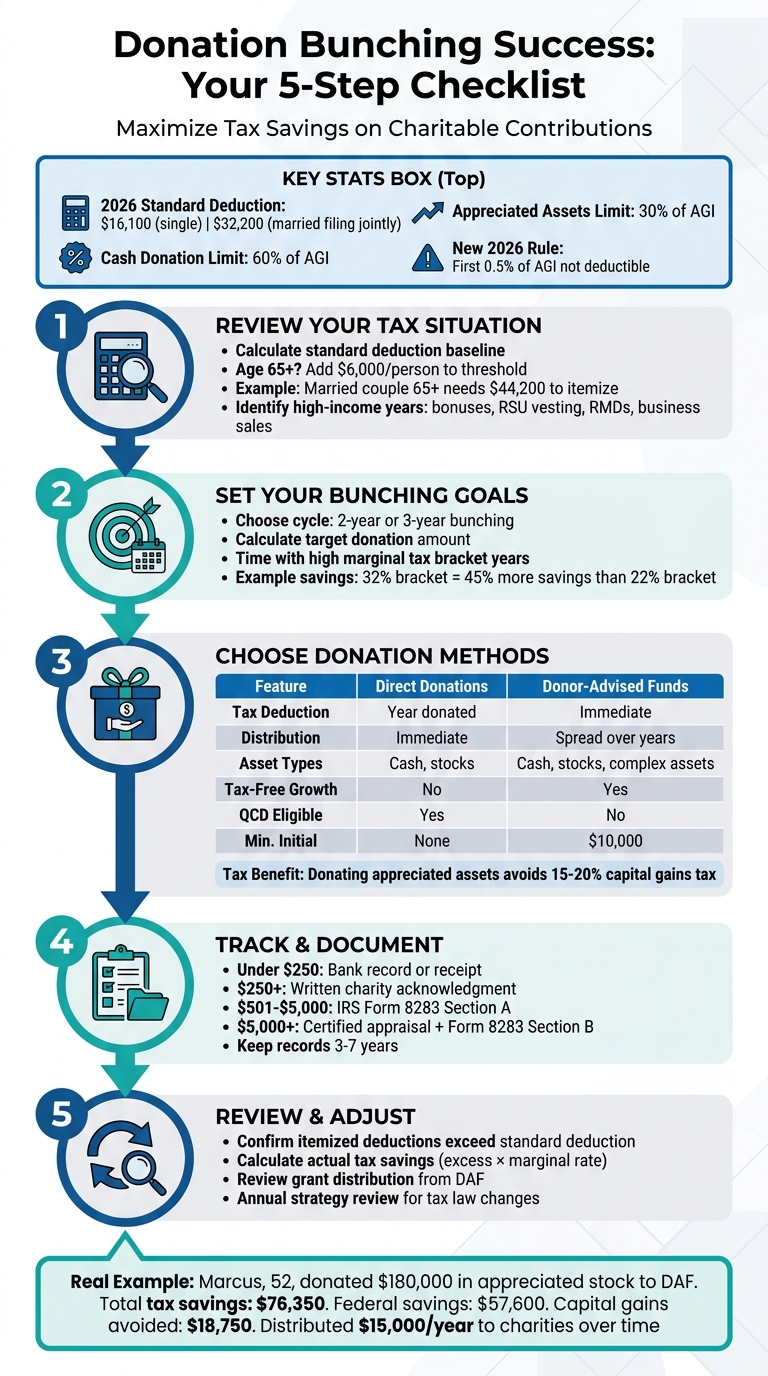

5-Step Donation Bunching Strategy for Maximum Tax Savings

Charitable Contributions (Part 1) | Bunching | DAF | QCD | Giving

sbb-itb-e723420

Step 1: Review Your Tax Situation

Start by taking a close look at your tax situation to see if donation bunching could save you more than the standard deduction. Break down your usual deductions and income trends to figure out how this strategy could fit into your overall tax plan.

Calculate Your Standard Deduction

Add up your typical itemized deductions, such as mortgage interest, state and local taxes (SALT), medical expenses over 7.5% of your adjusted gross income (AGI), and your regular charitable contributions. Compare that total to the standard deduction threshold.

If you're 65 or older, you can add up to $6,000 per person (or $12,000 for couples) to your standard deduction [4]. For instance, a married couple both aged 65 or older would need their itemized deductions to exceed $44,200 in 2026 to make donation bunching worthwhile, rather than just the base $32,200.

Also, keep in mind the 0.5% AGI floor starting in 2026. This means the first 0.5% of your AGI in donations won’t count as deductible [3]. For example, if your AGI is $400,000, the first $2,000 of your charitable donations wouldn’t qualify for a deduction.

Forecast Income and Deduction Patterns

Once you’ve calculated your deductions, take a closer look at your income trends. Identify years where your income is likely to spike - such as from bonuses, stock vesting, or required minimum distributions (RMDs) - and plan your bunched donations for those high-income years. These years are ideal for bunching because the deductions will offset income taxed at a higher marginal rate. Common income triggers include:

- Year-end bonuses

- Stock option or RSU vesting

- Business or real estate sales

- Roth IRA conversions [2]

If you're approaching age 73, remember that RMDs can significantly increase your taxable income. The year you start taking RMDs could be a great time to bunch donations [2]. Similarly, if you’re in your peak earning years before retirement, bunching now might offer better tax benefits than waiting until your income decreases.

For example, if your fixed deductions like mortgage interest and SALT already total $25,000 as a married couple, you’d only need to bunch enough charitable gifts to cover the remaining $7,200 gap to exceed the $32,200 standard deduction [2].

Step 2: Set Your Bunching Goals

Once you’ve got a handle on your tax situation, the next step is to create a plan. Clear goals can help you make the most of your tax benefits while staying committed to your charitable giving.

Define Your Bunching Cycle

A common approach for many taxpayers is to follow a two-year cycle. In Year 1, you concentrate your charitable donations to exceed the standard deduction, and in Year 2, you take the standard deduction instead [2]. This strategy works particularly well if your annual itemized deductions are just below the standard deduction threshold.

The cycle you choose depends on how far you are from the threshold. If you’re close, a two-year cycle might do the trick. If the gap is larger, bunching three years of donations into one might make more sense. High-income years - often caused by events like stock option vesting, large bonuses, business sales, or rebalancing your investment portfolio - are ideal times to bunch your giving [2]. Once you’ve identified the right timing, calculate the exact donation amount needed to close the gap.

Set a Target Donation Amount

Start by figuring out how much you need to donate to surpass the standard deduction. Subtract your non-charitable deductions (like mortgage interest and state and local taxes) from the standard deduction. For instance, if your mortgage interest and SALT deductions total $25,000, you’d need about $8,750 in charitable donations to exceed the threshold.

Don’t forget the IRS limits on deductions: cash donations are generally capped at 60% of your adjusted gross income (AGI), while donations of appreciated assets are limited to 30% of AGI [2].

Align with Financial Milestones

Timing is everything. Aim to bunch your donations during years when you’re in a higher marginal tax bracket. For example, a deduction in a 32% bracket provides about 45% more tax savings than the same deduction in a 22% bracket [8]. High-income periods - like when you receive year-end bonuses, RSU vesting, Roth IRA conversions, or proceeds from a business sale - are perfect opportunities for this strategy [2].

In 2026, Marcus, a 52-year-old e-commerce entrepreneur with $520,000 in AGI, donated $180,000 in appreciated company stock to a Donor-Advised Fund (DAF) during a high-income year. This move saved him $76,350 in total taxes: $57,600 in federal tax savings and $18,750 by avoiding capital gains taxes. He then used the DAF to distribute his usual $15,000 annual donations to education nonprofits over the next several years [2].

If you’re nearing age 73, the year you begin taking Required Minimum Distributions (RMDs) could be an excellent time to bunch donations. RMDs can significantly increase your taxable income, making this a prime moment to use a DAF to donate assets with large unrealized gains. This approach can help you avoid capital gains taxes, which can reach up to 23.8% [2].

Step 3: Choose Your Donation Methods

Now that you've set your bunching goals, it's time to decide how to donate in a way that maximizes your tax savings while supporting charities over time. Picking the right method is a crucial step in making the most of your contributions.

Consider Donor-Advised Funds (DAFs)

Donor-Advised Funds (DAFs) are a smart way to enhance the benefits of donation bunching. By using a DAF, you can claim an immediate tax deduction for the entire amount you contribute during the bunching year, while spreading out grants to charities over the following years. This approach lets you separate the timing of your tax deduction from when charities actually receive the funds.

"Donor advised funds are the ideal vehicle for implementing bunching strategies because they separate the timing of your tax deduction from the timing of your charitable distributions - giving you double the flexibility, and double the control."

Another advantage of DAFs is their ability to accept a wider range of assets, such as privately held stock, real estate, or cryptocurrency - assets that many individual charities cannot process. Contributions to a DAF can also grow tax-free through investments, potentially increasing the amount available for future grants. However, there are some limitations: most DAF sponsors require a minimum initial donation of $10,000, additional contributions of at least $1,000, and grant recommendations of $100 or more. Also, DAFs cannot accept Qualified Charitable Distributions (QCDs) from IRAs. If you're 70½ or older and want to use a QCD to meet your Required Minimum Distribution, you'll need to send the check directly to a qualified charity.

Weigh Cash vs. Non-Cash Donations

The type of asset you donate can significantly impact your tax benefits. Cash donations to public charities are deductible up to 60% of your adjusted gross income (AGI), while donations of appreciated assets held for over a year are capped at 30% of your AGI. Donating appreciated securities, in particular, offers a double tax benefit: you avoid capital gains tax on the appreciation and can deduct the asset's full fair market value.

"Eliminating the long-term capital gains tax - typically 15% or 20%, depending on your income level - can increase the charitable contribution available to charities by up to 20% as well as boost your tax deduction."

- Hayden Adams, Director of Tax Planning and Wealth Management, Schwab Center for Financial Research

If you own investments that have lost value, consider selling them first to claim the loss against other gains, then donating the cash proceeds. Starting in 2026, new rules under the One Big Beautiful Bill Act will require charitable donations to exceed 0.5% of your AGI to be deductible. Additionally, for those in the highest tax bracket, the benefit will be capped at 35%.

Compare Direct Donations vs. DAFs

Direct donations and DAFs each have their own strengths. Here's a quick comparison to help you decide:

| Feature | Direct Donations | Donor-Advised Funds (DAFs) |

|---|---|---|

| Ease of Use | Simple process | Requires setup and ongoing management |

| Flexibility in Granting | Funds go directly to charities | Grants can be spread over several years |

| Tax Deduction Timing | Deduction in the year funds are donated | Immediate deduction when funds are contributed |

| Asset Types | Primarily cash and public securities | Accepts cash, stocks, and more complex assets |

| Tax-Free Growth | No – funds are used immediately | Yes – contributions can grow tax-free |

| QCD Eligibility | Eligible for QCDs | Not eligible for IRA distributions |

| Administrative Costs | Minimal or none | May involve fees for administration and investments |

| Record Keeping | Requires receipts for each donation | Consolidates receipts into one statement |

If you're donating appreciated assets and want to support charities over several years, a DAF might be your best option. On the other hand, if simplicity or using Qualified Charitable Distributions is your priority, direct donations could be the way to go. Consider what aligns best with your financial goals and tax planning strategy.

Step 4: Track and Document Your Donations

Once your donation strategy is set, keeping thorough records is absolutely necessary to claim tax benefits. The IRS has strict guidelines, and even minor oversights can lead to deductions being denied. Proper tracking not only ensures compliance but also helps you claim the full deductions you're entitled to.

Keep Detailed Records

The type of documentation required depends on the size and nature of your donation. For cash contributions under $250, a simple bank record (like a canceled check or statement) or a receipt from the charity will do. However, for contributions of $250 or more, you’ll need a written acknowledgment from the charity, which must be obtained before you file your tax return [9].

Non-cash donations have additional requirements. For items valued between $501 and $5,000, you must complete IRS Form 8283 (Section A). If the value exceeds $5,000, a certified appraiser must provide a qualified appraisal, and you’ll need to fill out Form 8283 (Section B) [9]. Every receipt should clearly include the charity’s name, the donation date, a description of the item or amount given, and a statement indicating whether you received any goods or services in return [9]. If you did receive something in return - like a ticket to a charity gala - the charity must estimate the value of that benefit. Only the amount exceeding that value is deductible [9].

For non-cash items, it’s smart to take photos before donating to show their condition. The IRS only allows deductions for items in "good used condition or better" [9]. Experts recommend keeping all donation records for at least three years, though holding onto them for seven years is better if your finances are more complex [9]. These records are the backbone of a compliant and efficient donation strategy.

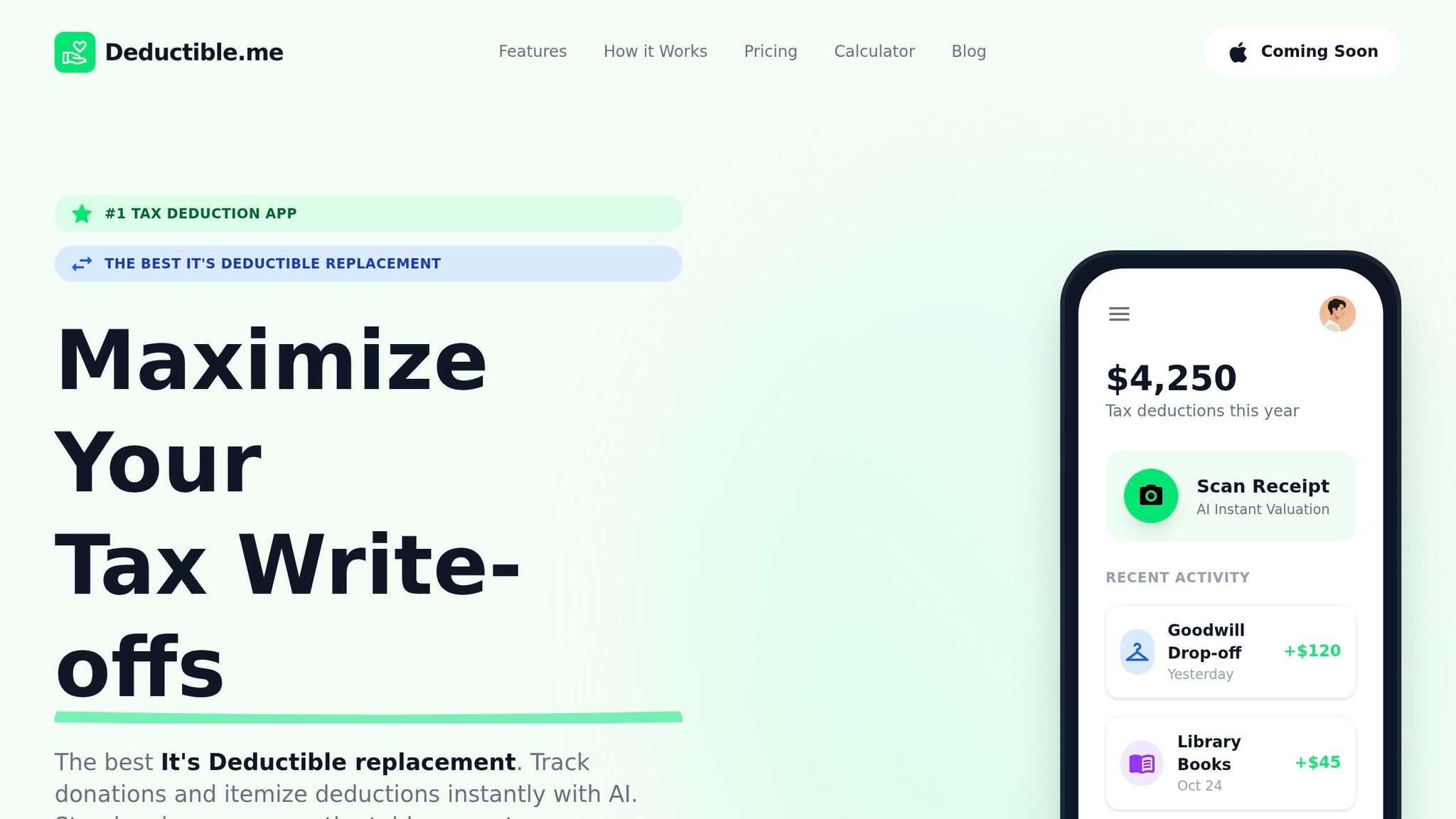

Simplify Tracking with Deductible.me

Manually keeping track of donations can be tedious and prone to errors. That’s where tools like Deductible.me come in. This platform lets you log donations instantly, upload photos for proof, and store digital receipts in one convenient place. Its AI-powered valuation feature even suggests fair market values for non-cash items based on their condition, saving you the hassle of researching values yourself.

When tax season rolls around, Deductible.me generates IRS-compliant reports that are ready to go with Form 8283. This can save you hours of effort and ensure your documentation is in order.

Stay Within Deduction Limits

As you track your donations, keep an eye on IRS limits to ensure you’re maximizing your deductions. Cash donations are capped at 60% of your AGI, while donations of appreciated assets are limited to 30% of your AGI [10]. If you exceed these limits in a single year, you can carry over the excess and deduct it over the next five years [10].

Looking ahead, starting in 2026, new rules under the One Big Beautiful Bill Act will require charitable donations to exceed 0.5% of your AGI to qualify for deductions [8]. This makes it even more important to monitor your AGI and donation totals throughout the year. Consulting a tax advisor can help you navigate these limits and optimize your tax benefits.

Step 5: Review and Adjust Your Strategy

Once you've implemented your donation bunching plan, it's time to step back and evaluate how well it's working. The main goal? Ensure your total itemized deductions in the bunching year surpass the standard deduction. For 2026, that means your deductions need to exceed $33,750 if you're married filing jointly or $16,900 if you're single [2]. Add up your bunched charitable donations, mortgage interest, and state and local taxes (up to the $10,000 cap), then compare the total to the standard deduction. If your total falls short, it's a sign your strategy might need some fine-tuning. Regularly reviewing your strategy ensures you're on track for future giving cycles.

Confirm Tax Savings

To see the actual tax benefit, calculate how much your itemized deductions exceed the standard deduction, then multiply that difference by your marginal tax rate. For example, if your itemized deductions are $5,000 over the standard deduction, and you're in the 24% tax bracket, your savings would be $1,200. Compare your total tax paid over a 2- or 3-year bunching cycle to what you'd pay if you stuck with the standard deduction every year. This comparison helps you determine whether your approach is delivering the savings you expected.

Review Your Grant Distribution

If you're using a Donor-Advised Fund, take a closer look at your grant distribution to ensure it aligns with your charitable goals. Adjust the timing or amounts of your grants if necessary to stay in sync with your giving intentions.

Adapt to Tax Law Changes

Tax laws can change, and so can your personal financial situation. That's why it's important to review your strategy annually. For instance, the standard deduction is adjusted for inflation each year [1], which could impact your calculations. Additionally, if you expect a significant income event - like a business sale, a large bonus, or RSU vesting - reassess your bunching strategy to align with that high-income year. This adjustment can help you maximize the value of your deductions [2]. To stay ahead, consider meeting with a tax advisor every fall to explore different scenarios and ensure your strategy continues to work in your favor.

Conclusion

This checklist is designed to help you implement an effective donation bunching strategy. It’s a process that requires consistent planning, attention to detail, and periodic adjustments to ensure you maximize your tax savings.

Start by evaluating your tax situation and income patterns to determine the best years for bunching. Aim to create a cycle that surpasses the 2026 standard deduction thresholds (e.g., $32,200 for married couples or $16,100 for singles) [5].

Choose the most effective donation methods for your situation. For instance, Donor-Advised Funds allow for immediate tax deductions while offering flexibility for future grant distributions. Alternatively, donating appreciated assets can help you avoid capital gains taxes and claim deductions based on their full fair market value [6][11].

Once you’ve selected your donation approach, focus on maintaining proper documentation. Keep IRS-compliant records such as receipts, acknowledgment letters, and appraisals. Tools like Deductible.me can simplify this process. Also, stay mindful of deduction limits - 60% of AGI for cash donations and 30% for appreciated assets [6].

Finally, review your strategy every year to adjust for tax law changes, such as the new 0.5% AGI threshold [7], and to account for changes in your financial situation. With careful planning and advice from experts, you can ensure your approach remains effective and impactful.

FAQs

How do I know if bunching will beat the standard deduction for me?

If you're wondering whether bunching could lead to better tax savings, here's how to evaluate it: Compare your total itemized deductions - including charitable contributions - over a span of several years to the current standard deduction. If your itemized deductions surpass the standard deduction in any given year, bunching might work in your favor. This strategy allows you to time your charitable contributions in a way that could help you save more on your taxes.

Should I bunch into a 2-year or 3-year donation cycle?

When deciding between a 2-year or 3-year donation cycle, it’s important to weigh your financial needs and tax objectives. Opting for a 2-year cycle might allow you to claim itemized deductions more frequently, potentially increasing your tax benefits. On the other hand, a 3-year cycle can offer more flexibility by spreading out donations and easing cash flow. To make the best choice for your situation, consider consulting a tax professional who can guide you based on your specific goals and circumstances.

When is a Donor-Advised Fund better than donating directly?

A Donor-Advised Fund can be a smart option if you're looking to align your charitable giving with tax-saving strategies. By bunching several years’ worth of donations into a single year, you may surpass the standard deduction threshold, enabling you to take advantage of itemized deductions. This method works well for those who want to time their contributions strategically to maximize tax benefits.