Charitable Receipt Requirements: IRS Guide

When it comes to charitable donations and tax deductions, the IRS has strict rules for documentation. To claim your deduction, you need specific records based on the donation type and value:

- For cash donations under $250, keep a bank record or a written statement from the charity.

- For donations of $250 or more, obtain a written acknowledgment from the charity, including details like the donation amount and whether you received anything in return.

- Noncash donations over $500 require Form 8283, Section A, and additional details about the item’s acquisition and value.

- Noncash donations over $5,000 must include a qualified appraisal and Form 8283, Section B.

Starting with 2025 tax filings, charitable deductions require itemizing on Schedule A. Non-itemizers can claim a limited above-the-line deduction for cash gifts, but stricter rules apply to donor-advised funds and private foundations. Missing documentation, such as receipts or appraisals, can result in denied deductions or penalties.

Proper recordkeeping is essential. Tools like Deductible.me can help you track and organize receipts, ensuring compliance with IRS rules. Always confirm the charity’s IRS status before donating, and document your contributions thoroughly to avoid issues.

IRS Charitable Donation Documentation Requirements by Amount

The Tax Documentation You Need for Charitable Donations

sbb-itb-e723420

IRS Documentation Rules by Donation Amount

The IRS sets specific documentation requirements based on the size of your donation to ensure your deductions are valid. Knowing these rules can help you keep the right records and maximize your deductions.

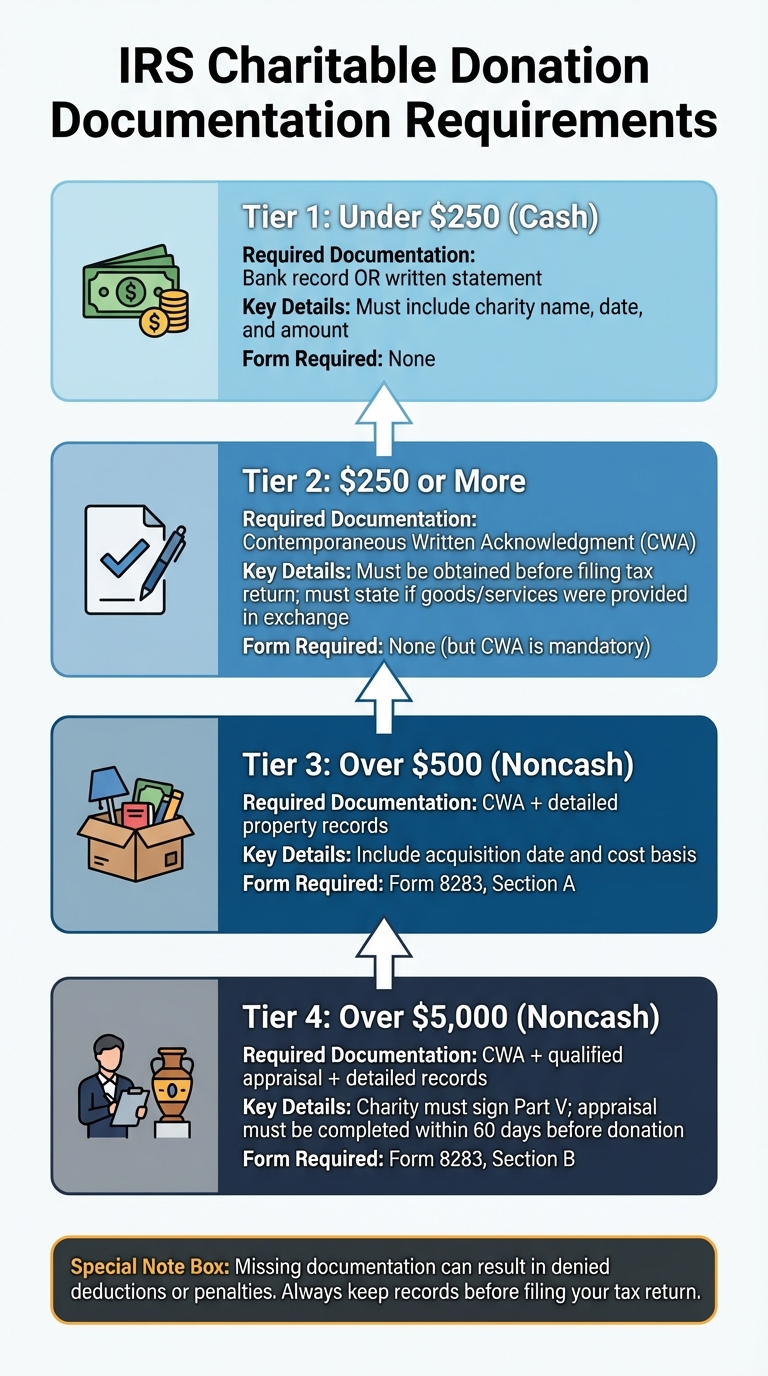

Donations Under $250

For cash donations under $250, you’ll need a bank record or a written statement from the charity that includes the charity's name, the donation date, and the amount [6].

If your donation was made through payroll deductions, keep your pay stub or Form W-2 showing the withheld amount, along with a pledge card or document that lists the charity's name [7]. For property donations under $250, you should get a receipt from the charity detailing its name, the date, location, and a description of the items donated. If you drop off items at an unattended location, create your own written record with details like the property description, its fair market value, and how you determined that value [3].

Important Notes:

- The IRS considers the credit card charge date as the donation date [6].

- Clothing and household items must be in at least good used condition to qualify for a deduction [7].

If your donation is $250 or more, additional documentation requirements apply.

Donations of $250 or More

For donations of $250 or more, you’ll need a contemporaneous written acknowledgment (CWA) from the charity. This acknowledgment must include the cash amount or a description of donated property (not the appraised value) and a statement indicating whether any goods or services were provided in return [7].

Make sure to obtain this acknowledgment by the earlier of your tax return filing date or its extended due date [8].

If the charity provided goods or services worth more than $75 in exchange for your donation, the acknowledgment must also include a description and an estimate of their value [7]. A single document from the charity can meet both the general recordkeeping and CWA requirements for donations of $250 or more [7].

Noncash Donations Over $500

Noncash donations exceeding $500 require additional steps. You must complete IRS Form 8283, Section A, and attach it to your tax return. This form includes detailed information about the donated property, such as when it was acquired and its cost basis [7].

You’ll also need the contemporaneous written acknowledgment required for donations of $250 or more and records showing the acquisition details and cost of the property [5].

Noncash Donations Over $5,000

If you donate noncash items valued over $5,000, the requirements increase further. You’ll need a qualified appraisal and must complete IRS Form 8283, Section B [7].

"For claimed contributions over $5,000, generally a qualified appraisal prepared by a qualified appraiser must be obtained." - Internal Revenue Service [7]

The charity must sign Part V of Section B on your Form 8283 to confirm receipt of the property. However, the charity’s signature only acknowledges receipt - it does not confirm the appraised value [5]. Keep in mind, publicly traded securities typically don’t require an appraisal, even if their value exceeds $5,000, and separate rules apply to vehicle donations [5].

| Donation Amount | Required Documentation | Key Details |

|---|---|---|

| Under $250 (cash) | Bank record or written statement | Must include charity name, date, and amount |

| $250 or more | Contemporaneous written acknowledgment | Must be obtained before filing your tax return |

| Over $500 (noncash) | Form 8283, Section A | Include acquisition date and cost basis |

| Over $5,000 (noncash) | Form 8283, Section B with appraisal | Requires charity's signature on the form |

Cash Contribution Documentation

When it comes to cash contributions, the documentation process is relatively straightforward compared to noncash donations. Cash gifts include payments made by check, credit card, electronic funds transfer (EFT), online services, and payroll deductions. Unlike noncash donations, such as clothing or furniture, which require valuation based on fair market value, cash contributions are documented differently.

Standard Documentation for Cash Gifts

To claim a deduction for a cash contribution, you need a bank record or a written statement from the charity. Acceptable forms of documentation include:

- Canceled checks

- Bank or credit card statements that show the charity's name, the date, and the donation amount

- Letters, receipts, or emails from the charity that include the charity's name, the contribution date, and the amount donated

As the IRS clearly states:

"A donor may not claim a deduction for any contribution of cash, a check, or other monetary gift... unless the donor maintains a record of the contribution in the form of either a bank record... or a written communication from the charity." – Internal Revenue Service

It's important to note that personal check registers and handwritten notes do not qualify as valid records. If you make a donation via text message, the deduction applies to the year the charge appears on your billing statement.

Payroll Deductions and Workplace Giving

For cash contributions made through payroll deductions, additional documentation is required. Specifically, you’ll need:

- A record from your employer, such as a pay stub or Form W-2

- A pledge card or document from the charity that includes the charity's name

For workplace giving campaigns, like the Combined Federal Campaign or United Way, the name of the local campaign can be used in place of the charity's name.

Each payroll deduction is considered a separate contribution when determining if it meets the $250 threshold for additional documentation. Make sure you gather all necessary records before filing your tax return or by its due date (including extensions). Following these steps ensures your cash contributions meet IRS requirements for tax deductions.

Noncash Property Donation Requirements

Donating noncash items like clothing, furniture, artwork, or vehicles comes with specific documentation rules. The fair market value (FMV) - what a willing buyer would pay a willing seller - plays a key role in meeting IRS requirements [11]. Once you determine FMV, you'll need to follow the appropriate filing steps.

If your total noncash contributions exceed $500, you must include Form 8283 when filing your tax return [10]. This form is divided into two parts: Section A is for items (or groups of similar items) valued between $501 and $5,000, while Section B is for items valued over $5,000 [11]. The IRS considers similar items collectively (e.g., books, paintings, or coins) to determine whether the $5,000 threshold applies [11].

Here’s a quick breakdown of the documentation and appraisal requirements based on the value of your donation:

| Deduction Amount | Required Documentation | Form 8283 Section | Appraisal Required? |

|---|---|---|---|

| $500 or less | Charity receipt | Not required | No |

| $501 – $5,000 | Charity receipt | Section A | No (unless item isn't in good condition) |

| Over $5,000 | Charity receipt + Appraisal | Section B | Yes (Qualified Appraisal) |

| Over $500,000 | Charity receipt + Appraisal | Section B | Yes (Attach full appraisal to return) |

Valuing and Recording Noncash Items

When donating noncash items, you’ll need to record the FMV, the method used to determine it, and the condition of the item [1]. For clothing and household items, the IRS generally requires them to be in "good used condition" or better to qualify for a deduction. If an item is not in good condition and the deduction exceeds $500, a qualified appraisal must be attached to your return [11].

Vehicle donations have specific rules. For cars, boats, or airplanes valued over $500, your deduction is typically limited to the gross proceeds the charity receives from selling the vehicle. These proceeds are reported on Form 1098-C [1][11]. This ensures donated vehicles are not overvalued.

Accurately documenting FMV and item condition is critical, especially when determining whether a qualified appraisal is needed.

When You Need a Qualified Appraisal

A qualified appraisal is mandatory for any single item or group of similar items valued at over $5,000 [1]. The appraisal must be completed, signed, and dated within 60 days before the donation [11]. For donations exceeding $500,000, the full appraisal must also be attached to your tax return along with Form 8283 [11].

The appraiser must have proper education and experience specific to the property type being valued and must adhere to IRS valuation guidelines [12]. For Section B items on Form 8283, both the appraiser and the charitable organization must sign the form. However, the charity’s signature only confirms receipt of the property - it does not endorse the appraised value [11][13]. If you’re donating art valued at $20,000 or more, additional requirements like providing a high-resolution photograph and a signed appraisal may apply [11].

Common Documentation Errors to Avoid

When it comes to tax deductions for donations, even small documentation mistakes can lead to big problems. If you’ve donated $250 or more, you’ll need a contemporaneous written acknowledgment by the time you file your taxes. Without it, you risk losing those deductions, no matter how well-intentioned your contributions were.

Missing or Incomplete Receipts

Your personal records won’t cut it. The IRS makes it clear: "written records prepared by the donor (such as check registers or personal notations) are no longer sufficient to support charitable contributions" [4]. For monetary donations, you’ll need either a bank record or a written acknowledgment from the charity. This acknowledgment must include:

- The date of the donation

- The amount donated

- The name of the organization [4]

Timing is everything. If you don’t have the acknowledgment by the time you file your tax return, your deduction could be denied [3][4]. The receipt also needs to state whether you received any goods or services in exchange for your donation. For example, if you got a dinner ticket or a tote bag, the receipt must include a good faith estimate of its fair market value. You can only deduct the portion of your donation that exceeds the value of those goods or services.

Omitting Required Appraisals

Proper valuation of noncash donations is just as important as having the right receipts. If your noncash contribution exceeds $5,000, you’re required to get a qualified appraisal and complete Form 8283, Section B [1][5]. Skipping this step can be costly - the IRS may hit you with a 20% penalty for substantial valuation misstatements or even a 40% penalty for gross valuation errors [1].

Form 8283, Section B, must include signatures from both a qualified appraiser and the charitable organization [1][5]. Keep in mind, the charity’s signature only confirms that they received the donation - it doesn’t mean they agree with your valuation. Without this documentation, your deduction will be denied.

Additionally, donated items must be in good used condition or better. If they aren’t, you’ll need a qualified appraisal to support your claim [1][4][7]. Taking photos of the items before donating can provide helpful evidence of their condition, which could save you from disputes down the road.

2026 Tax Law Changes for Charitable Deductions

The tax rules for charitable giving have undergone notable changes in 2026, introducing new limits on deductions and stricter documentation requirements.

New AGI Floor and Non-Itemizer Deduction Limits

For taxpayers who itemize, a new 0.5% Adjusted Gross Income (AGI) floor now applies to charitable deductions. This means the first 0.5% of your AGI in charitable contributions won't count toward your deduction. For instance, if your AGI is $200,000, the first $1,000 of your donations won't be deductible [14]. Megan Lencoski of Carnegie Investment Counsel explains:

"This 0.5% threshold functions like a floor. You must clear it before any of your donations count for a tax deduction" [15].

Non-itemizers, who make up about 87% of U.S. taxpayers, can now take an above-the-line deduction of up to $1,000 for individuals or $2,000 for married couples filing jointly. However, this only applies to cash contributions made directly to U.S. publicly supported charities. Noncash donations, such as clothing or furniture, are excluded if you opt for the standard deduction [14][15].

Additionally, taxpayers in the highest tax bracket now face a deduction cap of 35%, reducing the tax benefit to 35 cents per dollar donated. Meanwhile, the 60% AGI limit for cash contributions to public charities has been made permanent [14][15].

To maximize your deductions, consider "bunching" donations into a single tax year to surpass the 0.5% AGI floor. Be sure to retain documentation like bank statements, credit card receipts, and written acknowledgments to substantiate your claims. These changes also introduce new restrictions on contributions to donor-advised funds and private foundations.

Changes to Donor-Advised Funds and Private Foundations

The new above-the-line deduction for non-itemizers excludes contributions to donor-advised funds (DAFs) and most private foundations [14][17]. Only cash donations made directly to U.S. publicly supported charities qualify for this deduction, leaving out DAFs and private foundations entirely [14][17].

For itemizers, the same 0.5% AGI floor and 35% deduction cap apply to contributions to DAFs and private foundations. For example, a $10,000 donation to a DAF would yield a $3,500 tax benefit in 2026, compared to $3,700 in 2025 [14][16]. Doug Hutchinson of Assembly Wealth emphasizes:

"The new 0.5% AGI floor and the lower 35% deduction cap for 2026 apply to DAF contributions, so a 2025 DAF contribution will lead to a larger tax benefit than contributing the same amount in 2026 or later" [17].

Given these updates, maintaining accurate records becomes even more critical. Be sure to separate donations made directly to public charities from those made to DAFs to determine whether you've surpassed the AGI floor. Before claiming any deduction, use the IRS Tax Exempt Organization Search tool to confirm the recipient's status and avoid mistakenly treating a DAF donation as a direct public charity gift [9][2].

Managing Receipts with Deductible.me

Keeping up with IRS recordkeeping requirements can feel like a full-time job, especially when it comes to charitable donations. Deductible.me steps in as a modern solution, offering a centralized digital hub to organize and manage your donation receipts. Whether you're drowning in a mix of paper slips and email confirmations, this platform simplifies the process by consolidating everything in one accessible place.

Why is this important? Proper documentation isn't just a nice-to-have - it’s critical for IRS compliance. As Deductible.me points out:

"A missing date on a key receipt could be all it takes for the IRS to deny your deduction, making proper paperwork absolutely essential" [18].

With Deductible.me, you can upload photos of paper receipts or PDFs of email acknowledgments directly to your records. This creates a permanent, easily accessible link to your donation documentation, ensuring you're always prepared to meet IRS requirements.

AI Valuation and Form 8283 Preparation

Determining the Fair Market Value (FMV) for noncash donations can be a headache. Traditionally, this involves researching comparable sales, noting acquisition dates, and calculating costs manually. Deductible.me eliminates the guesswork with AI-powered tools that suggest FMVs based on the item's type and condition - whether it’s Excellent, Good, or Fair.

The platform also allows you to capture IRS-compliant photos of donated items, documenting their condition as "good used condition or better." This feature is especially useful for noncash donations exceeding $500, which require Form 8283. At the end of the year, Deductible.me generates detailed, itemized reports, making tax preparation much smoother.

Tracking Your Annual Giving Goals

Deductible.me isn't just about compliance - it also helps you stay on top of your charitable giving strategy. The platform tracks your annual progress, ensuring you're maximizing your itemized deductions while staying within IRS guidelines. For those seeking more advanced features, the Premium plan costs just $2 per month and includes unlimited tracking and analytics. If your donation activity is lighter, the Free plan covers up to $500 in donations with basic receipt tracking.

Conclusion

Navigating IRS receipt requirements doesn’t have to be complicated. For cash donations, you’ll need either a bank record or a written acknowledgment. If your contribution is $250 or more, make sure to get a contemporaneous written acknowledgment by the time you file your tax return. For noncash donations over $500, you’ll need to file Form 8283, and donations valued above $5,000 usually require a qualified appraisal.

Common mistakes - like missing dates, incomplete receipts, or forgetting appraisals - can cost you deductions. It’s important to remember that it’s up to you, not the charity, to request and keep the proper documentation for tax purposes.

To make this process easier, digital tools can help you stay organized. For example, Deductible.me lets you manage your donation records digitally, uses AI to provide valuations, and generates IRS-compliant reports, including Form 8283 preparation. Whether you’re tracking smaller donations for free or opting for unlimited tracking with their $2/month Premium plan, this tool can help you stay compliant while maximizing your deductions.

Stay on top of your records: document donations immediately, confirm the charity’s status using the IRS Tax Exempt Organization Search tool before giving, and keep everything organized throughout the year. By combining good record-keeping habits with modern tools, you’ll ensure your deductions are accurate and fully optimized.

FAQs

What counts as a “bank record” for a cash donation?

When making a cash donation, a “bank record” can refer to several things: a canceled check, a bank statement, or a receipt from the charity. The charity’s receipt should include three key details: the name of the organization, the date of the donation, and the amount contributed. These records are essential to comply with IRS rules for documenting charitable contributions.

How do I get a contemporaneous written acknowledgment if the charity won’t send one?

If the charity hasn’t given you a written acknowledgment, you can ask them for a statement that confirms the donation amount and specifies whether you received any goods or services in return. It’s also important to keep thorough records, such as bank statements or canceled checks. The IRS requires clear documentation to back up your deduction, so make sure everything aligns with their guidelines for charitable contributions.

How do I determine fair market value for noncash donations without an appraisal?

When figuring out the fair market value for noncash donations without an appraisal, you can rely on practical methods. For example, evaluate the item's condition, compare it to similar items sold in the market, or refer to IRS valuation guides. If your donation exceeds $5,000, it's especially important to document how you arrived at the value and include any supporting details. Keeping thorough records is essential to comply with IRS guidelines.