Charitable Bunching: Pros and Cons Explained

Charitable bunching is a tax-saving strategy that involves grouping multiple years of donations into a single year. This allows you to exceed the standard deduction threshold and claim larger itemized deductions. For 2026, the standard deduction is expected to be $32,200–$33,750 for married couples and $16,100–$16,900 for singles. Here’s a quick breakdown:

- How it works: Combine donations from two or more years into one year to surpass the standard deduction. Take the standard deduction in non-bunching years.

- Tax benefits: Higher deductions in bunching years can save thousands in taxes, especially for high-income earners.

- Cash flow: Requires upfront funds or appreciated assets, which may strain finances.

- Charity impact: May leave gaps in funding for nonprofits unless paired with a donor-advised fund (DAF).

- Annual giving alternative: Easier to manage and supports consistent funding for charities but may not provide extra tax savings if deductions fall below the standard threshold.

Quick tip: If your itemized deductions are close to the standard deduction, bunching may help maximize your tax savings. Tools like donor-advised funds can help balance tax benefits and steady charitable support.

1. Charitable Bunching

Charitable bunching involves combining several years of planned donations into a single tax year. The goal? To surpass the standard deduction threshold and gain a bigger tax benefit. In the years you don’t bunch, you simply take the standard deduction.

Tax Deduction Impact

By grouping two or three years' worth of donations into one year, you can itemize deductions in that year while reverting to the standard deduction in others. This approach can increase your total deductions over time.

Here’s how it works: cash donations to public charities are deductible up to 60% of your adjusted gross income (AGI), while contributions of appreciated assets, like stocks, are capped at 30% [1]. If your donations exceed these limits, the excess can be carried forward for up to five years.

But it’s not just about tax thresholds. Your cash flow and donation schedule also play a big part in making this strategy work.

Cash Flow Flexibility

To make charitable bunching work, you’ll need enough liquid cash or easily accessible appreciated assets to make a larger donation in one year. This strategy is especially useful in high-income years - like when you receive a big bonus, sell a business, or have significant investment gains - because the larger deduction can help offset a higher tax bracket. However, if your cash flow is tight, front-loading donations could create financial strain.

While your liquidity is crucial, it’s also important to think about how bunching might impact the charities you support.

Charitable Organization Stability

One downside of bunching is that it could leave charities with funding gaps during the years you don’t make donations. To address this, many donors turn to Donor-Advised Funds (DAFs). With a DAF, you can make a larger contribution in your bunching year, secure your tax deduction immediately, and then distribute smaller, steady grants to charities over time. This ensures nonprofits receive consistent support, even in your off years.

"DAFs are the perfect vehicle for bunching charitable deductions because you decouple the timing of tax deduction from charitable distributions."

– Uncle Kam

Planning Complexity

Charitable bunching isn’t a set-it-and-forget-it strategy - it requires careful planning. You’ll need to calculate your baseline itemized deductions, keep an eye on AGI limits, and ensure all bunched donations are made by December 31. The IRS also requires written acknowledgment from charities for any donation of $250 or more. And don’t forget, recent changes like the $40,000 SALT cap [6] make consulting a tax advisor essential.

sbb-itb-e723420

2. Annual Giving

Annual giving involves making steady contributions to charities each year and claiming those donations as itemized deductions on your tax return. Unlike the charitable bunching strategy, which focuses on maximizing tax benefits by grouping donations, annual giving maintains consistent support without altering deduction thresholds. However, this approach often doesn’t provide additional tax advantages if your total itemized deductions fall short of the standard deduction.

Tax Deduction Impact

Starting in 2026, the standard deduction will be $16,100 for singles and $32,200 for married couples. If your total itemized deductions, including annual charitable contributions, don’t exceed these amounts, there’s no extra tax benefit. For instance, if your deductions - combined with capped SALT and other eligible expenses - still fall below the standard deduction, annual giving won’t reduce your tax bill.

"For many, this difference can mean the gap between no tax benefit and capturing thousands in deductions."

Take the example of a married couple without a mortgage who donates $10,000 annually. With their SALT deductions capped at $10,000, their total itemized deductions would reach $20,000, which is far below the $32,200 standard deduction. Over three years, their $30,000 in donations would result in no additional tax savings. However, if they grouped those donations into a single year, they could save $4,320 in taxes by itemizing [7].

This highlights the trade-off between the tax savings of bunching and the steady cash flow benefits of annual giving.

Cash Flow Flexibility

One advantage of annual giving is its flexibility with cash flow. By spreading donations over several years, you avoid the need for a large upfront contribution or relying on liquid assets or appreciated investments. However, if your itemized deductions routinely fall below the standard deduction threshold, you forgo potential tax savings.

Charitable Organization Stability

Consistent annual donations also play a key role in supporting the financial stability of charities. Predictable contributions allow nonprofits to plan their budgets and operations more effectively [7]. Regular giving enables these organizations to develop and sustain programs with confidence, which is why many charities value donors who contribute consistently - even if the total amount given over time is the same.

Advantages and Disadvantages

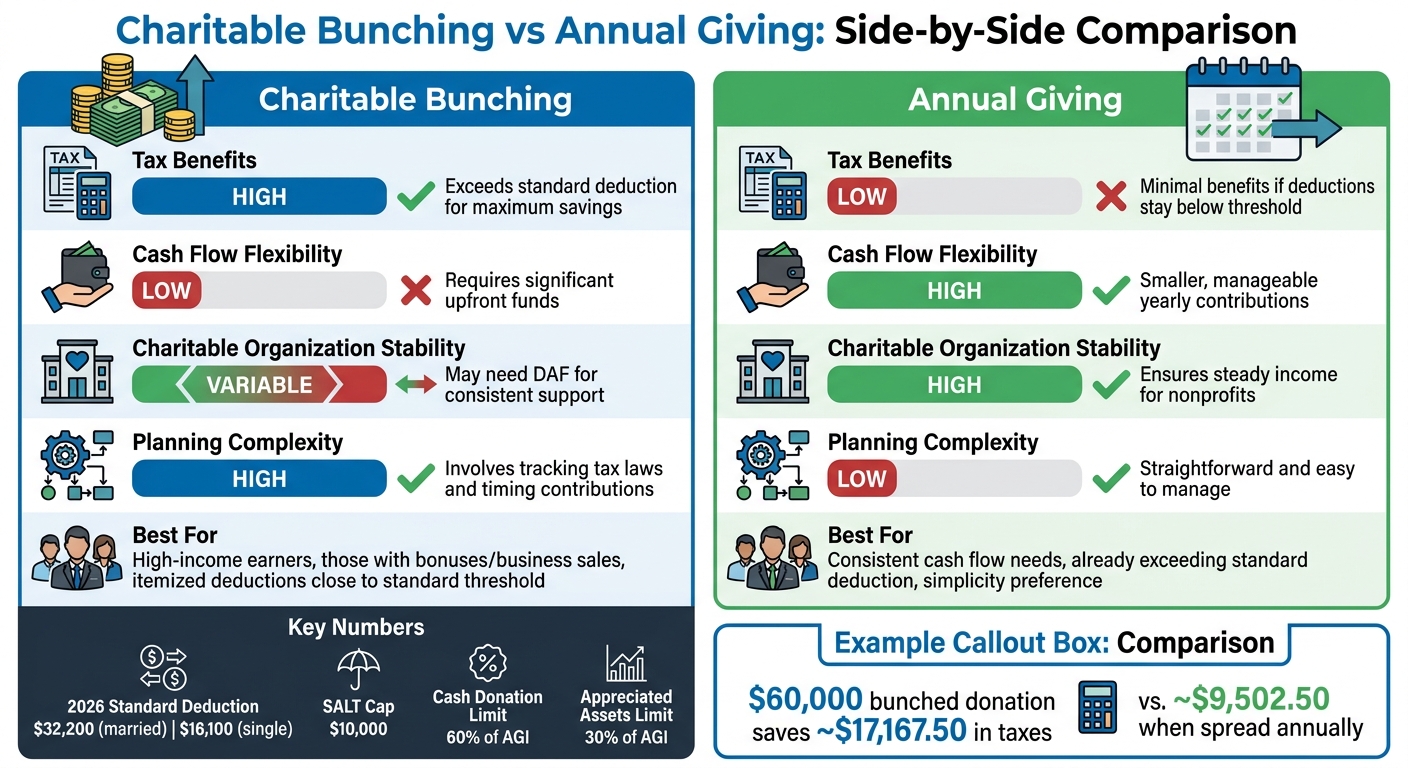

Charitable Bunching vs Annual Giving: Tax Benefits and Cash Flow Comparison

This section breaks down the pros and cons of charitable bunching versus annual giving, helping you weigh tax efficiency against simplicity and cash flow.

Charitable bunching is all about maximizing your tax deduction by grouping donations to push itemized deductions above the standard threshold - $32,200 for married couples or $16,100 for singles in 2026. This strategy makes the most sense if your usual deductions, like the $10,000 SALT cap and mortgage interest, are just shy of the standard deduction. For example, donating $60,000 in one year could save you around $17,167.50 in taxes, compared to about $9,502.50 when spread out annually [2].

But there’s a catch: bunching requires a significant upfront financial commitment. On the other hand, annual giving spreads out donations, making it easier to manage alongside other expenses. The downside? Many high-income earners won’t see much of a tax benefit if their total deductions stay below the standard threshold [7].

From a nonprofit’s perspective, steady annual donations make budgeting and program planning easier. In contrast, bunched donations might require the use of a donor-advised fund (DAF) to ensure consistent support. A DAF allows you to consolidate donations for tax benefits while still providing nonprofits with reliable funding [2][8].

Here’s a quick comparison of the two approaches:

| Feature | Charitable Bunching | Annual Giving |

|---|---|---|

| Tax Benefits | High; exceeds the standard deduction for maximum savings [2] | Low; minimal benefits if deductions stay below the threshold [7] |

| Cash Flow Flexibility | Low; requires significant upfront funds [3][7] | High; smaller, manageable yearly contributions [7] |

| Charitable Organization Stability | Variable; may need a DAF for consistent support [2][8] | High; ensures steady income for nonprofits [7] |

| Planning Complexity | High; involves tracking tax laws and timing contributions [3][7] | Low; straightforward and easy to manage [7] |

Bunching does come with added complexity. It requires careful planning - tracking deduction thresholds, managing a DAF, and timing contributions strategically, especially during high-income years like those with bonuses or business sales [3][7]. In contrast, annual giving is much simpler: donate, keep your receipts, and claim deductions. For those who prioritize ease and don’t need the extra tax savings, annual giving is the more straightforward option.

How to Implement and Track Your Donations

If you want to balance tax benefits with consistent charitable giving, these steps can help you manage your donations more effectively.

One option is to set up a donor-advised fund (DAF) through providers like Fidelity Charitable or T. Rowe Price Charitable. For example, Fidelity Charitable doesn’t require a minimum initial contribution to open a Giving Account [2], while The Signatry charges nothing to open or maintain an account [5]. Most DAF sponsors, however, ask for initial contributions ranging from $500 to $5,000, though some community foundations may require as much as $25,000 [4]. Once your DAF is ready, review your donation history to develop a timing strategy that works for you.

"Donor advised funds are an ideal vehicle for bunching donations because they provide immediate tax deductions for large contributions while allowing you to recommend grants to charities over multiple years." - Greater Houston Community Foundation [9]

Timing your donations can also increase your tax savings. Start by analyzing your donations over the past two to three years to determine if they exceeded the standard deduction threshold or provided any tax benefits [4]. Then, focus on high-income years - like when you receive bonuses, RSU vesting, or sell a business - so your donations can offset higher marginal tax rates [4]. Take Marcus, for instance, an e-commerce entrepreneur who, in 2026, earned $520,000 in adjusted gross income (AGI). He contributed $180,000 in appreciated company stock to a DAF, avoiding capital gains tax on $125,000 of appreciation. By itemizing his $180,000 deduction - far above the $33,750 standard deduction - he saved approximately $57,600 in federal taxes and $18,750 in capital gains taxes, totaling $76,350 in tax savings [4]. This example highlights how timing donations during high-income years can maximize your benefits.

Keep thorough documentation to stay IRS-compliant. This includes receipts, DAF confirmations, and valuation reports for non-cash donations [4]. Tools like Deductible.me can help by providing AI-powered valuations and generating IRS-compliant reports, such as Form 8283 for high-value items. The app also tracks your annual giving goals, helping you determine if you’re likely to exceed the standard deduction threshold - $16,100 for singles or $32,200 for married couples in 2026 [2]. This makes it simpler to decide whether to bunch contributions or stick with the standard deduction.

Finally, consult a tax strategist to model your potential savings and ensure your contributions stay within AGI limits - usually 60% for cash donations and 30% for appreciated assets [4]. While excess deductions can be carried forward for up to five years [4], proper planning helps you avoid leaving any unused. Donating appreciated assets is another smart strategy, as it allows you to bypass up to 23.8% in capital gains taxes while still claiming the full market value as a deduction [1].

Conclusion

Choosing the right charitable giving strategy hinges on your personal financial situation. Charitable bunching is particularly effective if your annual itemized deductions are close to the 2026 standard deduction thresholds [2]. This approach shines in high-income years - like when you earn bonuses, sell a business, or realize investment gains - because it helps offset a higher marginal tax rate while avoiding capital gains taxes on appreciated assets [1].

"Bunching doesn't mean you have to stop supporting your favorite charities annually. You can maintain giving consistency with a donor-advised fund." – Fidelity Charitable [2]

On the other hand, annual giving may make sense if your current itemized deductions already exceed the standard deduction without factoring in charitable contributions [7]. It’s also a straightforward option for those who value consistent cash flow and want to avoid the logistical steps involved with donor-advised funds.

For individuals aged 70½ or older with traditional IRAs, Qualified Charitable Distributions (QCDs) often provide a better alternative to bunching. QCDs reduce your adjusted gross income directly, offering a unique tax advantage [3]. However, if you’re in a high-earning phase and expect to be in a lower tax bracket during retirement, bunching now can maximize your long-term benefits [7].

To simplify your decision-making, tools like Deductible.me can help you determine whether you’re likely to exceed the standard deduction threshold. With AI-powered valuations and IRS-compliant reports, the app minimizes paperwork, allowing you to focus on your giving strategy. Ultimately, timing your donations to align with your financial goals is the key to optimizing your charitable tax benefits.

FAQs

How do I know if bunching will beat the standard deduction for me?

To figure out if bunching donations could work in your favor, start by estimating whether combining several years' worth of charitable contributions would surpass the current standard deduction. If it does, you can itemize deductions for that specific year while sticking to the standard deduction in the other years. This approach can help you optimize your tax savings, especially if your combined donations in the itemized year are well above the standard deduction limit.

What’s the safest way to bunch donations without hurting my cash flow?

The most effective way to maximize tax benefits from donations is by grouping multiple years of charitable contributions into a single year. This approach helps you surpass the standard deduction threshold, enabling you to itemize deductions. To manage this without straining your finances, consider planning in advance and using a donor-advised fund. This tool allows you to make a one-time donation upfront while distributing the funds to charities over several years, ensuring you maintain both tax advantages and financial flexibility.

Can I bunch for the tax break but still give to charities every year?

Yes, it's possible to group your charitable donations into a single year to take advantage of tax benefits while still supporting your favorite causes annually. In the years you don't itemize, you can opt for the standard deduction and continue giving regularly, even if those contributions don’t provide extra tax savings.