Ultimate Guide to Donating Appreciated Assets

Donating appreciated assets like stocks, real estate, or cryptocurrency can save you significant taxes while boosting your charitable contributions. Instead of selling these assets and paying capital gains tax, you can donate them directly to qualified charities. This allows you to:

- Avoid capital gains tax (up to 23.8% for high earners).

- Claim a deduction on the full market value of the asset if held for over a year.

- Support charities more effectively, as they receive the full value tax-free.

For example, donating $50,000 in appreciated stock (originally purchased for $20,000) directly could save over $7,000 in taxes compared to selling the stock first and donating cash. However, donations over $5,000 (except publicly traded securities) require a qualified appraisal and proper IRS documentation, such as Form 8283.

Key Takeaways:

- Donating appreciated assets maximizes tax benefits and charitable impact.

- Ensure assets are held for over a year to deduct full market value.

- Follow IRS rules for appraisals, forms, and documentation.

This approach is ideal for high-income years or when rebalancing investments. Tools like donor-advised funds or platforms like Deductible.me simplify the process and help track donations.

Donating Appreciated Assets

sbb-itb-e723420

Tax Benefits of Donating Appreciated Assets

Tax Savings Comparison: Selling vs Donating Appreciated Stock

This section highlights the key tax advantages of donating appreciated assets, emphasizing how this approach can enhance both your financial and charitable goals.

Avoiding Capital Gains Tax

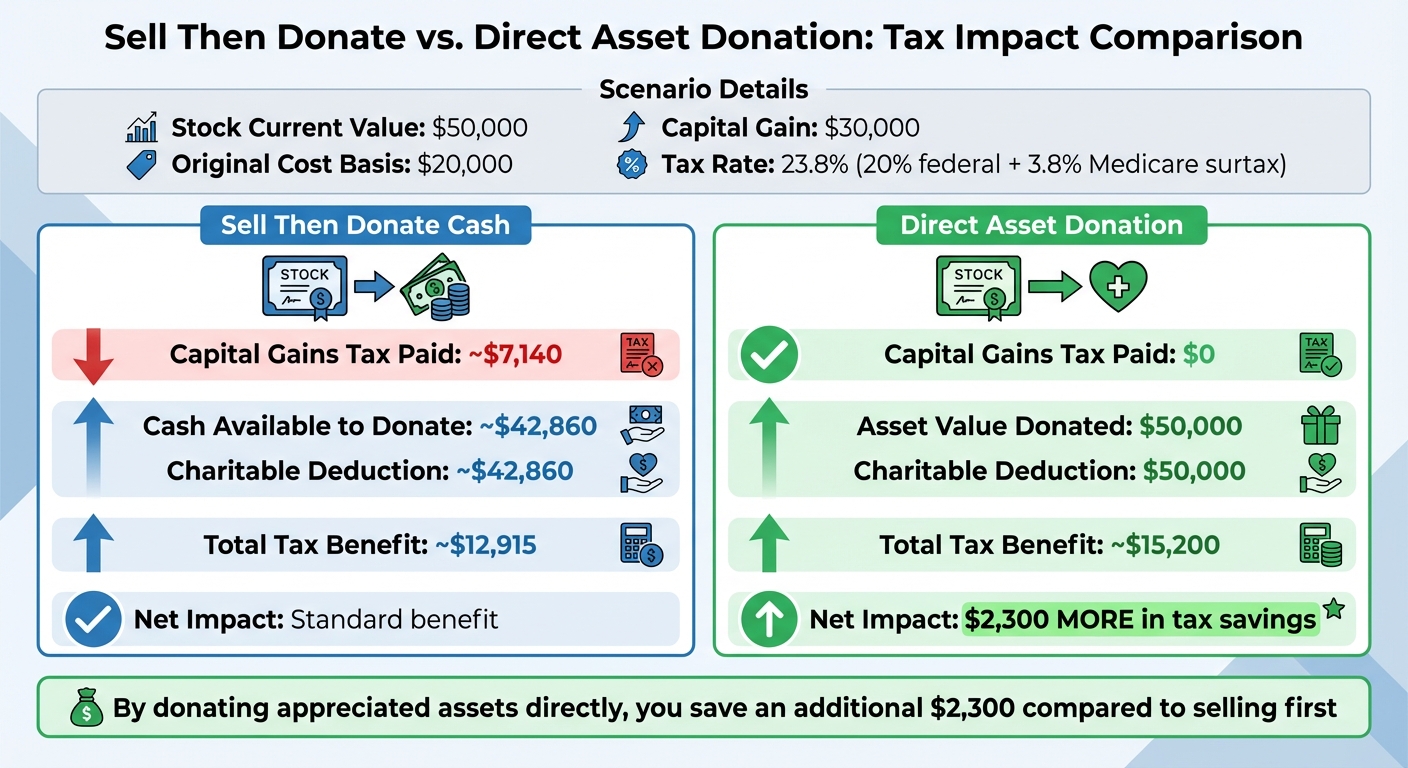

When you donate long-term appreciated assets directly to qualified charities, you can sidestep a taxable event entirely. Normally, selling such assets triggers federal capital gains tax (up to 20%), along with a 3.8% Medicare surtax for high earners, resulting in a combined rate of about 23.8% on your gains (excluding state taxes). For instance, imagine you own stock currently worth $50,000, which you originally purchased for $20,000. Selling it would result in approximately $7,140 in taxes on the $30,000 gain. However, by donating the stock directly, you avoid this tax burden entirely. Since charities are tax-exempt, they can sell the asset and retain 100% of the proceeds [7][8].

Deducting Fair Market Value

Another major benefit is the ability to deduct the full fair market value of the donated asset on your tax return, provided that you've held it for more than one year. If the asset is held for one year or less, the deduction is limited to its original cost basis [6][8].

There are, however, AGI-based limits to consider. For donations of appreciated assets to public charities or donor-advised funds, you can deduct up to 30% of your AGI. In contrast, cash contributions allow for a higher deduction limit of 60% of AGI. If your deduction exceeds these limits, the unused portion can usually be carried forward for up to five years [10][11][12].

Comparing Tax Savings: Appreciated Assets vs. Cash

The financial benefits of donating appreciated assets directly often surpass those of selling the asset and donating the after-tax cash. Let’s break it down with an example:

You have stock worth $50,000 with an original cost basis of $20,000. Selling it would result in $7,140 in taxes, leaving you with about $42,860 to donate. This would generate a total tax benefit of approximately $12,915. Alternatively, donating the stock directly avoids the $7,140 tax and allows you to claim a $50,000 deduction, resulting in a tax benefit of around $15,200 - $2,300 more than the sell-and-donate route.

As Natasha O'Yang, Regional Vice President at Fidelity Charitable, puts it:

"The charitable deduction is one of the most advantageous tax strategies available to people who make charitable giving part of their overall financial plan." [8]

| Action | Capital Gains Tax | Deduction Amount | Total Tax Benefit |

|---|---|---|---|

| Sell then Donate Cash | ~$7,140 | ~$42,860 | ~$12,915 |

| Direct Asset Donation | $0 | $50,000 | ~$15,200 |

(Note: Figures are based on a hypothetical scenario; see [8] for details.)

Despite these clear benefits, only 21% of donors who own appreciated assets have ever donated them directly, even though 80% of donors hold such assets. Donating in-kind could increase your charitable impact by as much as 20% compared to selling first [11].

These tax savings make donating appreciated assets an effective strategy. Tools like Deductible.me's AI-powered valuation and IRS-compliant reporting can help simplify the process of documenting your donations.

Which Assets Qualify for Charitable Donations

When it comes to charitable giving, the type of asset you donate can significantly impact both your tax benefits and the support you provide to your chosen cause. Here's a breakdown of common asset types that qualify for donations, along with key rules and considerations.

Publicly Traded Securities

Donating stocks, bonds, mutual funds, or ETFs listed on major exchanges is one of the simplest ways to give. These assets are easy to value, and you typically don't need a qualified appraisal [9][14].

To maximize tax benefits, transfer shares directly to the charity's brokerage account instead of selling them. This allows you to claim a deduction for the full market value while avoiding capital gains tax. Keep in mind, though, that the deduction is capped at 30% of your adjusted gross income (AGI), with any unused portion eligible for a five-year carryover [10][13].

Real Estate and Cryptocurrency

Real estate - whether it's land, residential, or commercial property - can also be donated, but it requires a qualified appraisal. Appraisals are typically based on comparable sales or the income capitalization method [9].

Cryptocurrency, such as Bitcoin, has become an increasingly popular donation option. Since the IRS treats crypto as property, it qualifies for similar tax benefits as stocks if held for more than a year. However, donations exceeding $5,000 require a qualified appraisal to validate your deduction [1]. If the charity you're supporting can't accept crypto directly, a donor-advised fund (DAF) can simplify the process [1][2].

Other Asset Types

Several other asset categories may be eligible for donation:

- Private Business Interests: These include closely held stock, S-corp shares, or partnership interests, all of which require a qualified appraisal [10][15].

- Art and Collectibles: Items like paintings, antiques, jewelry, rare books, and stamps can be donated if they meet specific condition standards. Donations valued over $500 require documentation, and art appraised at $50,000 or more may warrant a formal Statement of Value from the IRS [9].

- Intellectual Property: Patents and other IP rights may qualify based on their future earnings potential.

- Tangible Property: Cars, boats, and aircraft are also eligible for donation [9][5].

For donations to private non-operating foundations, the deduction limit is lower - capped at 20% of AGI compared to 30% for public charities [10].

| Asset Category | Valuation Method | Appraisal Required? |

|---|---|---|

| Publicly Traded Securities | Average of high/low price on transfer date [10] | No [9] |

| Real Estate | Comparable sales or income capitalization [9] | Yes [9] |

| Cryptocurrency | Market value at time of donation [1] | Yes, if >$5,000 [1] |

| Private Business Interests | Qualified appraisal [10] | Yes [10][15] |

| Art & Collectibles | Professional appraisal [9] | Yes, if >$5,000 [9] |

Before donating, confirm the recipient's status as a qualified 501(c)(3) organization using the IRS Tax Exempt Organization Search tool [4][10]. For more complicated assets, like those that small charities might struggle to process, a DAF can handle the liquidation and distribution for you [1][2]. Always ensure your donations meet IRS documentation and valuation requirements to avoid any issues later.

IRS Rules and Documentation Requirements

Navigating IRS rules is key to ensuring your noncash donation qualifies for a deduction. Proper documentation isn't just a formality - it’s what allows you to claim the full tax benefits of donating appreciated assets. Requirements depend on the value of your donation, and overlooking key details can lead to denied deductions or even penalties.

Valuation and Appraisal Requirements

If you're donating assets worth more than $5,000 (excluding publicly traded securities), you’ll need a qualified appraisal. This appraisal must be completed within 60 days before the donation and no later than your tax return due date. The appraiser should have recognized credentials and experience with your specific type of asset [16][18].

Publicly traded securities are a notable exception. Since their fair market value is readily available through exchange listings, an appraisal isn’t required, no matter the amount [17][18]. However, for other assets like real estate, cryptocurrency (over $5,000), private business interests, art, or collectibles, a qualified appraisal is mandatory.

Keep in mind: if you donate multiple similar items in a year, their total value determines whether an appraisal is required. For example, donating several items that collectively exceed $5,000 means you’ll need a single appraisal covering all of them [16].

Form 8283 and Required Documentation

Form 8283 is your go-to for reporting noncash donations. Here’s how to use it:

- Section A: For donations with deductions between $500 and $5,000. Publicly traded securities also belong here, regardless of their value [16][17].

- Section B: For deductions exceeding $5,000 (except publicly traded stocks). This section requires two signatures: one from a qualified appraiser (Part IV) and another from the charity (Part V). These signatures confirm receipt of the donation, not the appraised value [17].

For donations of $250 or more, you must also get a contemporaneous written acknowledgment from the charity. This acknowledgment should describe the donated property and note whether any goods or services were received in return [5][18]. High-value donations come with additional requirements: artwork valued over $20,000 requires a signed appraisal copy, while donations over $500,000 require the full appraisal report to be attached to your tax return [5][18].

Using tools like Deductible.me can help you stay on top of your documentation, making it easier to meet IRS standards and claim your deductions.

Common Compliance Mistakes to Avoid

A common misstep is failing to aggregate similar donations. For instance, donating $3,000 worth of books to one charity and $2,500 to another in the same year means the combined value exceeds $5,000, triggering the appraisal requirement - even though no single donation hits that threshold [16].

As Legacy Donation Appraisers explains:

"The most common mistake donors make is treating the appraisal as an afterthought - something to sort out after the donation has already been made" [16].

Other common pitfalls include:

- Missing the 60-day appraisal window: An appraisal outside this timeframe won’t be valid [16][19].

- Omitting the cost basis on Form 8283: Forgetting to include the original or adjusted cost basis can lead to a denied deduction [20].

- Misclassifying assets: Cryptocurrency and NFTs are not treated as publicly traded securities. Donations of these assets over $5,000 require a qualified appraisal and must be reported in Section B [16].

- Overstating value: Inflating a donation’s value can result in penalties. The IRS may impose a 20% accuracy-related penalty for underpaid taxes, which increases to 40% for gross valuation misstatements [16][18].

By addressing these common mistakes upfront, you can ensure your documentation meets IRS standards and avoid headaches later.

| Donation Value | Required Documentation | Appraisal Required? |

|---|---|---|

| $250 – $500 | Written acknowledgment from charity | No |

| $501 – $5,000 | Written acknowledgment plus Form 8283, Section A | No |

| Over $5,000 | Written acknowledgment plus Form 8283, Section B, and appraisal | Yes (except publicly traded stocks) |

| Over $500,000 | Written acknowledgment plus Form 8283, Section B, and full appraisal report | Yes |

Lastly, the IRS generally has three years to audit your valuation, but this period only begins once your donation is "adequately disclosed." Detailed descriptions and supporting documents from the start can protect you from prolonged scrutiny [18].

Best Practices for Donating Appreciated Assets

Following IRS guidelines can help ensure your donations are compliant while also maximizing potential tax benefits. Timing your contributions wisely, working with the right professionals, and keeping detailed records are key steps in this process.

When to Donate: Timing Strategies

The timing of your donation can significantly impact your tax savings. A popular approach is "bunching" donations, where you combine several years' worth of contributions into a single tax year. Starting in 2026, only charitable contributions exceeding 0.5% of your Adjusted Gross Income (AGI) will qualify for deductions [21][22].

As Garrett Harbron, J.D., CFA, CFP® from Vanguard points out:

"By consolidating contributions into one year, donors are more likely to surpass this threshold and maximize the tax benefit of their charitable efforts. This change makes strategic timing - such as bunching donations - more important than ever." [21]

High-income years or financial windfalls, like selling a business or an IPO, are ideal times to donate. For business owners, contributing appreciated private stock or pre-IPO shares before a sale or public offering can help avoid capital gains taxes on the highest valuation [22][23].

Steven Elliott, MST, CPA at Mercer Advisors, highlights another option:

"A donor-advised fund (DAF) lets you make a large gift in one year, claim the deduction immediately, and recommend grants later, with no time limitation for use." [22]

For those aged 70½ or older, Qualified Charitable Distributions (QCDs) offer a unique advantage. Starting in 2026, you can transfer up to $115,000 directly from an IRA to a charity. This satisfies Required Minimum Distributions (RMDs) without increasing your AGI [22][24].

Once you’ve determined the best timing for your donation, the next step is ensuring the process runs smoothly by collaborating with the right professionals and organizations.

Working with Charities and Tax Professionals

Before making a donation, confirm that the charity can accept complex assets. Use the IRS Tax Exempt Organization Search tool to verify the organization’s 501(c)(3) status [4].

For simpler assets like publicly traded securities, most established charities can process transfers through their brokerage accounts. However, for more intricate assets - such as real estate, cryptocurrency, or private stock - partnering with a donor-advised fund (DAF) provider with specialized expertise can simplify the process.

It’s wise to consult with tax professionals before donating, especially when dealing with non-cash assets. These transactions often involve legal, real estate, and tax complexities that require expert advice. Additionally, financial advisors can assist with strategies like resetting your cost basis after donating appreciated shares, which reduces future capital gains exposure [23].

Tools to Track and Document Donations

After coordinating with your charity and advisors, maintaining accurate records is essential. This includes documenting the asset’s cost basis, holding period, fair market value, and the necessary IRS forms.

Platforms like Deductible.me can simplify this process. Their tools include AI-powered valuation, IRS-compliant Form 8283 reporting, and receipt management. For those who make multiple donations throughout the year, the Premium plan ($2/month) offers unlimited tracking, annual goal monitoring, and advanced analytics to refine your giving strategy.

The platform’s receipt management system is particularly helpful for donations of $250 or more, ensuring you have the required acknowledgments for tax filings or potential audits.

For brokerage transfers, ensure your financial institution processes the donation as a direct transfer via the Depository Trust Company (DTC). This preserves the "in-kind" status of your gift, avoiding capital gains taxes triggered by a sale before transfer [14]. Keep records of the transfer date, as this determines the valuation date for your deduction. For publicly traded securities, the valuation date is typically when the stock is recorded on the corporation’s books [25].

Conclusion

This guide highlights how donating appreciated assets can amplify your charitable contributions while offering significant tax advantages. By donating these assets, you can sidestep capital gains taxes and claim a deduction based on their full fair market value.

To make the most of these benefits, it's crucial to follow IRS regulations carefully. Ensure that you hold assets for over a year, confirm the 501(c)(3) status of your chosen charity, secure qualified appraisals for donations exceeding $5,000, and properly complete Form 8283 to avoid IRS penalties, which can range from 20% to 40% [18]. Timing your donations strategically - such as grouping them together or donating during high-income years - can further optimize your tax savings, especially with the upcoming 0.5% AGI threshold starting in 2026 [3].

Keeping thorough records is another essential step. It simplifies tax preparation and safeguards you in case of an audit. Tools like Deductible.me can make this process seamless. With features like AI-powered valuation, IRS-compliant Form 8283 reporting, and receipt management, Deductible.me helps you stay organized. For just $2 per month with the Premium plan, you can track donations year-round and fine-tune your giving strategy. Revisit earlier sections or check out Deductible.me to put these strategies into action and maximize the impact of your charitable giving.

FAQs

How do I know if my asset is “long-term” for the full-value deduction?

A “long-term” asset is one you’ve owned for over a year before donating it. Assets like stocks or securities held for more than 12 months usually qualify for a deduction based on their full fair market value. Plus, donating these assets helps you sidestep capital gains tax.

What exact paperwork do I need for a noncash donation over $5,000?

For noncash donations exceeding $5,000, you must fill out Section B of IRS Form 8283 to document the donated property. Additionally, a qualified appraisal from a certified appraiser is required to establish the fair market value. This step is particularly important for valuable items such as real estate or collectibles. Make sure the appraisal is thorough and meets IRS guidelines to validate your deduction.

Should I donate through a donor-advised fund or directly to the charity?

When deciding between a donor-advised fund (DAF) and making a direct donation to charity, it all comes down to your financial priorities and tax goals.

A DAF can offer several perks. For example, you can avoid capital gains taxes when donating appreciated assets, enjoy flexibility in choosing when to distribute grants, and claim an immediate tax deduction at the time of your contribution. It’s a great option if you’re looking for strategic ways to manage charitable giving.

On the other hand, direct donations are straightforward and provide immediate support to the causes you care about. However, they don’t come with the same strategic tax benefits as a DAF.

If your primary focus is maximizing tax efficiency while maintaining flexibility, a DAF often comes out on top.