Tax Benefits of Short- vs. Long-Term Donations

When donating assets to charity, the tax benefits you receive depend on how long you've owned the asset. Here's a quick breakdown:

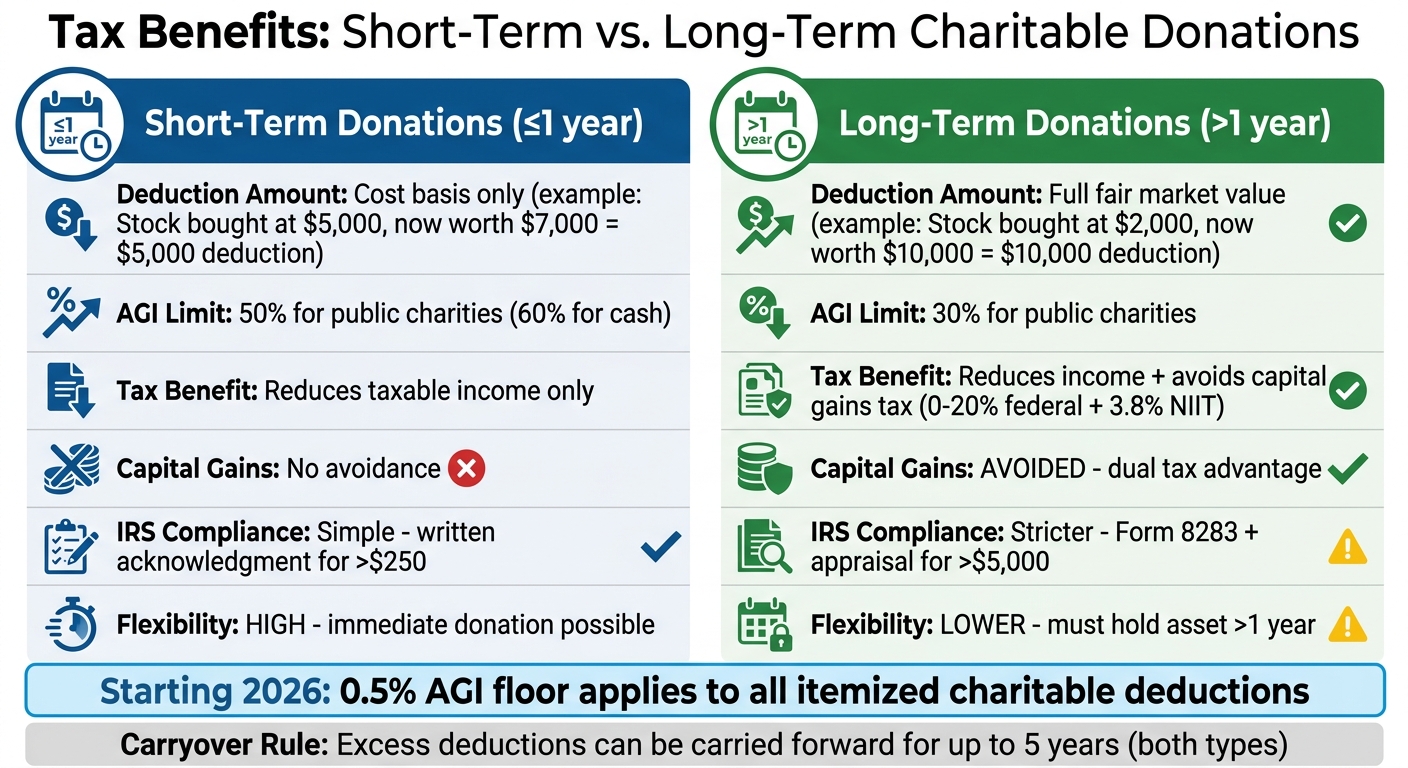

- Short-term donations (assets held for 1 year or less): Deduction is limited to the asset's cost basis (what you paid for it). AGI deduction limit is up to 50% for public charities.

- Long-term donations (assets held for more than 1 year): Deduct the full fair market value (FMV) and avoid capital gains taxes. AGI deduction limit is 30% for public charities.

Starting in 2026, a 0.5% AGI floor for itemized deductions will apply, making it even more important to track and plan donations carefully.

Key tip: Long-term donations often offer greater tax savings, especially for appreciated assets. Tools like Deductible.me can simplify tracking and reporting, ensuring compliance with IRS rules.

Quick Comparison:

| Factor | Short-Term Donations | Long-Term Donations |

|---|---|---|

| Deduction Amount | Limited to cost basis | Full fair market value (FMV) |

| AGI Limit | Up to 50% | Up to 30% |

| Tax Efficiency | Reduces taxable income only | Reduces income + avoids capital gains tax |

| Flexibility | Immediate | Requires holding asset >1 year |

| IRS Compliance | Simple (e.g., written acknowledgment) | Stricter (e.g., Form 8283, appraisals) |

Understanding these distinctions can help you maximize deductions while supporting causes you care about.

Short-Term vs Long-Term Charitable Donations Tax Benefits Comparison

The New "Hidden Floor" on Charitable Deductions Explained

sbb-itb-e723420

1. Short-Term Donations

Short-term donations cover any property held for a year or less. This includes items like recently purchased stocks, business inventory, used clothing, furniture, and even artwork created by the donor. The IRS classifies these as "ordinary income property", which comes with specific tax rules that impact how deductions are calculated [4].

Deduction Basis

How deductions are calculated for short-term donations largely depends on the asset's adjusted basis, which starts with the original purchase price. For short-term property, the IRS limits your deduction to this adjusted basis rather than the current market value. For example, if you bought stock for $5,000 three months ago and its value has since risen to $7,000, your deduction is limited to the original $5,000. The $2,000 gain doesn’t count toward your deduction [4].

The adjusted basis is determined by adding acquisition costs like sales tax or commissions to the original purchase price. It can increase with improvements (e.g., adding a new roof to a property) or decrease due to factors like depreciation, casualty losses, or certain tax credits [4]. If the property was gifted to you, you typically inherit the donor's basis. In contrast, inherited property usually gets a stepped-up basis, meaning its value is adjusted to the fair market value at the time of the original owner's death [4]. Once your adjusted basis is clear, the IRS's AGI limits will determine how much of it you can deduct.

AGI Deduction Limits

For short-term donations to public charities, you can deduct up to 50% of your adjusted gross income (AGI) in a single tax year. Donations to private non-operating foundations have a lower cap, at 30% of your AGI [3]. While these limits are higher than those for long-term donations, the deduction is still restricted to the asset's adjusted basis rather than its current market value.

Carryover Rules

If your short-term donation exceeds the AGI limit, the IRS allows you to carry the excess deduction forward for up to five additional tax years [5]. These carryovers retain their original classification, meaning a short-term donation subject to the 50% AGI limit will remain under that same limit in future years. Each year, current contributions are deducted first, and then the oldest carryovers are applied [5]. Keeping detailed records - such as a spreadsheet tracking the year of donation, property type, recipient, and remaining carryover - is essential for staying compliant and optimizing your donation strategy [5]. These carryover rules can be a helpful tool for spreading out deductions over multiple years.

2. Long-Term Donations

Long-term donations involve assets you've held for over a year, such as appreciated stocks, real estate, mutual funds, and other capital assets that have increased in value since you acquired them. The IRS treats these donations differently than short-term gifts, offering tax benefits that can significantly increase your deduction [7].

Deduction Basis

When donating long-term assets, you can deduct their full fair market value (FMV) instead of just the original purchase price. For example, if you bought stock for $2,000 five years ago and it's now worth $10,000, you can claim a $10,000 deduction when donating it to a qualified charity [1]. This is a major advantage compared to short-term donations, where the deduction is limited to the $2,000 cost basis. However, if an asset has lost value, it’s better to sell it, claim the capital loss, and then donate the cash [1].

Capital Gains Treatment

One of the biggest perks of donating appreciated assets is avoiding capital gains taxes. By giving these assets directly to charity, you skip the federal capital gains tax (which ranges from 0% to 20%, depending on your income) and the additional 3.8% Net Investment Income Tax that applies to high-income earners [1][8].

"It's generally advisable to delay a gift of appreciated property until the long-term holding period can be met."

This advice comes from Gordon Fischer, Founder of Gordon Fischer Law Firm [7]. For instance, a taxpayer with an AGI of $150,000 who donates long-term stock worth $10,000 (originally purchased for $2,000) gets a $10,000 deduction while also avoiding taxes on the $8,000 gain. This creates a dual tax advantage [1].

AGI Deduction Limits

The IRS imposes AGI limits on deductions for long-term appreciated property. Donations to public charities are capped at 30% of your AGI, while contributions to private non-operating foundations are limited to 20% [3][1]. For example, with an AGI of $150,000, your maximum deduction for public charities would be $45,000 (30% of $150,000), even if the total value of your donations exceeds this amount [1].

There’s a workaround: if you reduce your deduction to the asset’s cost basis, the AGI limit increases to 50%. This can be useful if you expect lower income in future years and want to maximize your immediate deduction [5].

Carryover Rules

If your deductions exceed the AGI limits, the excess can be carried forward for up to five years, using a first-in, first-out (FIFO) system [5][9][11]. These carryovers retain their original 30% or 20% AGI classification, regardless of changes in your income [5].

Starting in 2026, new rules will introduce a 0.5% AGI floor for charitable deductions. However, carryovers from 2025 or earlier will not be subject to this floor [10]. For instance, if your AGI in 2026 is $100,000 and you donate $10,000, $500 (0.5% of your AGI) would be postponed, leaving a $9,500 deduction for the current year [6]. Keeping detailed records is essential to ensure compliance. As with short-term donations, careful planning of long-term gifts can help you align your charitable goals with IRS guidelines.

Advantages and Disadvantages

When it comes to charitable giving, short-term and long-term donations come with distinct tax benefits and compliance requirements. Understanding these differences can help you craft a strategy that aligns with your financial goals and tax planning needs.

Short-term donations - such as cash, checks, or assets held for less than 12 months - are straightforward and offer immediate flexibility. The IRS keeps the requirements simple: for donations over $250, you’ll need bank records or written acknowledgments. One major advantage is the higher AGI deduction limit of 60% for cash donations [12]. However, these contributions are limited to your cost basis, meaning you won’t avoid capital gains tax on any appreciation [7]. Also, starting in 2026, itemizers will face a 0.5% AGI floor for deductions.

Long-term donations, on the other hand, involve assets held for more than a year, like appreciated stock. These donations provide a double tax benefit: you can deduct the full fair market value and avoid paying capital gains tax [12][13]. However, stricter IRS rules apply. For assets valued over $5,000, you’ll need to file Form 8283 and secure a qualified appraisal. Long-term donations also come with a lower AGI deduction limit of 30% when donating securities to public charities. Additionally, these assets may be less liquid, potentially delaying their conversion to cash for the receiving charity.

Here’s a quick comparison of the two approaches:

| Factor | Short-Term Donations | Long-Term Donations |

|---|---|---|

| Deduction Amount | Limited to cost basis only | Full fair market value |

| AGI Limit | Up to 60% for cash donations | Up to 30% for securities |

| Tax Efficiency | Reduces taxable income only | Reduces taxable income and avoids capital gains tax |

| Flexibility | High; donations can be made immediately | Lower; assets must be held for more than a year |

| IRS Compliance | Simple (e.g., written acknowledgments for donations over $250) | Stricter (requires Form 8283 and appraisals for assets over $5,000) |

| 2026 AGI Floor Impact | Subject to the 0.5% AGI floor for itemizers | Subject to the 0.5% AGI floor for itemizers |

"One-size-fits-all approaches to charitable giving often fall short. Donors should evaluate their financial goals, tax situation, and philanthropic objectives to determine the most effective gifting strategy."

If you’re managing multiple donations throughout the year, tools like Deductible.me can simplify the process. These platforms offer IRS-compliant reporting and AI-powered valuations, helping you stay organized and maximize deductions no matter which strategy you choose.

Ultimately, your decision will depend on factors like your income, asset mix, and comfort with administrative tasks. Many donors find that combining cash for immediate needs with appreciated assets for planned gifts strikes the right balance between maximizing tax benefits and supporting meaningful causes.

Conclusion

Deciding between short-term and long-term donations depends on factors like your income, asset mix, and how comfortable you are with handling IRS documentation. Cash donations and short-term asset contributions are relatively simple to document and typically allow deductions up to 60% of your adjusted gross income (AGI) [14]. On the other hand, donating long-term appreciated assets offers a notable tax advantage: you can deduct the full fair market value and skip paying capital gains tax.

Gordon Fischer from the Gordon Fischer Law Firm emphasizes, "It's generally advisable to delay a gift of appreciated property until the long-term holding period can be met" [7]. For depreciated assets, selling them first to claim a capital loss before donating the proceeds is often the smarter move [14].

With the upcoming 0.5% AGI floor set to take effect in 2026 [2], staying on top of every deductible expense becomes even more important. Small, overlooked deductions can add up quickly. To simplify this, tools like Deductible.me offer AI-powered valuations, IRS-compliant Form 8283 reporting, and unlimited donation tracking. Their Premium plan, priced at just $2 per month, helps ensure you capture every eligible deduction - whether you're donating cash, securities, or other assets - and stay compliant with IRS requirements.

FAQs

When does the 1-year holding period start for donated assets?

The 1-year holding period for donated assets begins the day after you acquire the property. According to IRS guidelines, this means the clock starts ticking the day after the acquisition date.

Should I donate appreciated stock or sell it and donate cash?

Donating stocks that have increased in value directly to a qualified charity can often be a smarter tax move than selling them and giving cash. Why? Because when you donate stock, you skip paying capital gains taxes on the appreciation. Plus, you can claim a deduction based on the stock's fair market value at the time of the donation. On the other hand, selling the stock first means you'll owe taxes on the gains, which reduces the amount you can give. If you're looking to make the most of your tax benefits, giving appreciated stock is typically the way to go.

What records and IRS forms are required for non-cash donations over $5,000?

For non-cash donations over $5,000, you’ll need to fill out Section B of IRS Form 8283 and get a qualified appraisal for the donated property. Make sure the appraisal aligns with IRS standards to meet all reporting requirements.