Form 8283: Common Errors to Avoid

Filing Form 8283 is essential if you’re claiming deductions for non-cash donations over $500. Mistakes on this form can lead to denied deductions or penalties. Here’s what you need to know:

- Section A: For items valued between $500–$5,000 (or exceptions like publicly traded securities).

- Section B: For items or groups exceeding $5,000, requiring a qualified appraisal and signatures.

- Key Errors to Avoid:

- Missing cost basis or acquisition details.

- Overstating fair market value without proper appraisals.

- Missing appraiser and charity signatures.

- Vague item descriptions or incorrect grouping.

- Failing to secure written acknowledgments for donations over $250.

Accurate records are critical. Attach appraisals, organize receipts, and ensure all fields are complete. Tools like Deductible.me can simplify compliance by automating valuations, tracking thresholds, and ensuring proper documentation.

Top 10 Questions, Myths, and Mysteries About IRS Form 8283 and 8282

sbb-itb-e723420

Common Errors When Completing Form 8283

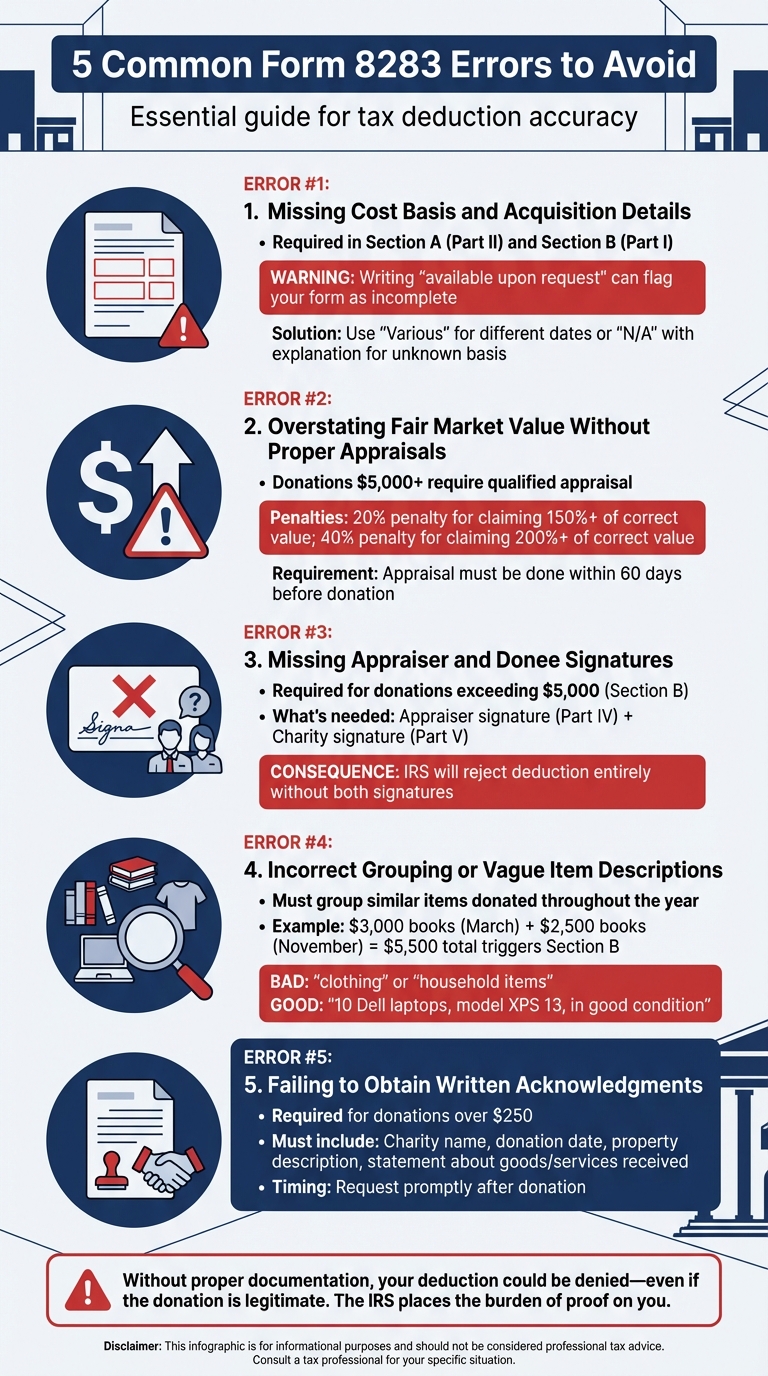

5 Common Form 8283 Errors to Avoid When Filing Non-Cash Donation Deductions

Even small mistakes on Form 8283 can lead to IRS scrutiny or the outright denial of your deduction. Knowing the common pitfalls can save you time, frustration, and money when tax season rolls around. Let’s break down the most frequent errors and how to steer clear of them.

Missing Cost Basis and Acquisition Details

One common misstep is failing to include the cost or adjusted basis of the donated property. This information, required in Section A (Part II) and Section B (Part I), helps the IRS determine whether your deduction is limited to the lower of the fair market value or your original cost.

Leaving these fields blank - or worse, writing "available upon request" - can cause your form to be flagged as incomplete or non-responsive. The IRS explicitly warns against such practices, stating that incomplete forms may lead to disallowed deductions [1]. If you’ve donated items acquired on different dates, use "Various" in the date acquired column. For inherited or older items where the basis is unknown, write "N/A" and attach a statement explaining why the basis isn’t available.

Failing to provide this information can jeopardize your deduction, no matter how legitimate or substantial the donation.

Overstating Fair Market Value Without Proper Appraisals

Fair market value reflects what a buyer and seller would agree upon under normal conditions, with all relevant facts considered. Overestimating this value - especially without a valid appraisal - can lead to penalties.

For donations of $5,000 or more (whether a single item or a group of similar items), a qualified appraisal is required. This appraisal must be completed no more than 60 days before the donation date and no later than your tax filing deadline (including extensions). It must also adhere to Uniform Standards of Professional Appraisal Practice (USPAP) and rely on recognized valuation methods, such as comparable sales [7].

The IRS imposes steep penalties for overvaluation. Claiming 150% or more of the correct value can result in a 20% penalty on underpaid taxes, while claiming 200% or more can lead to a 40% penalty - with no defense for "reasonable cause" [5]. Ensuring all required signatures are included with the appraisal further solidifies its validity.

Missing Appraiser and Donee Signatures

For donations exceeding $5,000 (reported in Section B), two signatures are critical: one from the qualified appraiser (Part IV) and one from the receiving charity (Part V). Without these, the IRS will reject your deduction entirely.

The appraiser’s signature certifies the appraisal’s accuracy and their independence from you, the charity, and the transaction. Meanwhile, the donee’s signature confirms receipt of the property and whether any goods or services were exchanged [4] [6]. Both signatures are essential for verifying your claimed values and complying with IRS rules.

To avoid delays, secure these signatures as soon as possible. Before donating high-value items, confirm that the charity is willing to sign Form 8283. Also, ensure your appraiser holds credentials from established organizations like the American Society of Appraisers (ASA), Appraisers Association of America (AAA), or International Society of Appraisers (ISA) [5].

Incorrect Grouping or Vague Item Descriptions

The IRS requires you to group "similar items" donated throughout the year, even if they were given to different charities. For instance, if you donated $3,000 worth of books in March and $2,500 worth in November, the combined $5,500 total triggers Section B requirements, including the need for a qualified appraisal. Proper grouping ensures accurate recordkeeping and compliance.

Avoid general descriptions like "clothing" or "household items", which won’t satisfy IRS standards. Instead, provide detailed descriptions such as "10 Dell laptops, model XPS 13, in good condition" or "Oak dining table with six chairs, circa 1990, in excellent condition." Include specifics like quantity, brand, model, age, and condition for each item or group. This level of detail strengthens your deduction and prepares you for any potential audit.

Failing to Obtain Written Acknowledgments

For donations over $250, the IRS requires a written acknowledgment from the charity. This document must confirm that no goods or services were received in exchange for your gift. While separate from Form 8283, it’s just as vital for supporting your deduction.

The acknowledgment should include the charity’s name, the donation date, a description of the property, and a statement about whether anything was received in return. Request these acknowledgments promptly after making your donation to avoid complications later on.

The Importance of Recordkeeping and Documentation

Without proper records, your deduction could be denied - even if the donation itself is legitimate. The IRS places the burden of proof squarely on you. While the charity confirms receipt, it doesn’t verify the value you claim. In an audit, your documentation becomes your only line of defense. Keeping accurate records not only backs up your entries on Form 8283 but also ensures compliance with the IRS's valuation rules.

Tax court cases highlight how critical this is. For instance, in RERI Holdings I, LLC v. Commissioner, failing to include cost basis details led to a disallowed deduction. Similarly, in Mohamed v. Commissioner (T.C. Memo. 2012-152), taxpayers donated their home to their foundation and claimed $1.8 million. But because the appraisal was done after filing and Form 8283 was incomplete, the deduction was denied. The court made it clear:

"the substantiation requirements are not mere technicalities; they are a prerequisite for the deduction." - Tax Court, Mohamed v. Commissioner.

Below, we’ll cover common mistakes and provide practical tips to ensure your deductions hold up.

Common Documentation Errors

Accurate and thorough recordkeeping is essential to support your deduction. Missing receipts or acknowledgments are some of the most common pitfalls. For donations of $250 or more, you must secure a Contemporaneous Written Acknowledgment (CWA) from the charity before filing your return. Courts have rejected deductions entirely when this document was obtained after the filing deadline, even if the donation itself was valid.

Vague item descriptions are another issue. For high-value items, take clear, detailed photographs at the time of donation to document their condition.

Incomplete cost basis records can also raise red flags. If you inherited an item or bought it so long ago that the original cost is unknown, don’t leave the field blank. Instead, write "N/A" and include a written explanation. This small step can prevent the IRS from dismissing your deduction as incomplete.

Best Practices for Recordkeeping

To avoid these pitfalls, keep all donation-related documents in one place. This includes itemized lists, purchase receipts, appraisal reports, written acknowledgments, and photographs of donated items. Organize everything by donation date, and retain these records for at least three years after filing. Many experts suggest holding onto appraisals and acknowledgments for seven years to cover any potential audit window. Consistent organization reduces errors on Form 8283 and strengthens your position in case of an audit.

Act quickly to secure signatures. Get the donee's signature on Form 8283 at the time of the donation, while authorized personnel are available. For electronics, include proof that personal data was professionally wiped before donating. If you’re donating a vehicle, retain the Form 1098-C issued by the charity within 30 days. Records created at the time of donation carry far more weight than those assembled months later during tax season.

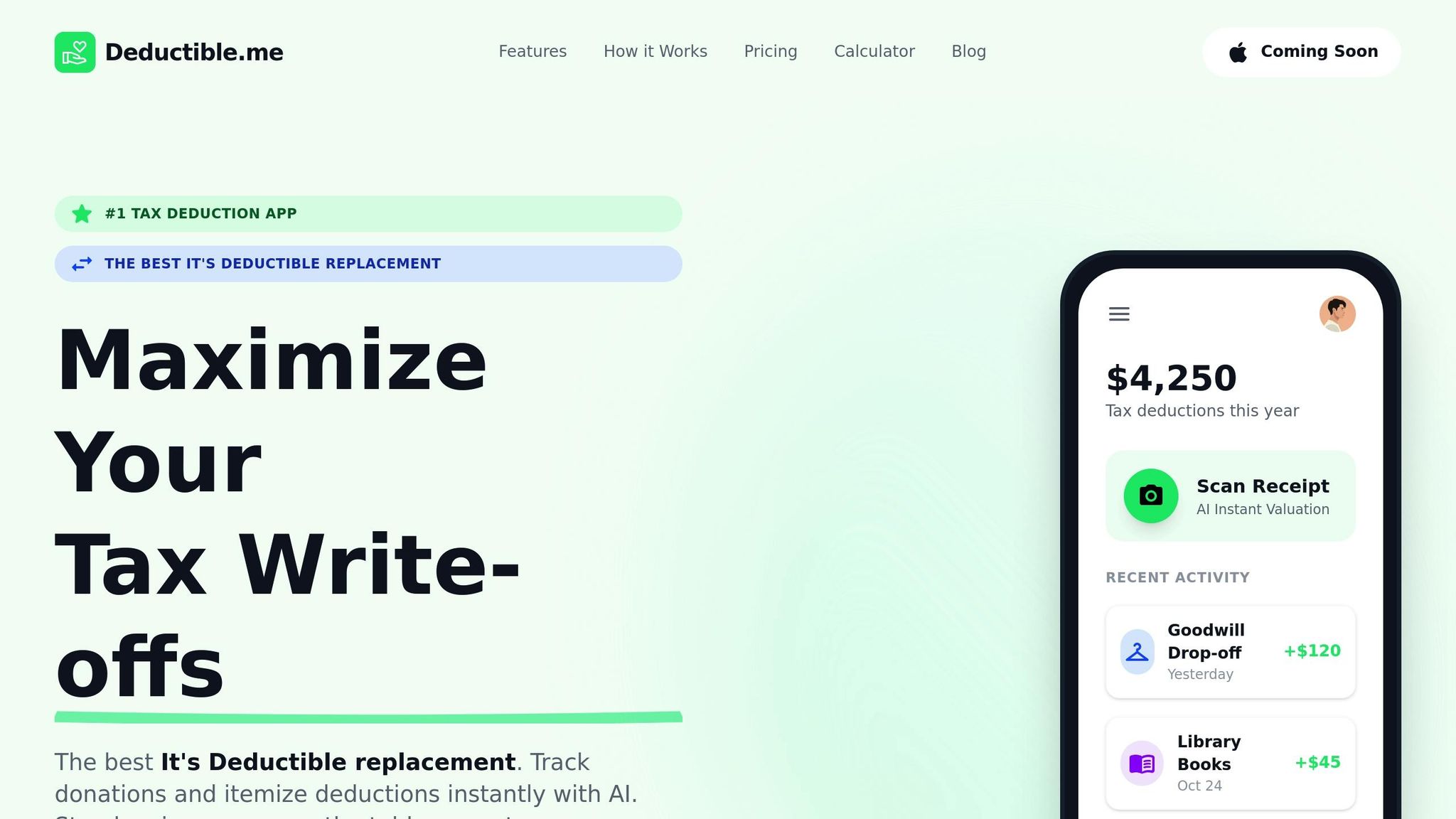

How Deductible.me Simplifies Form 8283 Compliance

Filling out Form 8283 can feel like navigating a maze. You need to provide accurate details like cost basis, acquisition dates, fair market values, signatures, and ensure you meet donation thresholds. Miss a single step, and you could lose your deduction entirely. That’s where Deductible.me steps in. By automating the complex calculations and documentation, this tool reduces the chances of costly mistakes that could draw unwanted attention from the IRS.

Key Features for Error Prevention

Deductible.me uses AI to calculate fair market values based on up-to-date market data. This eliminates the guesswork and avoids the common error of overestimating values, which can result in penalties of 20% to 40% if the IRS finds significant misstatements [5].

The app also tracks donation thresholds automatically. For instance, if your total non-cash donations exceed $500 in a year, you’ll get a notification that filing Form 8283 is required. It even groups similar items - like clothing or books - to alert you if your donations surpass the $5,000 mark, which would require a qualified appraisal. These features address frequent filing errors, like failing to get the necessary appraisal when it’s mandatory.

In addition, the tool records cost basis and acquisition details, ensuring these often-missed elements are properly documented. It securely stores acknowledgments and tracks required signatures, keeping you compliant with IRS rules.

For higher-value donations, such as vehicles or digital assets, Deductible.me offers tailored features like recording VINs or transaction hashes. You can even upload photos to document item conditions, which can be critical if the IRS questions your valuations. All this information is neatly organized by donation date, making it easy to access if an audit arises.

These features are available through flexible pricing plans, designed to accommodate a range of donation needs.

Premium vs. Free Plans

Deductible.me offers both free and premium plans to suit different types of donors. The Free plan is perfect for occasional donors with deductions under $500 annually. It includes AI photo scanning, basic receipt tracking, and IRS-compliant reports.

The Premium plan, priced at just $2 per month, is ideal for those donating over $500 in non-cash items annually or managing multiple donations. It removes all tracking limits and adds advanced features like Form 8283–ready reports, detailed receipt management, annual giving goal tracking, advanced analytics, and priority customer support.

| Feature | Free Plan | Premium Plan |

|---|---|---|

| Annual Donation Limit | Up to $500 | Unlimited |

| AI Photo Scanning & Valuation | ✓ | ✓ |

| IRS-Compliant Reports | ✓ | ✓ (Form 8283–Ready) |

| Advanced Receipt Management | - | ✓ |

| Annual Giving Goal Tracking | - | ✓ |

| Advanced Analytics | - | ✓ |

| Priority Support | - | ✓ |

| Price | $0/month | $2/month |

Considering that Americans donate around $46 billion in property to charities annually [5], and the IRS can reject deductions for incomplete forms, spending $24 per year on the Premium plan could save you hundreds - or even thousands - by avoiding denied deductions and penalties.

Conclusion

Filling out Form 8283 correctly is key to protecting your deductions from being denied by the IRS. Mistakes like omitting the cost basis, overestimating item values without proper appraisals, leaving out required signatures, or providing vague descriptions can lead to disallowed deductions. As TaxShark explains, "Filing mistakes or incomplete information are among the top reasons the Service denies deductions." [2]

The stakes are high - valuation penalties can climb up to 40% of any tax underpayment [2]. If your donation exceeds $5,000, you’ll need a qualified appraisal and signatures on Section B from both the appraiser and the donee organization [2]. Missing these steps could result in losing your deduction entirely.

Good recordkeeping is non-negotiable. Take clear photos of donated items, noting details like their condition, brand names, and model numbers. For donations of $250 or more, secure a written acknowledgment before filing your return [2]. To ensure the charity qualifies, use the IRS Tax Exempt Organization Search tool to confirm its 501(c)(3) status [3].

For those juggling multiple donations or contributions over $500 annually, tools like Deductible.me can make life easier. Its Premium plan, priced at just $2 per month, offers features like AI-powered valuations, automatic tracking of IRS thresholds, and ready-to-file Form 8283 reports - helping you stay compliant while maximizing deductions.

FAQs

When do I use Section A vs. Section B on Form 8283?

Form 8283 is designed to document noncash charitable contributions, but the section you use depends on the value of your donation.

- Section A: Reserved for noncash donations where the claimed deduction is more than $500 but does not exceed $5,000.

- Section B: Used for donations valued over $5,000. These often require a qualified appraisal to substantiate the deduction.

Make sure to choose the correct section based on the value of your donation to avoid any issues with your tax filing.

What counts as “similar items” for the $5,000 appraisal rule?

When donating two or more similar items, it's important to list each one separately on Form 8283. However, you can group them within a single appraisal report. Just make sure the report is divided into clear, distinct sections to keep everything organized.

What documents should I keep if I’m audited?

If you're ever audited, it's crucial to keep detailed documentation such as receipts, appraisals, and records of donated property. These documents should clearly outline descriptions, fair market value, and, when necessary, include appraiser signatures. Having accurate records ensures your claims align with IRS guidelines and helps avoid potential issues.