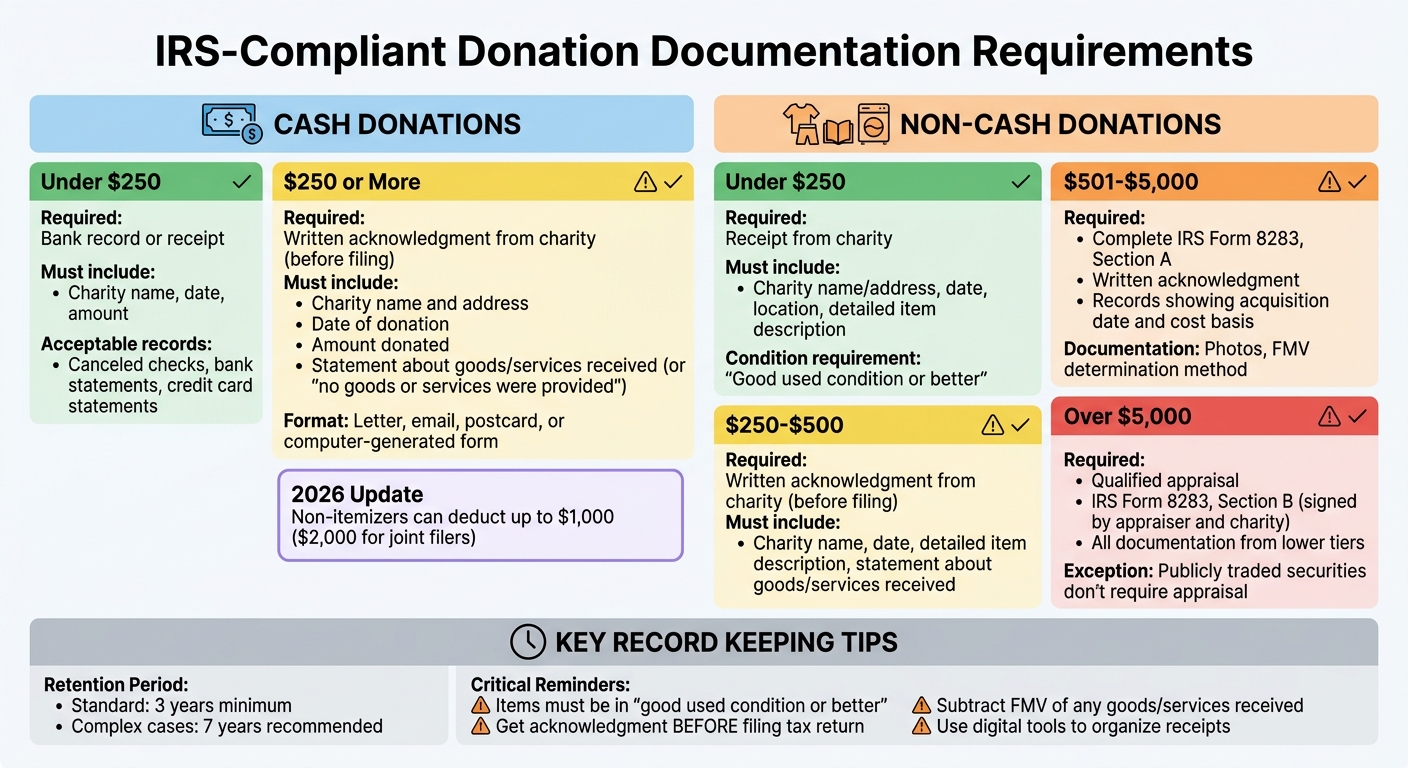

Checklist for IRS-Compliant Donation Records

When it comes to claiming tax deductions for charitable donations, proper documentation is key. The IRS has specific guidelines based on the type (cash or non-cash) and value of your donation. Missing or incomplete records can lead to deductions being denied during an audit. Here’s what you need to know:

-

Cash Donations:

- Under $250: Keep a bank record or receipt with the charity's name, date, and amount.

- $250 or more: Obtain a written acknowledgment from the charity before filing your tax return.

- Starting 2026: Non-itemizers can deduct up to $1,000 ($2,000 for joint filers).

-

Non-Cash Donations:

- Under $250: Get a receipt with the charity’s name, date, location, and item description.

- $250–$500: A written acknowledgment is required.

- $501–$5,000: Complete Form 8283, Section A, and provide detailed records.

- Over $5,000: A qualified appraisal and Form 8283, Section B, are mandatory.

-

Key Tips:

- Ensure all items are in "good used condition or better."

- Keep records for at least three years (seven years for complex cases).

- Use digital tools to organize receipts and valuations.

Proper documentation ensures your deductions are secure and audit-proof. Without it, even legitimate donations can be disallowed.

IRS Donation Documentation Requirements by Type and Value

Charitable Contributions: Recordkeeping Requirements

sbb-itb-e723420

Documentation Requirements for Cash Donations

To ensure your cash donation records meet IRS standards, follow these guidelines. Cash donations cover more than just physical currency - they include checks, credit card and debit card payments, electronic funds transfers, and even donations made through apps like PayPal or Venmo.

Cash Donations Under $250

For donations under $250, you’ll need a bank record or documentation from the charity, such as a receipt, letter, or email. Acceptable bank records include canceled checks, bank statements, or credit card statements that show the charity’s name, the transaction date, and the donation amount. Credit card statements should also list the posting date.

The $250 limit applies to each individual donation. For instance, if you donate $100 three times to the same charity in a year, each contribution only requires basic documentation - you won’t need a formal acknowledgment just because the total exceeds $250. However, if you receive goods or services (like a ticket to a charity dinner) for a donation under $250, you’ll need a written acknowledgment from the charity. Your deduction must also be reduced by the value of what you received.

For donations of $250 or more, stricter documentation rules apply.

Cash Donations of $250 or More

For single donations of $250 or more, you must get a written acknowledgment from the charity before filing your tax return. This acknowledgment can be a letter, email, postcard, or a computer-generated form. It must include:

- The charity’s name and address

- The date of your donation

- The amount donated

- A statement clarifying whether goods or services were provided in return

If you received nothing in return, the document should explicitly state, "no goods or services were provided." If you did receive something, such as event tickets or merchandise, the acknowledgment must describe the items and provide a good faith estimate of their value.

It’s essential to have this acknowledgment before filing your tax return. You need it in hand by the earlier of the date you file or the return’s due date (including extensions). As SD Mayer cautions:

If you file your return without having the letter in hand, you cannot go back and get it later to fix a mistake if audited.

To avoid audit complications, ensure you have the acknowledgment before filing. Remember, it’s your responsibility as the donor to secure this documentation - don’t assume the charity will automatically send it.

Documentation Requirements for Non-Cash Donations

Non-cash donations require a bit more effort than cash donations when it comes to documentation. The IRS has clear rules based on the value of the donation, and you’ll need to provide specific details about the property’s condition and valuation.

Non-Cash Donations Under $250

For donations valued under $250, you’ll need a receipt from the charity. This receipt should include:

- The charity’s name and address

- The date and location of the donation

- A detailed description of the donated items

According to IRS Publication 526:

If you make any non-cash contribution, you must get and keep a receipt from the charitable organization showing: 1. The name of the charitable organization, 2. The date and location of the charitable contribution, and 3. A reasonably detailed description of the property.

If you can’t get a receipt, you should still keep personal records, like photos, to document the items’ condition and fair market value. It’s also important to note that clothing and household items must generally be in "good used condition or better" to qualify for a deduction, no matter their value.

Non-Cash Donations $250 to $500

When the value of your donation hits $250 or more, you’ll need a written acknowledgment from the charity. This document must include:

- The charity’s name

- The date of the donation

- A detailed description of the donated items

- A statement indicating whether you received any goods or services in return

Make sure you receive this acknowledgment before filing your tax return.

Non-Cash Donations $501 to $5,000

If your non-cash donations total more than $500, the IRS requires additional documentation. You’ll need to:

- Complete IRS Form 8283, Section A

- Attach the form to your tax return

- Include a written acknowledgment from the charity

- Provide records showing when you acquired the items and their original cost basis

Tom O'Saben, EA, from the University of Illinois Tax School, emphasizes the importance of accurate valuation:

Fair market value (FMV) is the price that property would sell for on the open market between a willing buyer and a willing seller, with neither being required to act.

Document how you determined the FMV - whether you used online resale sites, thrift store pricing guides, or other methods. Photos and detailed notes about the items’ condition will also help meet the IRS’s “good condition or better” standard. Avoid using rounded numbers like $499, as these can raise red flags during an audit.

Non-Cash Donations Over $5,000

For donations exceeding $5,000, the rules become even stricter. You’ll need a qualified appraisal and must complete IRS Form 8283, Section B. Both the appraiser and an authorized official from the charity must sign the form. However, publicly traded securities are an exception and don’t require an appraisal, even at this level.

The IRS explains:

The signature does not represent agreement with the appraised value of the contributed property. A signed acknowledgment represents receipt of the property described on Form 8283 on the date specified on the form.

Make sure to get the charity’s signature on Form 8283 before submitting your tax return. Note that the charity cannot act as your appraiser, and you must provide the charity with a copy of the completed and signed form. If the charity sells or disposes of the donated property within three years, they are required to file Form 8282 (Donee Information Return) within 125 days and give you a copy.

Up next, we’ll explore tips for keeping your records organized to stay compliant with IRS guidelines.

Record Keeping Best Practices

Keeping your donation records in order isn’t just a good habit - it’s essential for staying on the IRS’s good side and protecting yourself during audits. Here’s how to do it right.

How Long to Keep Donation Records

The IRS typically has a three-year window from the date you file your return to conduct an audit. So, at a minimum, hold onto your donation records - both cash and non-cash - for three years. However, when it comes to more complex gifts, like those requiring professional appraisals or involving tax carryovers, many tax experts suggest keeping those records for seven years for extra peace of mind.

As Greg McRay, EA, Founder and CEO of Foundation Group, explains:

If it's not in writing, it didn't happen [4].

This means that without a proper written acknowledgment for donations of $250 or more, the IRS could reject your deduction - even if you have a bank statement to back it up. For carryover contributions, make sure to retain records until seven years after the final carryover is used. Similarly, for high-value gifts over $5,000, keep appraisal documents on hand for at least seven years.

Now that we’ve covered the "how long", let’s talk about the "how."

How to Organize Donation Records

A little organization goes a long way when tax season rolls around - or if you ever face an audit. Start by categorizing your records by type and value. Use separate folders - physical or digital - labeled by tax year, and then break them down further by donation type (e.g., "2026_Cash_Donations" or "2026_Non-Cash_Items"). Keep each donation’s main receipt alongside any supporting documents, like bank statements or photos.

If you’re still dealing with paper receipts, consider scanning or photographing them to create digital backups. For non-cash donations, maintain an inventory that includes details like item descriptions, quantities, conditions, and how you determined their fair market value. Adding quick notes about why you made the donation can also save time if you’re ever asked to explain it.

Digital Tools for Tracking Donations

Gone are the days of juggling spreadsheets and shoeboxes full of receipts. Digital tools can take the hassle out of managing your records while ensuring you meet IRS requirements.

For example, platforms like Deductible.me offer features that make tracking donations a breeze. They securely store receipts, automate IRS-compliant reporting, and even provide AI-powered valuation for donated items. The platform can generate ready-to-use reports for Form 8283 and centralize all your documentation in one place. With a Premium plan costing just $2/month, you can enjoy unlimited tracking, advanced analytics, and priority support.

Make it a habit to record donations as soon as you make them to avoid leaving anything out. For non-cash contributions, take clear photos to document their condition - remember, items must be in "good used condition or better" to qualify for a deduction [2] [5]. If you’re a recurring donor, check if your charity provides an annual summary statement. These summaries can save you the trouble of managing individual receipts throughout the year.

Common Record Keeping Mistakes to Avoid

Even with the best intentions, donors can lose out on tax deductions because of simple documentation mistakes. Avoiding these common errors can save you stress during tax season - or worse, an IRS audit.

Missing Timely Documentation

One of the most frequent slip-ups is filing your tax return without having the proper acknowledgment letter in hand. A bank statement alone won’t cut it; you need a contemporaneous written acknowledgment.

If you file without this required documentation, the IRS can disallow your deduction during an audit, and you won’t be able to fix it later. To prevent this, make it a habit to request acknowledgment letters immediately after making any substantial donations. Always ensure you have the required written acknowledgment before filing your tax return.

Let’s take a closer look at another common error - how donated items are valued.

Incorrect Valuation of Donated Items

Another widespread mistake is valuing donated items based on their original purchase price instead of their fair market value (FMV). FMV reflects what an item would sell for in its current, used condition - not what you paid for it.

As the Charity Record Team explains:

A shirt you paid $50 for isn't worth $50 when you donate it. It's worth what Goodwill would sell it for: maybe $3–8 depending on condition [1].

To get the valuation right, use guides from organizations like Goodwill or the Salvation Army, or check eBay’s "sold" listings for similar items. Also, keep in mind that the IRS typically allows deductions for clothing and household goods only if they’re in "good or better" condition. Items that are stained, torn, or broken usually don’t qualify.

Now, let’s explore how benefits tied to donations can affect your deductions.

Failing to Account for Goods or Services Received

If your donation includes benefits - like event tickets or merchandise - you need to subtract the FMV of those benefits from the donation amount. Ignoring this can lead to overstating your deduction.

For donations of $250 or more, the charity’s acknowledgment letter must specify either the value of any goods or services you received or confirm that "no goods or services were provided." Only the portion of your donation that exceeds the value of those benefits is tax-deductible. For example, if you donate $500 and receive benefits worth $75, your deductible amount is $425.

Conclusion

Sticking to the checklist and best practices outlined above ensures your charitable donations can withstand IRS scrutiny. Keeping proper donation records isn't just about avoiding trouble with taxes - it’s about making sure you claim every dollar you're entitled to. As M&J CPA explains:

A charitable gift may be legitimate, but if the taxpayer fails to substantiate it properly, the deduction may be lost [3].

The lack of required, timely documentation is the leading reason deductions are denied during audits [1]. And with changes coming in 2026 - like the 0.5% AGI floor for itemized charitable deductions and capped rates for higher-income taxpayers - keeping accurate records will be even more important to preserve your tax benefits [6].

Thankfully, technology makes this easier. Tools like Deductible.me streamline donation tracking with features like AI-powered valuation, automatic IRS-compliant reporting, and centralized storage. Their Premium plan is just $2/month and offers unlimited tracking, Form 8283 preparation, and advanced analytics to keep you organized throughout the year.

Whether you’re donating $50 in gently used clothes or $5,000 in appreciated stock, having the right documentation at the right time safeguards you during audits and ensures you claim every deduction you're entitled to. Follow IRS guidelines for record retention and remember: getting organized before filing is far easier than scrambling if the IRS comes calling [2].

Start implementing these strategies now to protect your deductions and make tax season less stressful.

FAQs

What counts as a “contemporaneous written acknowledgment”?

A “contemporaneous written acknowledgment” is a document provided by the charity for donations of $250 or more. This acknowledgment must include:

- The charity’s name.

- The cash amount donated.

- A description (but not the value) of any non-cash items contributed.

- A statement indicating whether goods or services were provided in exchange for the donation.

- If goods or services were provided, a description and an estimate of their value.

- A note specifying if only intangible religious benefits were received.

This documentation is essential for tax purposes and ensures compliance with IRS regulations.

How do I prove fair market value for donated items?

To establish the fair market value (FMV) of donated items, focus on aspects like their condition, age, and resale potential. It's important to maintain proper documentation, such as receipts, written acknowledgments, or appraisals. If the donated item's value exceeds $5,000, you'll generally need a professional appraisal. The valuation should accurately represent the FMV at the time of donation, taking into account the item's current state and its appeal in the market.

When do I need an appraisal and Form 8283?

When donating noncash items valued over $5,000, you'll need both a qualified appraisal and Form 8283 to document the donation's value for the IRS. If the donation's value falls between $500 and $5,000, only Form 8283 is required, and an appraisal isn't usually necessary unless the IRS specifically asks for one. For donations above $5,000, make sure to complete Section B of Form 8283 and secure a proper appraisal to stay compliant with tax regulations.