How Overvalued Donations Trigger IRS Audits

Overvaluing charitable donations on your tax return can lead to audits, denied deductions, and steep penalties. The IRS uses advanced algorithms to flag discrepancies, especially when donation values seem inflated or lack proper documentation. For instance, claiming a $200 deduction for a thrift store sweater worth $50 could raise red flags. Here’s what you need to know:

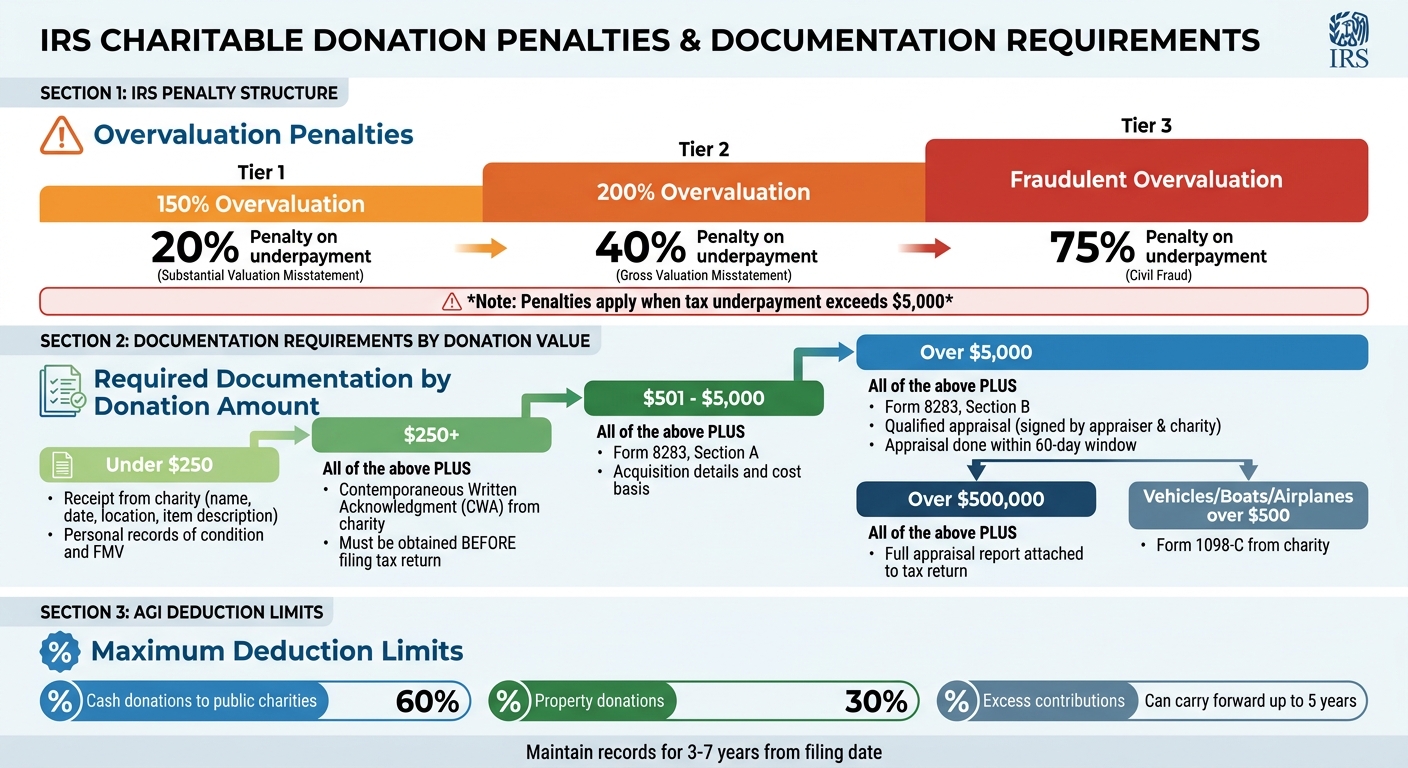

- Penalties: Overstating a donation’s value by 150% can result in a 20% penalty. At 200%, the penalty increases to 40%.

- Common Mistakes: Failing to submit required forms (like Form 8283 for noncash donations over $500) or skipping a qualified appraisal for items over $5,000.

- Documentation Rules: Donations over $250 require a written acknowledgment from the charity, while higher-value items need appraisals and additional forms.

- IRS Red Flags: Round-number estimates, disproportionate deductions, and unsupported claims often trigger audits.

Accurate valuations and thorough record-keeping are key to avoiding penalties and securing your rightful deductions.

IRS Penalties and Documentation Requirements for Charitable Donations

The Donation Write off IRS is Denying

sbb-itb-e723420

How the IRS Detects Overvalued Donations

The IRS relies on automated systems and data analytics to identify discrepancies in reported donations. These systems issue automated notices (labeled with a "CP" prefix) when your claimed donations don't align with the data the IRS already has, such as W-2s and 1099s [7]. If a mismatch is spotted, the system initiates a "desk audit", which requests additional documentation to verify the claims [7]. Here's how these checks work in more detail.

IRS Algorithms and Statistical Comparisons

The IRS uses algorithms to flag unusual donation patterns. For instance, claiming a $15,000 deduction on a $60,000 income is likely to stand out. These systems also cross-check payroll data with tax filings to identify inconsistencies [2][9]. For high-value items, the IRS may enlist internal appraisers or consult the Commissioner's Art Advisory Panel [1].

"IRS systems are being used to compare payroll data with other filings. Mismatches trigger follow-up." - Kim Wylam, Managing Principal, Baker Tilly [9]

These statistical methods help the IRS focus on returns that show clear signs of irregularities.

Red Flags That Trigger IRS Scrutiny

Certain donation behaviors are more likely to attract IRS attention. One major red flag is disproportionate value-to-cost ratios - like purchasing an item for $5,000 but claiming a $50,000 deduction [2]. Another is reporting round number estimates, such as claiming exactly $100 or $200 for donated clothing, which suggests you may not have itemized your donations [3]. Failing to include Form 8283 for noncash donations over $500 or neglecting to provide a qualified appraisal for items over $5,000 can also lead to denied deductions [2][1].

"Any larger-than-average deduction is going to arouse suspicion, but charitable contributions are a common red flag." - Anaheim Income Tax [7]

The IRS also scrutinizes promoter-led schemes, where third parties promise inflated donation values - often involving art, conservation easements, or closely-held business interests [8][2]. Appraisals that lack details about an item's rarity, age, or condition, especially when arranged by promoters, are another area of concern [8].

Common Valuation Mistakes That Cause Audits

Donors often make errors that catch the attention of the IRS, leading to audits. Being aware of these missteps can help you avoid unnecessary penalties and scrutiny.

Skipping Required Professional Appraisals

For noncash donations exceeding $5,000, the IRS mandates a qualified appraisal. This applies whether it’s a single item or a group of similar items donated throughout the year [10][11]. A common mistake involves aggregating similar items - like books, jewelry, or furniture - donated to different charities. For example, if you donate book collections to separate organizations and their combined value exceeds $5,000, a qualified appraisal is still required [11].

"The most common mistake donors make is treating the appraisal as an afterthought - something to sort out after the donation has already been made." - Legacy Donation Appraisers [10]

Timing is just as critical. Appraisals must be completed within a specific 60-day window: no earlier than 60 days before the donation and no later than the tax return due date [10][11]. Missing this deadline can result in your deduction being entirely disallowed.

Even if the appraisal is done correctly, errors in reporting can still invite IRS scrutiny.

Errors in Reporting Noncash Donations

For noncash donations over $500, Form 8283 is required. Mistakes on this form - like failing to report the cost or basis - can result in the IRS rejecting your deduction outright [11].

Another frequent issue involves the related-use rule. If you donate a painting to an art museum where it’s displayed (a related use), you can deduct its full fair market value. However, if the same painting is donated to a hospital for a fundraising auction (an unrelated use), your deduction is limited to your original cost basis. One donor, David, faced this issue when his $50,000 painting (with a cost basis of $10,000) would have only qualified for a $10,000 deduction if donated for an unrelated use [11].

On top of these mistakes, exceeding allowable deduction limits can make matters worse.

Claiming Deductions Above AGI Limits

The IRS enforces strict penalties for valuation errors. If your valuation misstatement exceeds 150% of the actual value, you face a 20% penalty on underpaid taxes. If it’s 200% or more, the penalty jumps to 40%, and reasonable cause defenses are typically not accepted [11][13].

"The IRS can and will disallow your entire charitable deduction, no matter how generous your gift... It does not matter if you made a small mistake or if your gift was genuine; the rules are strict." - TaxShark Inc [11]

The statute of limitations can also work against you. Normally, the IRS has three years to audit, but this only begins once your donation is properly documented. If your records are vague or incomplete, the IRS can challenge your valuation indefinitely [6][12].

IRS Documentation Rules and Audit Triggers

The IRS has specific guidelines for the paperwork required to substantiate charitable donations. Failing to meet these rules - even if your valuation is correct - can quickly trigger an IRS audit.

Required Documentation by Donation Amount

The type of documentation you need depends on the value of your donation. For contributions under $250, you’ll need a receipt from the charity that includes the organization's name, the date and location of the donation, and a detailed description of the items. Additionally, you should maintain personal records that note the condition and fair market value of the donated items [15].

For donations above $250, the requirements become more stringent. You must have a "contemporaneous written acknowledgment" (CWA) from the charity. This acknowledgment needs to confirm whether you received any goods or services in return for your donation and provide an estimate of their value. Importantly, this document must be obtained before you file your tax return - getting it afterward won’t satisfy IRS requirements [15][16][17].

"The IRS has gotten much stricter about these rules, sometimes denying deductions just because a receipt was missing a key piece of information." - DeductAble [15]

For noncash donations valued between $501 and $5,000, you’ll need the CWA along with Form 8283, Section A. This form requires details on how you acquired the property, the date of acquisition, and your cost basis. For donations over $5,000, you must complete Form 8283, Section B, and include a qualified appraisal signed by both the appraiser and the charity. Donations exceeding $500,000 require the full appraisal report to be attached to your tax return [14][15][17][18].

If you’re donating vehicles, boats, or airplanes worth more than $500, you’ll need Form 1098-C from the charity. In most cases, your deduction will be limited to the gross proceeds from the charity’s sale of the vehicle, rather than its fair market value [16][18].

Failing to provide the necessary documentation can lead to the IRS denying your deduction or subjecting your return to additional scrutiny.

How Missing Records Lead to Audits

Incomplete records don’t just raise red flags - they can outright disqualify your deduction. For donations of $250 or more, the law requires a contemporaneous written acknowledgment. Without it, your deduction is invalid, and even obtaining proof after filing won’t reverse the denial [16].

The IRS also uses Form 8282 to verify the accuracy of your claimed deductions. If a charity sells or disposes of donated property valued over $500 within three years, they must file this form within 125 days and send you a copy [14]. If the sale price reported by the charity significantly differs from the value you claimed, the IRS may investigate further.

Keeping thorough and accurate records not only supports your claimed deductions but also helps protect you from audit penalties tied to overvalued donations.

What Happens When the IRS Finds Overvaluation

Overstating the value of donations can lead to the IRS recalculating your tax liability and imposing hefty penalties.

Denied Deductions and Financial Penalties

The IRS enforces accuracy-related penalties depending on the degree of overvaluation. If the claimed value is overstated by 150% or more and results in a tax underpayment exceeding $5,000, a 20% penalty - called a "substantial valuation misstatement" - is applied. For overstatements of 200% or more, the penalty jumps to 40%, known as a "gross valuation misstatement." In cases of fraudulent overvaluation, the penalty can reach a staggering 75% of the underpayment [19].

"If the IRS finds that the value or basis of the property was overstated by 150% or more, and the underpayment of tax exceeds $5,000, a 20% penalty may apply; if overstated by 200% or more, the penalty increases to 40%." – Alana Mueller, Partner, Bennett Thrasher

A striking example is the case of Reri Holdings I, LLC v. Commissioner (2017), where the U.S. Tax Court denied a $33 million charitable deduction after finding the actual value to be just $3 million. This led to a 40% gross overvaluation penalty, along with interest on the underpayment and an additional monthly penalty of 0.5%, capped at 25% of the total [19].

| Misstatement Type | Claimed vs. Actual Value | Penalty Rate |

|---|---|---|

| Substantial Valuation Misstatement | 150% or more | 20% of underpayment |

| Gross Valuation Misstatement | 200% or more | 40% of underpayment |

| Civil Fraud | Intentional deception | 75% of underpayment |

These financial penalties are no small matter, and repeated overvaluation can lead to even more serious consequences.

Legal Consequences for Repeated Violations

Beyond monetary penalties, systematic or intentional overvaluation can attract criminal charges. The IRS views repeated overvaluation as a form of tax evasion, which could lead to fines and even imprisonment. For instance, in United States v. Michael Meyer, the IRS pursued criminal tax evasion charges after uncovering a deliberate scheme to inflate donation values.

"Participating in an illegal scheme to avoid paying taxes can result in repayments of the taxes owed with penalties and interest and potentially even fines and imprisonment." – IRS.gov

When fraud or deliberate misrepresentation is involved, the IRS can audit and challenge deductions indefinitely, as there is no statute of limitations. Professional appraisers who overvalue property also face penalties under IRC 6695A. This can include the lesser of either $1,000 or 10% of the underpayment, or 125% of the fee earned for the appraisal. Additionally, appraisers may be referred to the Office of Professional Responsibility, risking the loss of their ability to practice before the IRS [19].

Ensuring accurate valuations and proper documentation not only protects your deductions but also keeps you clear of escalating penalties and potential legal trouble.

How to Value Donations Accurately and Avoid Audits

Accurate and verifiable assessments of donated items are key to avoiding overvaluation risks. The IRS defines Fair Market Value (FMV) as the price a willing buyer would pay a willing seller in an open market, where both parties are informed about the item's condition. Following this definition and maintaining detailed records can significantly reduce your chances of an audit.

Use AI-Powered Valuation Tools

Technology can make valuing your donations much easier. Deductible.me is an app that uses AI to analyze photos of your donated items, assigning values that comply with IRS standards based on their condition and category. It also generates IRS-compliant reports, offering a simple and affordable way to track donations throughout the year.

If you don’t have access to such tools, you can rely on a manual method. Start by identifying the item's category, evaluating its condition, and assigning a reasonable value - ideally on the lower to mid-range of established market values. When setting a value, prioritize data from completed sales on platforms like eBay rather than relying on active listings.

Keep Complete Records of All Donations

Documenting your donations thoroughly is essential. Take clear photos of each item to establish proof of its condition and existence. Store these photos along with receipts and detailed donation logs in digital form, ensuring they are retained for the required 3–7 years [15][20].

With these records in place, you can confidently claim deductions that reflect realistic and supportable market values.

Claim Deductions Within Reasonable Limits

Keeping your claims within IRS guidelines is another way to avoid triggering reviews. For instance, cash donations to public charities are generally capped at 60% of your Adjusted Gross Income (AGI), while property donations are limited to 30% [5]. If your contributions exceed these limits, you can carry the excess forward for up to five years.

If your total deductions are close to the standard deduction threshold, consider a bunching strategy. This involves consolidating two years’ worth of donations into one, allowing you to exceed the threshold and maximize your tax benefits. Always confirm that your chosen charity is a qualified 501(c)(3) organization using the IRS Tax Exempt Organization Search tool before claiming any deductions [3]. Taking a cautious and realistic approach to valuation ensures your claims remain defensible and keeps you well within IRS guidelines.

Conclusion

Overestimating the value of charitable donations can lead to serious consequences, including IRS audits, denied deductions, and penalties that may reach up to 40% of the underpaid tax in severe cases [13]. It's crucial to remember that the responsibility for determining a fair market value lies with you - not the charity. This makes proper documentation and realistic valuations absolutely essential [4][15].

Thankfully, avoiding these risks is manageable with careful planning and accurate record-keeping. Tools like Deductible.me simplify the process by providing IRS-compliant valuations for donated items based on their condition and category. This app also allows you to capture photos, store digital receipts, and create reports ready for Form 8283, removing the guesswork and reducing the risk of manual errors [15][20]. Digital solutions like these ensure you're prepared for an audit at any time.

"The core principle is simple: An accurate valuation ensures you get the full tax benefit you're entitled to, while solid documentation provides the proof the IRS requires." - DeductAble [4]

With Americans donating a staggering $392.45 billion in 2024 alone [15], the importance of accurate reporting has never been greater. A cautious, well-documented approach ensures you avoid penalties while claiming every deduction you're entitled to. Using the right tools helps you maintain thorough, defensible records - records that must be kept for three to seven years from your filing date [4][15]. Proper documentation not only minimizes audit risks but also ensures you maximize your tax benefits.

FAQs

How does the IRS decide a donation value is too high?

When it comes to donations, the IRS keeps a close eye on valuations. If you claim a donation's value is higher than its fair market value (FMV) - essentially, the price it would fetch in a deal between knowledgeable buyers and sellers - it could raise red flags. This is especially true if there’s no proper documentation or a qualified appraisal to back up the claim. To stay compliant, make sure your valuations match the FMV and meet the IRS's substantiation rules.

What proof do I need for noncash donations if I’m audited?

To steer clear of IRS scrutiny, it’s crucial to have the right documentation for your noncash donations. The requirements vary based on the donation’s value:

- Under $250: Keep a bank record or an acknowledgment from the charity.

- $250–$500: Obtain a written acknowledgment that details the donation.

- $501–$5,000: Complete Form 8283. For donations exceeding $5,000, you’ll also need a qualified appraisal.

Make sure to organize all relevant documents - like receipts, acknowledgment letters, photos, and appraisals - to back up your claims and stay compliant with IRS regulations.

How can I estimate fair market value for donated items without overclaiming?

To determine the fair market value (FMV) accurately, think about what a willing buyer and seller would agree upon in an open market, factoring in the item's condition. One practical way to estimate this is by comparing prices of similar items at thrift stores or online marketplaces. For items valued over $5,000, a professional appraisal is typically necessary. Keeping detailed records - such as receipts and photographs - not only helps establish the value but also ensures compliance and minimizes the risk of IRS scrutiny.