What should I choose for Tax Filing Status on my taxes?

Your tax filing status is one of the most important decisions when preparing your tax return. It directly impacts your standard deduction, tax brackets, and eligibility for credits. The IRS offers five filing status options based on your marital and household situation as of December 31 of the tax year:

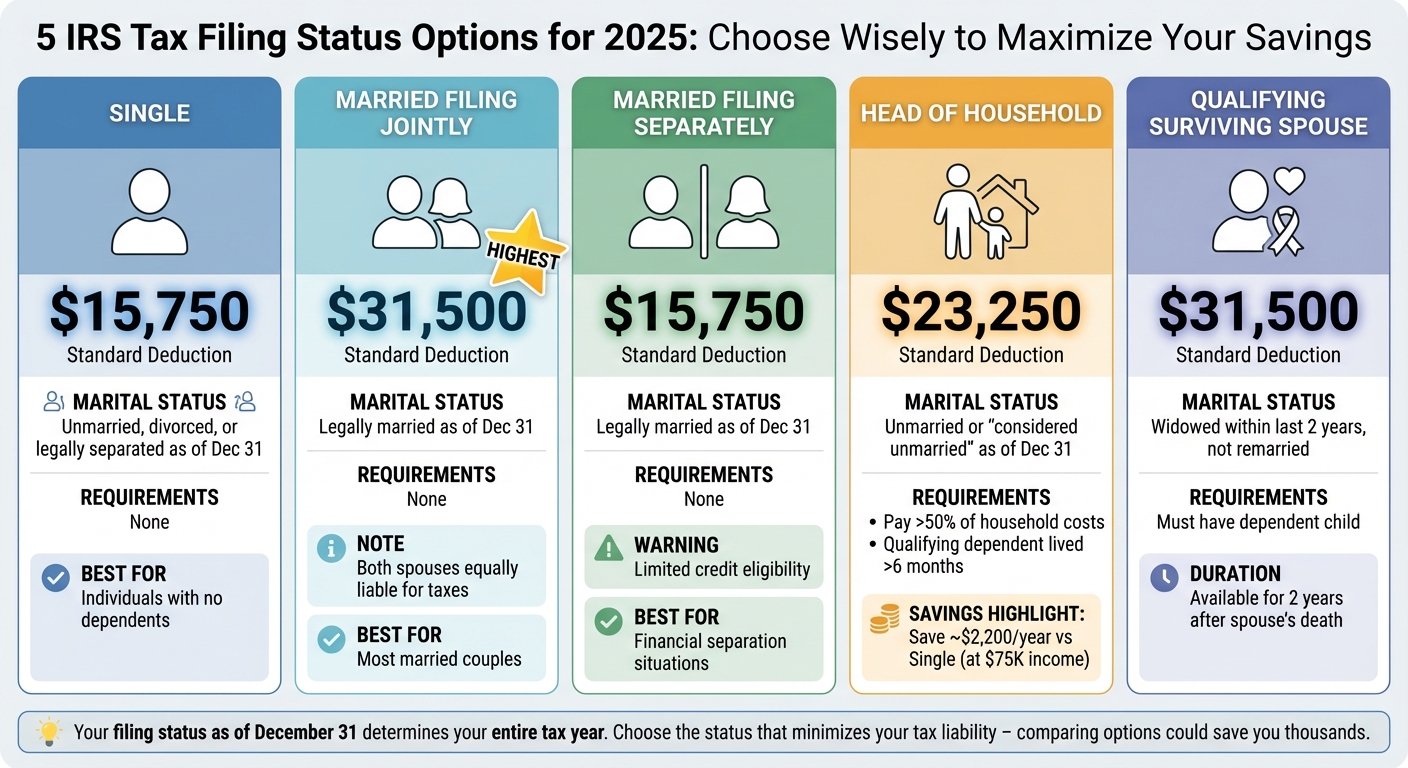

- Single: For those unmarried, divorced, or legally separated. Standard deduction: $15,750 (2025).

- Married Filing Jointly: Combines income and deductions for married couples. Standard deduction: $31,500.

- Married Filing Separately: Each spouse files their own return. Standard deduction: $15,750 but with limited credit eligibility.

- Head of Household: For those who pay over half of household costs and have a qualifying dependent. Standard deduction: $23,250.

- Qualifying Widow(er): Available for two years after a spouse's death if you have a dependent child. Standard deduction: $31,500.

Key takeaway: Choose the filing status that minimizes your tax liability. For example, filing as Head of Household instead of Single could save you around $2,200 annually if you earn $75,000. Always evaluate your situation and compare outcomes if multiple statuses apply.

2025 Tax Filing Status Comparison: Standard Deductions and Requirements

What to know about your tax filing status & what it means for your refund

sbb-itb-e723420

The 5 IRS Tax Filing Status Options

The IRS provides five filing status options, each with specific rules for eligibility. Your filing status is determined based on your situation as of December 31 and applies to the entire tax year. The choice you make can significantly influence your tax deductions, credits, and overall liability.

Single

The Single filing status applies if you're unmarried, divorced, or legally separated under a court decree as of December 31. If you don't meet the criteria for any other filing status, this is your default option. For the 2025 tax year, the standard deduction for Single filers is $15,750.

Married Filing Jointly

If you're legally married on the last day of the year, you can file under Married Filing Jointly. This status combines both spouses' income, deductions, and credits into one return. However, both individuals are equally responsible for any taxes, interest, or penalties owed. The standard deduction for this status is $31,500 in 2025, the highest among all filing options. Additionally, if your spouse passed away during the year and you haven’t remarried, you can still file jointly for that tax year.

Married Filing Separately

The Married Filing Separately status allows each spouse to file their own tax return, taking responsibility only for their individual tax liabilities. This option is often used in cases of financial separation or divorce proceedings. For 2025, the standard deduction is $15,750. However, there are trade-offs: if one spouse itemizes deductions, the other must do the same, and this status often disqualifies you from claiming certain credits like the Child and Dependent Care Credit or education-related credits.

Head of Household

To qualify as Head of Household, you must either be unmarried or "considered unmarried" as of December 31, pay more than half the expenses for maintaining your home, and have a qualifying dependent who lives with you for more than half the year. If you're married but separated, your spouse must not have lived in your home for the last six months of the year to meet the "considered unmarried" condition. For 2025, the standard deduction is $23,250. Notably, dependent parents don’t need to live with you as long as you provide over half of their financial support.

"Head of Household is perhaps the most overlooked filing status, but it offers higher standard deductions and lower tax rates compared to Single status." - Jacob Dayan, CEO, Community Tax, LLC [4]

Qualifying Widow(er)

The Qualifying Surviving Spouse status (previously called Qualifying Widow/Widower) is available for up to two years following the death of your spouse, provided you haven’t remarried and have a dependent child living with you for the entire year. You must also pay more than half the household expenses. This status offers the same tax rates and standard deduction as Married Filing Jointly - $31,500 for 2025 - providing some financial relief during a challenging time.

Here's a quick summary of the key details for each filing status:

| Filing Status | Marital Status Requirement (as of Dec 31) | Household/Dependent Requirement | 2025 Standard Deduction |

|---|---|---|---|

| Single | Unmarried, divorced, or legally separated | None | $15,750 |

| Married Filing Jointly | Legally married | None | $31,500 |

| Married Filing Separately | Legally married | None | $15,750 |

| Head of Household | Unmarried or "considered unmarried" | Paid >50% of home costs; qualifying dependent lived >6 months | $23,250 |

| Qualifying Surviving Spouse | Widowed within last 2 years; not remarried | Must have a dependent child | $31,500 |

Choosing the right filing status is a critical step in managing your tax situation effectively. It can help you take advantage of deductions and credits while minimizing your overall tax burden.

How Filing Status Affects Standard Deductions and Tax Brackets

Your filing status doesn't just categorize you - it directly impacts how much of your income is taxed and at what rates. It determines your standard deduction and sets the income thresholds for each tax bracket. These factors combined can significantly influence your overall tax bill. In short, understanding how filing status works can lead to considerable tax savings.

The U.S. operates under a progressive tax system, meaning your income is divided into portions, each taxed at different rates ranging from 10% to 37%. Your filing status determines where these brackets start and end. For instance, Single filers hit the 12% tax rate at income up to $48,475, but for those Married Filing Jointly, that same rate extends to $96,950 - essentially doubling the threshold.

"When your income jumps to a higher tax bracket, you don't pay the higher rate on your entire income. You pay the higher rate only on the part that's in the new tax bracket." - Internal Revenue Service [8]

This means that even if you move into a higher bracket, only the income exceeding the threshold is taxed at the new rate. For example, a Single filer with $100,000 in taxable income would owe about $16,913 in taxes. That’s an effective tax rate of 16.9%, which is much lower than the 24% bracket they’ve reached [9].

2025 Tax Brackets and Deductions by Filing Status

The table below highlights how standard deductions and tax brackets differ depending on your filing status. Notably, Head of Household filers enjoy both a higher standard deduction ($23,625) and wider lower-income brackets compared to Single filers. Meanwhile, Married Filing Jointly offers the largest standard deduction at $31,500.

| Tax Rate | Single Filers | Married Filing Jointly | Head of Household | Married Filing Separately |

|---|---|---|---|---|

| Standard Deduction | $15,750 | $31,500 | $23,625 | $15,750 |

| 10% | $0 – $11,925 | $0 – $23,850 | $0 – $17,000 | $0 – $11,925 |

| 12% | $11,926 – $48,475 | $23,851 – $96,950 | $17,001 – $64,850 | $11,926 – $48,475 |

| 22% | $48,476 – $103,350 | $96,951 – $206,700 | $64,851 – $103,350 | $48,476 – $103,350 |

| 24% | $103,351 – $197,300 | $206,701 – $394,600 | $103,351 – $197,300 | $103,351 – $197,300 |

| 37% | Over $626,350 | Over $751,600 | Over $626,350 | Over $626,350 |

If you qualify for more than one filing status - like Head of Household versus Single - it’s worth comparing how each affects your tax liability. A higher standard deduction and better tax brackets could save you a substantial amount. Since nearly 88% of taxpayers opt for the standard deduction instead of itemizing, choosing the right filing status is crucial for most Americans [7].

How Filing Status Affects Your Deductions, Credits, and Tax Bill

Your filing status plays a big role in determining which credits and deductions you can claim, directly impacting how much tax you owe. Here's a closer look at how different filing statuses influence your eligibility for key tax benefits and overall tax liability.

If you choose Married Filing Separately, you'll lose access to the Earned Income Tax Credit (EITC), education credits like the American Opportunity and Lifetime Learning credits, and the Premium Tax Credit. On top of that, your capital loss deduction is capped at $1,500, and if your spouse itemizes deductions, you're required to do the same.

On the other hand, Married Filing Jointly gives you access to the full range of benefits, including the EITC, Child Tax Credit, education credits, and deductions for student loan interest. It also offers the largest standard deduction - $31,500 for 2025. However, both spouses are equally responsible for any taxes or penalties owed.

Filing as Head of Household comes with a higher standard deduction ($23,625 for 2025) and lower tax rates compared to Single filers. You can also qualify for the EITC and Child Tax Credit, provided you pay more than half of your household expenses and have a qualifying dependent.

Benefits and Limitations of Each Filing Status

| Filing Status | Key Benefits | Major Limitations |

|---|---|---|

| Married Filing Jointly | Largest standard deduction ($31,500); full access to EITC, Child Tax Credit, education credits; can deduct up to $3,000 in capital losses. | Both spouses are jointly liable for taxes and penalties; may face a "marriage penalty" at higher income levels. |

| Head of Household | Higher standard deduction ($23,625) than Single; lower tax rates; eligible for EITC and Child Tax Credit. | Must pay over 50% of household costs and have a qualifying dependent. |

| Single | Straightforward filing process with individual liability. | Lowest standard deduction ($15,750) and narrower tax brackets. |

| Married Filing Separately | Individual liability; can help with income-driven student loan repayment. | Ineligible for EITC, education credits, and Premium Tax Credit; lower capital loss deduction ($1,500); must itemize if spouse itemizes. |

| Qualifying Widow(er) | Can use Married Filing Jointly tax rates and standard deduction ($31,500) for two years after a spouse's death. | Only available for two years and requires a qualifying dependent. |

"Married Filing Separately may be beneficial if one spouse has significant medical expenses, miscellaneous deductions, or if you want to keep finances separate for legal reasons."

- Jacob Dayan, CEO, Community Tax, LLC

Carefully evaluate your situation to weigh the pros and cons of each filing status. Running the numbers for each option can help you pinpoint the choice that minimizes your tax liability.

How to Determine Your Correct Filing Status

Figuring out your filing status can seem tricky, but the IRS provides clear guidelines to help you stay compliant and potentially reduce your tax bill.

Step 1: Understand Your Marital and Household Situation

Your marital status as of December 31 dictates your filing status for the entire tax year. For example, if you marry or divorce on that date, you're considered married or single for the whole year [4].

Next, look at your household expenses. To claim certain statuses, like Head of Household, you must cover more than 50% of your home's costs, including rent or mortgage payments, property taxes, utilities, repairs, food, and other expenses [4]. Additionally, a qualifying child or relative must live with you for more than half the year. However, there’s an exception if you support a dependent parent who lives elsewhere [4].

If living apart from your spouse, remember that separation alone isn’t enough. A finalized divorce decree or separate maintenance agreement must be in place by December 31 to file as single or Head of Household [4].

Once you've reviewed your situation, move on to the next step to confirm eligibility.

Step 2: Verify Eligibility with IRS Guidelines

Now, compare your situation to the IRS's eligibility requirements. An easy way to do this is by using the IRS Interactive Tax Assistant (ITA) tool. It only takes a few minutes to confirm which filing statuses you qualify for [1].

For example, if your spouse passed away in 2023 or 2024 and you have a dependent child, you might qualify as a Qualifying Surviving Spouse. This status allows you to benefit from joint-filing tax rates and a $31,500 standard deduction for up to two years [4].

Step 3: Evaluate Tax Outcomes for Each Status

Once you know your eligible statuses, compare how each one affects your tax liability. If you qualify for more than one, choose the one that results in the lowest tax bill [1].

"It is highly recommended that spouses compute their tax liability under both 'joint' and 'separate' statuses to see which will work best for them." - Jacob Dayan, CEO of Community Tax, LLC [11]

For example, a taxpayer earning $75,000 with one dependent could save about $2,200 annually by filing as Head of Household instead of Single [6]. Similarly, someone making $100,000 might pay around $17,400 in federal taxes as a Single filer but only $15,600 if filing as Head of Household [6].

Keep detailed records of household expenses - like rent, utilities, and groceries - to prove you covered more than half the costs if claiming Head of Household. Also, remember that filing as Married Filing Separately may disqualify you from certain credits (like the Earned Income Tax Credit) or deductions (like student loan interest) [11].

Using Deductible.me to Simplify Your Tax Filing

Once you’ve set your filing status, the next step is managing your deductions. Deductible.me makes this process easier by organizing your charitable donations and showing how they align with your selected status.

Track Your Charitable Donations

Keeping tabs on your donations throughout the year ensures you don’t miss any deductible expenses. Deductible.me uses AI photo scanning to log and assess the value of donated items as you give them. This means no more scrambling to piece together your donation history at tax time. The platform also tracks whether your total itemized expenses - such as donations, mortgage interest, and medical costs - exceed the standard deduction threshold for your filing status in 2025 [12].

Here’s why this is crucial: charitable contributions only lower your tax bill if you itemize. If your total itemized deductions, including donations, don’t surpass the standard deduction for your filing status, tracking them won’t result in savings [12]. Deductible.me keeps you updated throughout the year, helping you determine if itemizing is worth it. This way, donation tracking becomes part of your overall tax planning.

Create IRS-Compliant Reports

Deductible.me simplifies compliance by generating Form 8283-ready reports for noncash charitable contributions exceeding $500 [12]. It organizes your donation records to meet IRS standards, eliminating the hassle of manually compiling receipts and valuations.

For married couples filing separately, the platform handles a key rule: if one spouse itemizes deductions, the other must also itemize and cannot take the standard deduction [4][10]. Deductible.me tracks this coordination, helping you avoid filing mistakes that could draw IRS attention.

Reduce Your Tax Bill with AI-Powered Tools

With accurate records in place, Deductible.me’s AI-powered analytics fine-tune your tax strategy. These tools analyze how your filing status affects your overall tax liability. For instance, if one spouse has significant charitable donations, the platform helps you compare the tax implications of filing jointly versus separately.

Here’s an example: a taxpayer earning $75,000 who qualifies for head of household status instead of single can save about $2,200 annually [6]. Deductible.me’s valuation tools also ensure you claim the full fair market value of donated items, helping you avoid leaving money on the table by undervaluing your contributions.

Conclusion

Your filing status plays a critical role in shaping your tax obligations. The IRS evaluates your status as of December 31 to determine key factors like your standard deduction, tax brackets, and eligibility for various credits for the entire year [2][3]. Selecting the wrong status can lead to penalties, while the right choice could save you thousands [5].

"Your federal filing status plays a huge role in determining your tax bracket, the deductions and credits you qualify for, and even your tax liability at the end of the process."

- Jacob Dayan, CEO of Community Tax [4]

For 2025, choosing Head of Household status offers a higher standard deduction compared to filing as Single [6]. Married couples filing jointly often benefit from the largest standard deduction and access to exclusive credits, unlike those filing separately [6]. If you qualify for more than one status, the IRS allows you to choose the one that minimizes your tax liability [4]. This flexibility underscores the importance of selecting the most advantageous option for your circumstances.

Major life changes - such as marriage, divorce, the birth of a child, or the death of a spouse - should prompt a reassessment of your filing status. These events can significantly impact your deductions, credits, and overall tax bill. Running the numbers for each eligible status is a smart move, and the IRS Interactive Tax Assistant can help confirm your choice in just a few minutes, potentially saving you from costly mistakes [1][2][3].

Once your filing status is determined, Deductible.me can help you maximize its benefits. The platform ensures your deductions are aligned with your status, tracks whether itemizing exceeds your standard deduction, and generates IRS-compliant reports. When every dollar matters, combining the right filing status with precise donation tracking can help you keep more of your hard-earned money.

FAQs

Can I change my filing status after I file?

Yes, you can change your filing status after submitting your tax return, but it requires filing an amended return using Form 1040-X. You’ll need to do this within three years of filing your original return or two years from the date you paid the tax - whichever comes later. Your filing status is determined by your marital status as of December 31, and any changes in your situation may affect how you file.

What counts as “paying more than half” of household costs?

Paying more than half of household costs means shouldering over 50% of the essential expenses required to keep a household running. These expenses typically include rent or mortgage payments, utilities like electricity and water, and property taxes.

When does Married Filing Separately make sense?

When choosing the Married Filing Separately status, it might make sense if you prefer to be responsible solely for your own tax liability. This option can also be useful in cases involving complex financial situations or concerns about potential liabilities tied to your spouse's taxes.

However, keep in mind that this filing status often comes with limitations. It can reduce or completely eliminate eligibility for certain tax deductions and credits compared to filing jointly. It's important to carefully evaluate how this choice impacts your overall tax situation before making a decision.